Download

1 / 16

160 likes | 412 Vues

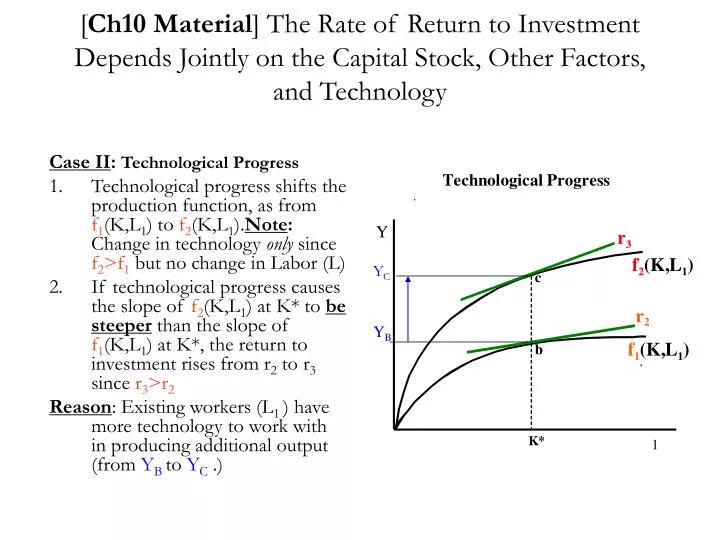

[ Ch10 Material ] The Rate of Return to Investment Depends Jointly on the Capital Stock, Other Factors, and Technology. Case II : Technological Progress

E N D

[Ch10 Material] The Rate of Return to Investment Depends Jointly on the Capital Stock, Other Factors, and Technology Case II: Technological Progress • Technological progress shifts the production function, as from f1(K,L1) to f2(K,L1).Note: Change in technology only since f2>f1 but no change in Labor (L) • If technological progress causes the slope of f2(K,L1) at K* to be steeper than the slope of f1(K,L1) at K*, the return to investment rises from r2 to r3 since r3>r2 Reason: Existing workers (L1 ) have more technology to work with in producing additional output (from YBto YC .) YC YB

[Ch.10 Material] International Investment and Economic Growth The Schumpeterian R&D model is used to explain how international investment might be expected to contribute to technological progress. One of the big issues is whether international investment facilitates the flow of technology from one country to another. There is some evidence that foreign direct investment (FDI) indeed does that, although the precise ways in which it transfers technology are still a very active area of research. The linkages between other forms of international investment and technology are even less understood. • International investment has been linked to economic growth (Recall Chapter 5?). • To understand the possible links, recall the Schumpeterian model of technological progress (q), summarized as: q = f( π, r, R, β ). • The variable q is the quantity of innovations generated in the economy, R the supply of resources in the economy, π is the profit from innovating, βthe efficiency of R&D activities in terms of the resources necessary to generate an innovation, and r is the interest rate that reflects people’s valuation of future gains versus current income and at which the returns from investments in R&D must be discounted.

[Ch.10 Material] International Investment and Economic Growth • International investment is likely to affect technological progress through π, the profit from innovation. • Because it contributes to globalization, which is essentially the integration of separate economies into a single world economy, international investment raises the potential profits from innovation. • International investment can reduce the cost of innovation, β, because it facilitates the flow of ideas. • There is evidence that foreign direct investment (MNE etc) leads to the transfer of technology to the recipient countries, and other forms of investment may also facilitate information flows between economies, thereby reducing β.

[Ch.10 Material] Why Is International Investment So Small?,1 • Investment is subject to some degree of risk. Investment is an intertemporal transaction where one party agrees to accept payment(s) at some future date. It is impossible to foresee the future with certainty. • There are also some perverse incentives that increase the likelihood that future payments will fall short of previously agreed-to levels (default issues.) • Thus, international investment faces greater difficulties in foreseeing the future and countering perverse incentives.

[Ch10 Material] Why Is International Investment So Small?,2 • Information available to lenders and borrowers is often asymmetric, with lenders knowing less than borrowers about the eventual payout of assets. • Asymmetric information can result in adverse selection, which is the case where, because buyers have difficulty in verifying the quality of assets, a disproportionate amount of “bad” assets (loans by banks) are likely to be offered for sale to “high-risk” buyers • Moral hazard refers to the likelihood that once borrowers have acquired a loan, sold stock, or sold a bond, they will behave differently than they would had they not gained the financing, thereby reducing the eventual earnings from an asset.

Chapter 11. Multi-National Enterprises (MNEs) • MNEs are involved in over 75% of all international trade. either as the exporter, the importer, or both. • MNEs account for a major portion of international investment. • MNE investments are categorized as Foreign Direct Investment (FDI). • There is extensive evidence that FDI is the international investment most likely to facilitate international technology transfers. • MNEs do many things that could, theoretically, be accomplished by individual firms in different countries, which means that the growth of MNEs must be due to some special advantages that international business organizations have over individual national firms. • MNEs have advantages in over arms’ length transactions between firms in different countries. • MNEs are both admired and criticized anywhere; unemotional discussion of why MNEs have grown helps to put the conflicting views into perspective. • It is also important to relate MNEs to FDI in order to highlight the fact that international trade and investment are related in complex ways.

Vertical and Horizontal FDI • Foreign direct investment undertaken by MNEs is often classified as either vertical and horizontal. • Vertical FDI implies that an MNE owns facilities that fit into different stages of the supply chain. More vulnerable to disruptions. • Horizontal FDI, on the other hand, consists of MNE investments that duplicate facilities and operation in several countries. In terms of risk management, this strategy impacts less on the firm in case of a serious disruption, such as war.

