Download

1 / 26

280 likes | 818 Vues

International Parity Conditions . By : Madam Zakiah Hassan 9 February 2010. Introduction Exchange rates are influenced by interest rates and inflation rates and together, they influence markets for exchange rates in the future, known as forward rates.

E N D

International Parity Conditions By : Madam Zakiah Hassan 9 February 2010

Introduction Exchange rates are influenced by interest rates and inflation rates and together, they influence markets for exchange rates in the future, known as forward rates. Means that, the main determinants of exchange rates are relative inflation rate, interest rates, national income and political stability. The linkages among these variables are called ‘parity conditions’ Parity conditions are key relationship used to predict movements in exchange rates. Since arbitrage plays a critical role in this discussion, we should define it upfront.

Objective Learn how to predict foreign exchange rates using arbitrage arguments.

What is arbitrage Business operation involving the purchase of foreign exchange gold, financial securities or commodities in one market and their almost simultaneous sale in another market, in order to profit from price differentials existing between the markets. Arbitrage generally tends to eliminate price differentials between markets. So, the act of simultaneously buying and selling the same or equivalent assets or commodities for the purpose of making certain profit.

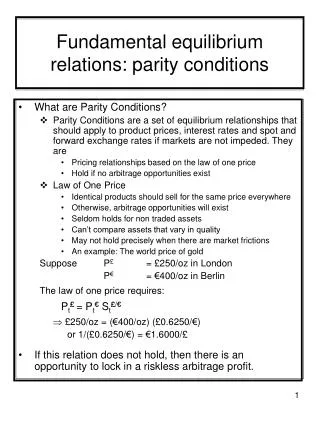

Structure of IPC Purchasing power parity (PPP) and Law of one price (LOP) International Fisher Effect (IFE) Fisher Effect (FE) Interest Rate Parity (IRP) Forward rates as unbiased predictors of future spot rates (UFR)

Diagram of Parity Conditions Exchange Rate Forecasts Unbiased Forward Rate Purchasing Power Parity Forward Rate Premium or Discount International Fischer Effect Differences in Inflation Rates Fisher Effect Interest Rate Parity Differences in Interest Rates

Interrelationship between Parity Conditions The four parity conditions are all inter linked. A change in price level ( inflation rate ) in the commodity market will affect the market interest rate. A change in the market interest rate will then, in turn, affect the future spot rate (IFE) and the forward market through IRP. The four main theoretical relationship among the S, F, P (inf), and I are shown in previous graph.

Purchasing power parity (PPP) and Law of one price PPP is based on law of one price (LOP) and the no arbitrage condition. LOP states : identical goods sell for the same price worldwide Stated that in the absence of transportation cost, taxes and other restrictions, meanwhile the price of a product stated in a common currency such as USD should be the same in every country. This means ‘ same product, same price’’ in one common currency. Since the product is sold in different countries, the product’s price must be stated in different currency terms, but the price of the product should still be the same when expressed in one common currency.

So, PPP states : the exchange rate between two countries’ currencies should be equal to the ratio of their price levels. PPP is a manifestation of the LOP applied internationally to a standard commodity basket.

Purchasing power parity (PPP) (1) Absolute PPP Goods and services should cost the same regardless of the country This simply requires replacing a single product with a price index. Example : if the price index in USD is the price of basket of goods in the US and a price index in AUD is the price of a similar basket of goods in Australia, then : Price index USD = Price index AUD ( spot USD/AUD) Problem : difficult of getting similar basket goods for both countries, because due to each country’s different consumption patterns.

Purchasing power parity (PPP) (2) Relative PPP The exchange rate is expected to adjust in order to reflect expected relative differences in purchasing power. -----the exchange between HC and any FC will adjust of reflect changes in the price levels ( inflation) of two countries.

