Download

1 / 42

420 likes | 878 Vues

“China’s factor” --- Recent changes of commodity prices and sea freight rates Feng Lu China Center for Economic Research (CCER) Peking University, Email: fenglu@ccer.edu.cn 20th NBER EASE conference on ""Commodity Prices and Markets" Hong Kong, June 26-27, 2009. Issues discussed

E N D

“China’s factor” --- Recent changes of commodity prices and sea freight rates Feng Lu China Center for Economic Research (CCER) Peking University, Email: fenglu@ccer.edu.cn 20th NBER EASE conference on ""Commodity Prices and Markets" Hong Kong, June 26-27, 2009. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Issues discussed • 1) Recent fluctuations and causes • 2) Understanding “China’s factor” • 3) Challenges and possible adjustments Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

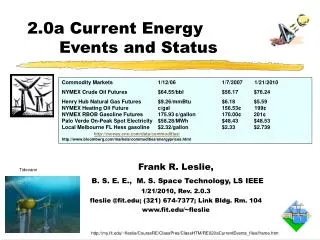

Recent commodity price swings • CRB spot index more than doubled during 2002-08 (from 212 in May 2002 to 476 in Jun. 2008). It fell drastically afterwards to 311 in Feb. 2009, one of the largest falls over the last 60 year or so. It increased by 17% over 3 months period to May 2009. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Swings of CRB sub-indices! • Comparison of major categories of sub-index indicates that metal prices had the largest swings in recent years! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Four metal materials and energy Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

International sea freight rates • Sea freight rates especially that of dry cargos had huge swings. The dry cargo rate index hiked from 95 in Jan. 2002 to 1647 in May 2008, and declined drastically to 90 in Jan. 2008. It bounced back to 255 by May 2009. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Driving forces of market changes • Upward shifts in world demand; • Monetary factors with US dollar; • Financial investors? Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Consumption of selected raw materials • Average growth rate of metal raw materials was to varying degrees higher than the previous period. There was a simultaneous growth of quantity and price! But upward shift of growth rate for crude oil consumption was relatively modest! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Growth of sea transport volume • Sea transport of selected commodities, especially dry-bulk cargos grew particularly strong in recent years! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Growth of sea transport volume • Simple comparison of growth rates during different periods indicates that growth rate of transport volume during 2002-2007 was to varying degrees higher than the previous periods. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Supply constrains tightens! • Shrinking slack capacity for sea transportation suggests very tight supply conditions in recent years in the market. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Demand driven commodity boom! • For some metal material commodities and sea freight rate, the demand growth may a crucial driving force behind the market changes in recent years, bearing in mind that intensity of demand shock differ among sectors! • Since the short run supply curves for the commodities and sea transport were inelastic towards the segment of near full capacity, unexpected demand growth bid up prices and freight rates! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

But crude oil may be another story! • Relative shift of growth rate for crude oil consumption was only modest recently, oil price hike in recent years may be more closely related with supply side factors: • Output reduced by 1.3 mb/d for OPEC-10 in 2006-07; • Long-lead time for creation of new capacity; • Trend decline of oil production in major oil fields in US; • “Above-ground risks” of Political instability and mismanagement in Iraq, Nigeria, Iran and Venezuela etc; • Worry about the ultimate depletion of resources • (James D. Hamilton “Understanding Crude Oil Prices” Dec. 6, 2008) . Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Effects of USD exchange rate change! • Depreciated by 37% during a period of 7 years: from 103.5 in Feb.2002 to 65 in Mar. 2008. • Appreciated by 17% to 76 in Apr. 2009, but depreciated somewhat over recent 2 months or so. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Effects of USD exchange rate change! • Using nominal effective exchange rate (NEER) of USD as deflator, prices of commodities and sea freight rate still increased 2-5 times in recent years! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Fed loose monetary policy • Fed runs the negative real interest rate policy in 2002-2005. Degree of extra-loose monetary policy measured by the negative rate was second only to the late 1970 with the highest inflation in the post-WWII era. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

2002-2007 Loose monetary policy and the dollar glut! • Relative low level of TED spread during 2002-2007 also indicates the dollar glut as a result of the extra-loose money supply! The “liquidity glut” may play a role of “adding fuel to the flames”. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Role of financial investors? • A characteristic of the recent global commodity price swings was that inflow and outflow of huge scale of index investments in commodities went hand in hand with changes in commodity prices! • There was fierce debate about what role has the index investment played in affecting velocity of the commodity market. • Though the impact of the financial investors can easily be exaggerated, the issue deserves close look and fresh investigation in light of the new evidences. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Role of financial investors? • As demonstrated by De Long et al. (1990), if rational speculator’s early buying triggers positive-feedback trading, an increase in the number of forward-looking speculators can increase volatility about fundamentals. • In view of the oligopolistic nature of the market in which a few financial institutions have great influence, it is possible that the unprecedented participation of index investors may have temporarily amplified the move of prices away from the fundamentals. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Role of “China’s factor” • The role of China’s factor may be observed through different perspectives: • 1) China’s contribution to the global demand growth! • 2) Co-movement between China’s sectoral performance and world market swings. • 3) The indirect impact of China’s productivity revolution. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Growth of China consumption demand • Driven by rapid industrialization and urbanization, growth of China’s consumption of selected commodities has accelerated, both in absolute volume and share in the world, in the recent years. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Growth of China consumption demand • Average growth rate of three metal materials and crude oil was to varying degrees higher than the previous periods. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