Among the reasons for the growth of MNEs are: • It can be less costly to internalize transactions within a business organization than to deal with outside firms. Benefits from “transfer pricing.” • Proprietary knowledge is often best exploited in-house. • By expanding overseas, economies of scale can be exploited. i.e. an expanding market allows longer production runs, for example, FDI in China • Reputations can be exploited in more than one market. It cuts both ways, Nestle products in the 70s! • Trade restrictions can be avoided by producing overseas behind tariff walls. Example, Celtic Tiger (Republic of Eire) ≈ Ireland

Among the reasons for the growth of MNEs are: • Taxes and regulations induce business to move activities across borders. CA firms located in Nevada, just across the border – problem workman’s compensation • Exchange rate risk inherent to international trade and investment can be reduced by spreading expenses and earnings across borders. Example: RUS =RUK + E(St+1) - St/ St • FDI may be possible when financial markets do not exist to otherwise channel funds to profitable projects. Equatorial Africa--- hardly any financial markets but lots of oil • A local presence can help firms anticipating favorable local business opportunities. Example – US companies working through 3rd parties, well before the US lifted sanctions against Libya!

MNEs and International Technology Transfers • MNEs use FDI to establish their methods and proprietary techniques in foreign countries. • MNEs also transfer people, designs, business philosophies, and management techniques across borders. • The evidence strongly suggests that the technological leaders in each industry are also the more active foreign investors. • Because firms do not easily part with proprietary technology, FDI may be the only way to introduce cutting-edge technology into a country.

Portfolio Investment Portfolio investment is another of the very largest categories of international investment. This category’s recent rapid growth, has largely been due to the widespread establishment of stock and bond markets throughout the world. Portfolio investment consists of purchases and sales of securities, such as bonds and stocks, in amounts that do not imply any direct management control or influence on the businesses issuing the securities. • Portfolio investment has, along with FDI, become one of the two largest categories of international investment. • The prominence of international portfolio investment is been a very recent phenomenon, however. • International portfolio investment first required the development of stock and bond markets in other countries. • Portfolio investment is widely used by investors to spread risk as well as to raise overall returns to savings.

International Banking • A critical characteristic of international banking is the emergence of the euro-currency markets. Offshore banking usually elicit strong views for and against it. The growth of the euro-currency markets is an interesting example of how global economic activity evolves in response to economic incentives and the rules and policies established by national governments. • Table 11.5 gives an idea of who the big players in international banking are. The rankings have been changing frequently, and indications are that they will continue to change as further mergers and acquisitions (M&A) take place. • Another issue is the recent wave of cross border mergers among the world’s largest commercial banks. Interesting issues include (a) whether international banking will increase or decrease the volatility of savings flows across borders, (b) whether the increased mobility of savings will lead to a greater concentration of flows to particular countries or a broader dispersal of savings across countries, and (c ) whether countries’ ability to regulate and direct savings flows within their borders will be weakened. NOTE: The term euro-currency is misleading because it seems to imply that such markets are located in Europe! In reality, any currency market is so designated provided the currency is outside the country of origin. Thus, we have euro-yen, euro-pound, eurodollar, and euro-rand markets outside Japan, UK, US, and South Africa respectively.

Foreign Aid • Foreign aid is not, strictly speaking, international investment. In the balance of payments it is included under transfers in the current account. But it is an important international “capital flow,” so it is included in this chapter’s discussion of financial flows. Foreign aid as a percentage of world GDP has declined in recent decades. • By 2002, there appeared to be increased interest in foreign aid by both opponents to globalization and proponents of globalization, but there was no clear sign that the volume of international aid was about to increase. • Foreign aid usually stirs strong emotions on either side of the debate. Are the alleged goals of foreign aid, namely economic growth and a reduction in poverty, better achieved through other means? [The 2015 Millennium Goals] How can donor countries prevent recipient governments from stealing or otherwise misusing the foreign aid? Should developed countries send more aid to developing countries? What precisely should foreign aid try to accomplish? Where does foreign aid fit in with other policies to promote international bank lending, FDI, and portfolio flows? What is the responsibility of people in one country vis-a-vis people in other countries? How does that responsibility differ from people’s responsibilities towards fellow citizens? Should it differ? That latter question brings into the whole issue of nationhood and globalization into the discussion. Philosophy and International Affairs types should enjoy these types of discussions!

International Investment: A Historical Perspective • When measured as a proportion of GDP, capital flows in the 1800s were much larger then than they are now. • But, because financial markets were not as developed, international investment was not nearly as diverse as today. • International investment flows were always subject to occasional defaults and renegotiation. • Most foreign debt was serviced on schedule by borrowers, and, in the case of Great Britain, the overall returns on foreign bonds were at least as high as they were on domestic British assets. • International investment came to a complete halt during the 1930s, only to recover toward the end of the 20th century.

International Investment: A Historical Perspective • International investment grew rapidly after World War II, but this growth was not uniform. • Immediately after World War II, foreign aid dominated. • During the 1950s, MNEs began to spread across borders and the eurocurrency market was born. • International bank lending and FDI accounted for much of the international investment among developed economies. • In the 1970s the eurocurrency lending to the developing economies grew rapidly, but the 1982 debt crisis slowed bank lending during the 1980s. • In the 1990s, bank lending was surpassed by FDI and portfolio investment as the largest categories of international investment.

The rapid growth of international investment that we are experiencing raises interesting questions: • What will be international investment’s role in the process of globalization in the future? • Will future international investment flows be as volatile as they have been over the past 25 years, or will they be more stable?