PURCHASING POWER PARITY 1. In mathematical terms: where et = future spot rate e0 = spot rate ih = home inflation if = foreign inflation t = the time period

PURCHASING POWER PARITY 2. If purchasing power parity is expected to hold, then the best prediction for the one-period spot rate should be

Example PPP US inflation 4% Australia inflation 8% Current spot is USD 0.8034 per AUD Answer : Spot rate = (1 + 0.04) / ( 1 + 0.08 ) * 0.8034 = USD 0.7736 per AUD

THE INTERNATIONAL FISHER EFFECT (IFE) IFE STATES: the spot rate adjusts to the interest rate differential between two countries.

THE INTERNATIONAL FISHER EFFECT IFE = PPP + FE

EXAMPLE IFE • Malaysia interest rate for 6-month 4% • Australia interest rate for 6 month 8% • Current spot rate is MYR2.8735/AUD • What is forecast future spot rate of the MYR/AUD if the interest rate in Australia were rise to 10% p.a? • Future spot rate = 2.8735 [ 1 + 0.04/20] / [1 + (0.1/2)] = 2.7914

Interest Rate Parity (IRP) Theory • IRP focuses on the spot and forward (expected) exchange rates with international money and bond markets. • The parity condition implied by this theory establishes the break-even condition where the return on a domestic currency investment is identical with the return on a foreign currency investment covered against exchange rate risk

EXAMPLE OF IRP Example : Assume that American has USD 1 M to invest either in the UK or USA given the following information: Spot rate USD 1.68/GBP Forward rate USD 1.6066/GBP UK interest rate 13 % p.a USA interest rate 8.0625% p.a

Two alternative : Alternative 1 : invest in USA & get USD 1,080,625 after one year ( 1M X 1.080625) Alternative 2 : Take advantage of the higher interest rate by investing in UK

Alternative 2: • Take advantage of the higher interest rate by investing in UK • IF INVESTOR CHOOSE AT ALTERNATIVE 2, HE MUST PERFORM THE FOLLOWING STEPS: • Step 1: Convert USD 1 Million into pounds at spot rate because bankers only accept pounds. USD 1 Million / 1.68 = GBP 595,238. • Step 2 : Invest GBP 595,238 at 13% after one year. GBP 595,238 X 1.13 = GBP 672,619 • Step 3 : Sell immediately one year forward at forward rate to get back USD GBP 672,619 X 1.6066 = USD 1,080,630. Arbitrage profit = USD 1 M – USD 1,080,630 = USD 80,630

Why doing covered interest rate because to protect against risk that pound will depreciate in one year.

UNCOVERED INTEREST RATE PARITY Example : Suppose that the current one year interest rate in the US is 9.4% and the UK interest rate is 11%. The spot rate is USD1.5 per GBP. • What is expected one year forward rate for USD/GBP? • [ 1 + 0.094] / [1 + 0.11] = f / s • [ 1 + 0.094] / [1 + 0.11] = f / 1.5 • So one year USD/GBP = 1.478

EXPECTATION THEORY OF THE EXCHANGE RATE. • Theory seeks to answer the question: is the forward rate an accurate forecast of future spot rate? • Actually investor want to know whether the forward rate is an unbiased predictor of the future spot rate. • The expectation theory state that forward rate approximately = the expected future spot but does not means they same, because forward rate will, on average, over estimate and under estimate the actual future spot rate. • The rationale behind that is the foreign exchange is reasonable efficient.

Conclusion In this chapter, we learned about five parity conditions or relationship apply to spot rates, inflation rates and interest rates in different currencies: PPP, FE, IFE,IRP and forward rates as an unbiased forecast of the future spot rate or UFR. International trade or exchange of goods and services across borders gives rise to international settlement with payments being made in different currencies. Discrepancies may arise as a consequences when the settlement is executed in one currency as against the other currency. Moreover, economic conditions and changes in economic conditions in different countries may take effect on the value of goods measured in different currencies and the relative values and opportunity costs of these currencies.

International parities are important since they establish relative currency values and their evolution in terms of economic circumstances and cross broader arbitrage may be possible when they are violated.