China’s growth of sea trade volume • China’s contribution to the world growth of sea traded volume of imports and exports were in average 43% and 20% respectively during 2002-2007. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

China’s growth of steel production • China steel output increased from 182 million tons to 489 million tons, by 307 million tons during 2002-2007, contributing to 70% of the global growth of steel output (440 million tons) during the period. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

China’s share of incremental copper and aluminum consumption The average ratios of China’s contribution to the world consumption growth of copper and aluminum were estimated at 51% and 56% respectively during 2001-2007. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

China’s share of incremental iron ore and crude oil consumption The average ratios of China’s contribution to the world consumption growth of iron ore and crude oil were estimated at 89% and 33% respectively during 2001-2007. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Co-movements of commodity prices and China’s industrial activity • Up and down of CRB metal price have gone hand in hand with trajectories of China’s industrial activities as well as China’s steel production! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Sea freight rate and China’s import! • There are some elements of co-movement between changes in China’s imports and sea freight rate for dry cargos. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Indirect impact of China’s productivity revolution! • China’s productivity growth in tradable sector with less flexible EX system produces two effects for US: trade effects in dampening inflation, capital effects in dampening interest rates! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

A new macro-economic pattern in US • Usually dual deficits was inversely related with trend changes of long-term interests and/or CPI in USA, but new pattern of persistent worsening of dual-deficits with relatively low CPI and declining interest rate evolved during 2001-2006. • The dual benign effects of China’s productivity revolution serve as one of the multiple factors shaping this new pattern! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Challenges and problems • Wide fluctuation in commodity and transport markets driven by multiple factors including China’s demand presents problems to the growth of the Chinese economy: • 1) Macro-economic instability, • 2) Welfare effect from worsening TOT, • 3) International relationship problems, Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Macro-economic stability effects • It leads to import price hike that in part transmits into the pressure of overall price increase and the so-called “imported inflation pressure”. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Import price hike for primary goods • Import price of all 4 categories of primary materials have increased, with minerals and oil witnessing the highest growth both in import volume and price. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Worsening terms of trade! • The total estimated welfare lose from worsening TOT during 2003-2008 exceeds 1 trillion RMB, about 10% of total GDP growth during the period. The lose in 2008 was 478.9 billion RMB, about 15% of GDP growth that year! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Challenges and problems • Continuous disputes over pricing of iron ore with the international oligopolistic suppliers; • Growing tension over the issue of building natural gas pipe-line from Russia to China. • Controversies over China’s firm bids in acquiring equity of resource firms in foreign countries. • ……. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Possible channels of adjustment • Hopefully, the shocks and imbalances in the markets will be eventually absorbed and adjusted through various channels. • 1) Responses from supply side ; • 2) Improvement on financial regulation; • 3) Encourage China’s firms to “go abroad”; • 4) Enhancing macro-economic stability; • 5) Adjustments in the very long run; Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Supply side adjustments? • Growth of new ship building may eventually equilibrate the market and accommodate the new demand for sea transport. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Supply side adjustments? • Non-ferrous sector investment of exploration budgets increased from about $2 billion in 2002 to more than $13 billion in 2008. • In 2005, Saudi Arabia started to implement an ambitious five-year, $129-billion energy investment plan, nearly $60 billion of which will be directed toward increasing upstream petroleum capacity to an estimated 12.5 million bbl/d by 2009. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Strengthening financial regulation • Appropriate measures of financial regulation may help in reducing the detrimental impacts that excessive financial investment may impose on commodity market. • A recent UNCTAD report: “regulators need access to more comprehensive trading data and make sure the trade is in order …… to ensure that positions on currently unregulated over–the-counter markets do not lead to ‘excessive speculation’”. • Many experts advocate that OTC derivatives trade should be regulated and they should be conducted on the exchange and through central clearing party (CCP). Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

The “going abroad” strategy? • “Going abroad policy” in China received more emphasis in recent years. Investments in foreign resource countries are expect to improve the situation: • To increase investment in industries so to expanding production capacity, and diversify portfolio of China’s net international position. • To strengthen coordination between downstream manufacturing firms inside China and upstream raw materiel producers abroad. • So far the policy has been implemented with a lot of difficulties, generating controversies in China! Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Achieving stable macro-economic environment! • More stable macro-economic environment with more balanced growth model is helpful to controlling drastic demand hike for imported commodities and avoiding steep segment of short-run marginal cost curve in world market. • To stabilize economy in an growing open environment, reforms are needed to liberalize interest rate, allow for more flexible exchange rate for RMB, introduce the inflation-targeting system, so as to provide new macro-management framework. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009

Adjustments in very long run! • In the long run, China has to make the best efforts to find alternative energies so as to gradually substituting for fossil energy. • As China’s per capita stocks of metal materials including steel, aluminum, copper increases, the demand for the new commodities may gradually diminish and approaches the more matured state observed in the developed countries. Conference on commodity markets, Hong Kong, Jun. 26-27, 2009