Download

1 / 14

140 likes | 384 Vues

A leading Retail software company, delivering Retail Solutions with seamless integration through CRM, POS, Merchandise Planning and Promotion campaigns.

E N D

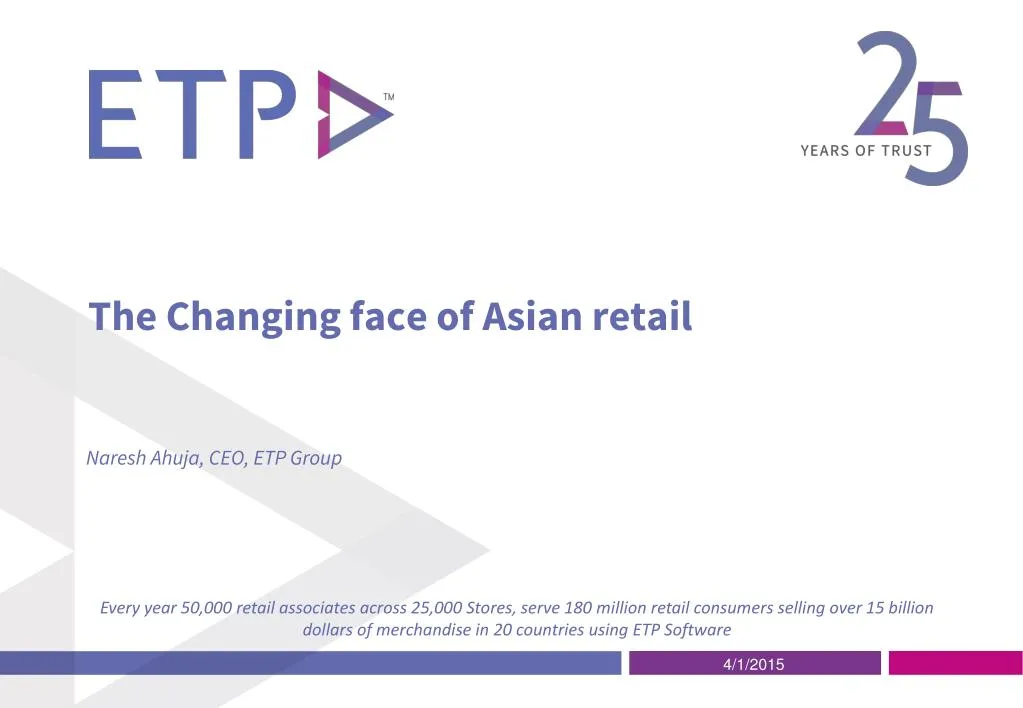

The Changing face of Asian retail Naresh Ahuja, CEO, ETP Group Every year 50,000 retail associates across 25,000 Stores, serve 180 million retail consumers selling over 15 billion dollars of merchandise in 20 countries using ETP Software 4/1/2015

The Middle class in SE Asia, India and China in 2012, 74% of Major Markets

The Middle class in SE Asia, India and China in 2020, 85% of Major markets

Growing Middle Class 1200 1000 800 600 400 200 0 India SEA China Brazil France, Germany, UK US 2012 2020

GDP per capita Growth in Asia 12,000 10,000 8,000 6,000 4,000 2,000 0 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 China India Indonesia Philippines Thailand

Asian Business Models Company Owned Multi Brand Shop In Shop Multi Country Franchisor Models ETP Multi Company Franchisee Models Wholesale Sales Consignment Models Web Sales Channel

eCommerce and Omni-Channel in Asia Customer expectations are that all retailers and brands should have a consistent experience across brick and click channels, not there yet However, most brands and retailers are yet to agree on an eCommerce strategy Retailers are slow to invest in an omni-channel strategy Merchandise Planning for e-commerce becoming a hot area CRM is becoming a key factor across channels as many players compete for wallet share Large Venture investments in ecommerce create uncertainty and volatility in the minds of retailers as ecommerce vendors use cash to buy revenue With COD and easy returns, people are more comfortable with shopping online • • • • • • • Credit/Debit Cards issued %age of population Country Indonesia Phillipines Malaysia India Thailand Singapore Poulation 74 50 28 255 102 31 1299 68 29% 49% 90% 102% 161% 740% 1,320 109 37 5

Thailand Political uncertainty, yet in 2014 consumer spending increased Tourism bounces back after a brief slow down Retailers see the need to internationalize their business Few very large players then a big gap, and then mid-sized players More focus on CRM as there is a need to have steady revenue in down times Local Mall groups continue expansion Consignment and SIS models continue to dominate the market, pose huge challenges in transparency 2014, Ecommerce <1% of Retail sales, expected to be 1.5 % by 2018 • • • • • • • •

Philippines BPOs and Foreign Worker Inflows have improved the urban economies of the Philippines, Japanese investments in manufacturing There is good growth outside Metro Manila as well and malls are springing up in smaller cities and towns along with the advent of small community malls catering to the demographic mix A young and vibrant population with a demand for fashion and convenience is driving value and fast fashion Personal high quality services is expected and provided A large number of mid sized retailers and 4 to 5 large retailers dominate the space Improving mall and telecom infrastructure is helping retailers modernize 2014, Ecommerce 0.4% of Retail sales, expected to be 1 % by 2018 • • • • • • •

Indonesia A young consumer with growing affluence in ASEANs largest economy, 16th largest in the world and will be 7thlargest by 2030 Currency volatility affects GDP and international brands try to absorb expensive dollar High growth of 1stclass malls, a discerning consumer buy locally and no longer only abroad Retail sales expected to grow 12-14% YOY from 411 BUSD in 2014 Indonesian retailers bullish and expanding rapidly outside Jakarta Traditional retail at 78% is expected to drop to 58% by 2018, showing the high growth of modern retail Large retailers consolidating smaller ones 2014, Ecommerce <1% of Retail sales, expected to be 1.4 % by 2018 • • • • • • • •

India Market is buoyant both in retail and e-commerce, positive consumer sentiment International retailers investing strongly and understanding India price points and buying patterns Local brands mushrooming, RituKumar, Chemistry, AND….. Due to Billions invested in e-commerce huge discounts on various brands and products are given by Flipkartand Myntra etc.. Many brands setting up their own ecommerce channels, and offering ecommerce players EOSS merchandise Supply chain challenges continue, improvements are slow Unified GST to be introduced in 2016 2014, Ecommerce 0.8% of Retail sales, expected to be 1.6 % by 2018 • • • • • • • •

The Changing face of Asian retail Naresh Ahuja, CEO, ETP Group Every year 50,000 retail associates across 25,000 Stores, serve 180 million retail consumers selling over 15 billion dollars of merchandise in 20 countries using ETP Software 4/1/2015