Download

1 / 3

30 likes | 41 Vues

This report describes India BNPL Market Consumer Segment, India BNPL Market E-commerce Sector, India BNPL Market Retail Sector, India BNPL Market Fintech Industry, India BNPL Market Partnership and Collaborations, India BNPL Market Future Prospects, India BNPL Market Competitive Landscape, India BNPL Market Value Chain Analysis.

E N D

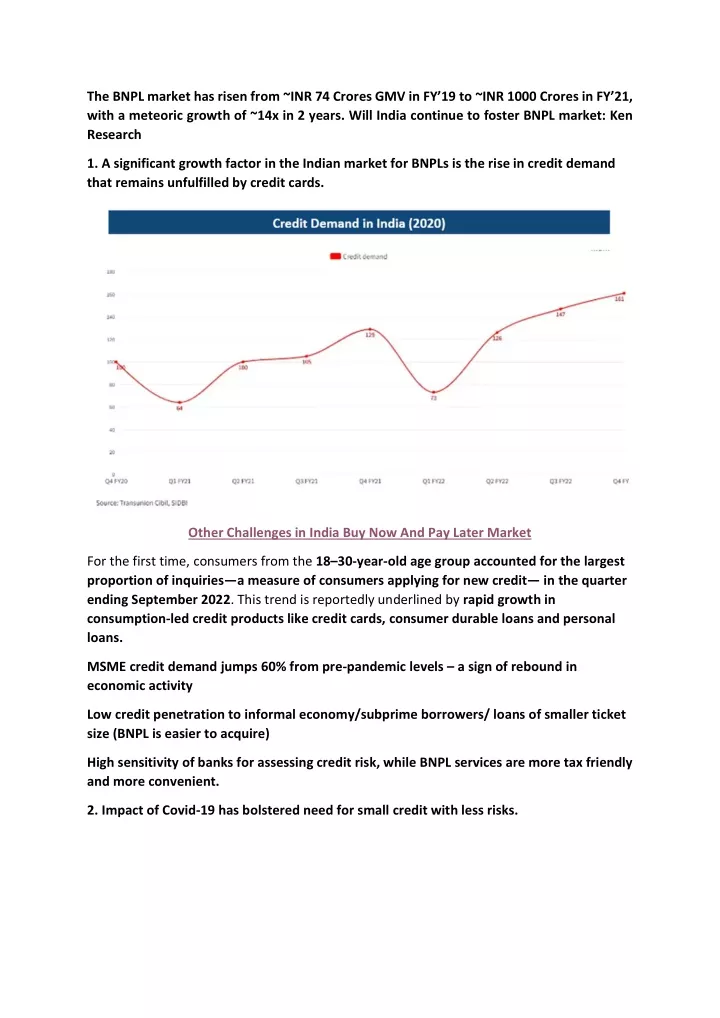

The BNPL market has risen from ~INR 74 Crores GMV in FY’19 to ~INR 1000 Crores in FY’21, with a meteoric growth of ~14x in 2 years. Will India continue to foster BNPL market:Ken Research 1. A significant growth factor in the Indian market for BNPLs is the rise in credit demand that remains unfulfilled by credit cards. Other Challenges in India Buy Now And Pay Later Market For the first time, consumers from the 18–30-year-old age groupaccounted for the largest proportion of inquiries—a measure of consumers applying for new credit— in the quarter ending September 2022. This trend is reportedly underlined by rapid growth in consumption-led credit products like credit cards, consumer durable loans and personal loans. MSME credit demand jumps 60% from pre-pandemic levels – a sign of rebound in economic activity Low credit penetration to informal economy/subprime borrowers/ loans of smaller ticket size (BNPL is easier to acquire) High sensitivity of banks for assessing credit risk, while BNPL services are more tax friendly and more convenient. 2. Impact of Covid-19 has bolstered need for small credit with less risks.

Interested to Know More about this Report, Interested to Know More about this Report, Request For The Sample Report Request For The Sample Report COVID19 has given rise to a trend of saving more; India having the highest population of experimental consumers willing to try new technologies. A rising unemployment rate during the COVID19 pandemic has sparked an increase in household financial saving in India, geared more towards bank deposit. As risk of unemployment heightened during the pandemic, the financial sensitivity has increased. Thus, a platform impacting credit score positively even with smaller loan amounts is welcome by many like BNPL services which provide hassle free, risk free and instant loans. 3. Niche models such as Off-card financing solutions focused BNPL providers have lesser competition in the Indian BNPL Market.

Visit This link :- Visit This link :- Request For Custom Report Request For Custom Report Point of sales (POS) financing is one of the most sought-after ways for a user to finance their purchase. In fact, a survey shows about 60% of users say they are likely to use POS financing over the next 12 months. Banks have offered POS financing for a long time now, but have failed to upgrade their tech and improve customer journeys to enable a better user experience. Initially, POS financing was also largely limited to the purchase of high-priced merchandise, usually capital goods. The growth of e-commerce and specifically direct-to- consumer business models have propelled the demand for small ticket size purchases as well. This was the starting point for many BNPL providers, who initially focused on small ticket size purchases. They focused their entire efforts on building an effortless customer journey. They built a simple user interface and reduced all friction in the onboarding process. Off-card financing solutions offer consumers to pay a 0% APR for a certain period and then a subsidized Annual Percentage Rate (APR). These players, while charging EMI, offer lower rates than credit cards, and hence are preferred over them. Majority of customers (>80% are credit card owners looking for cheaper financing solutions. This model has not yet established roots in India, due to higher cost of acquisition making business model unfeasible for such a low penetration of credit cards.