Download

1 / 2

20 likes | 58 Vues

Did you know that any proposed works at your home need to be notified to your insurers before they commence? http://www.advantageuk.net/

E N D

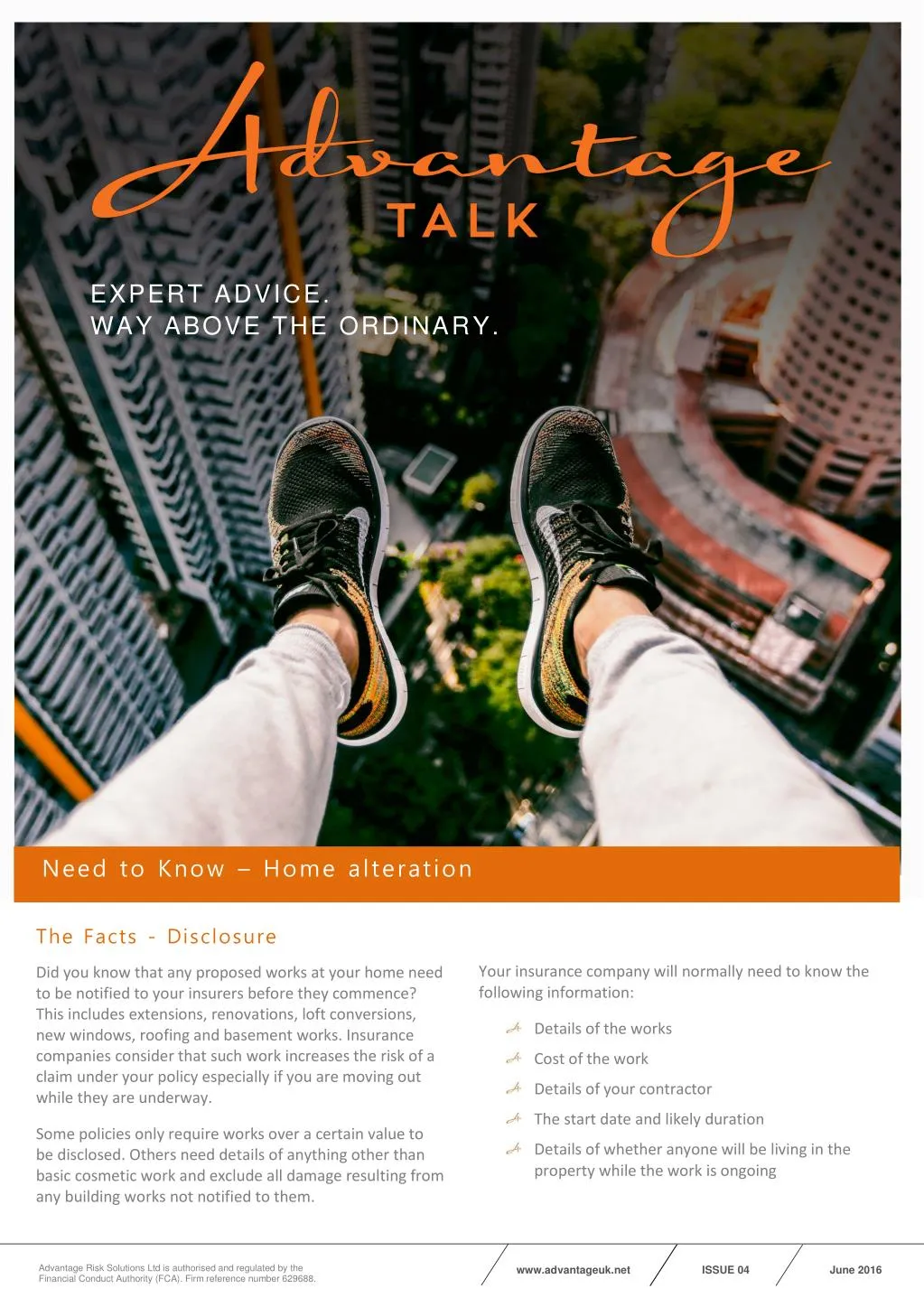

EXPERT ADVICE. WAY ABOVE THE ORDINARY. Need to Know – Home alteration The Facts - Disclosure Your insurance company will normally need to know the following information: Did you know that any proposed works at your home need to be notified to your insurers before they commence? This includes extensions, renovations, loft conversions, new windows, roofing and basement works. Insurance companies consider that such work increases the risk of a claim under your policy especially if you are moving out while they are underway. Details of the works Cost of the work Details of your contractor The start date and likely duration Some policies only require works over a certain value to be disclosed. Others need details of anything other than basic cosmetic work and exclude all damage resulting from any building works not notified to them. Details of whether anyone will be living in the property while the work is ongoing Advantage Risk Solutions Ltd is authorised and regulated by the Financial Conduct Authority (FCA). Firm reference number 629688. www.advantageuk.net ISSUE 04 June 2016

RELAX, WE SPEAK PLAIN ENGLISH If you are directly employing the various sub-contractors yourself e.g. separate contracts with the builder, electrician, plumber and roofer, you will also need to ensure you have cover for the works and the existing structure with the same insurer so that as each contractor signs over their works to you and it forms part of the existing structure, cover is seamless. JCT contracts Insurers will also want to know whether you are entering into any form of contract with the contractor. JCT standard forms of building contracts contain clauses which confirm who is responsible for arranging insurance of both the works and the existing structure. What will an insurer do? They can also stipulate how cover is to be arranged; some contracts require the existing structure to be insured in the joint names of you and the contractor. This will prevent insurers being able to claim from the contractor if he causes damage to the existing structure. Others require a minimum level of cover to be arranged either on the works or on the existing building. e.g. fire and the full range of perils including accidental damage. For extensive works, it is possible that your household insurer will restrict cover quite dramatically. Limiting cover to fire, lightning, explosion and aircraft is not unusual. In addition, various conditions may apply such as requiring the services to be disconnected and the water system drained, regular inspections inside and out, certain security measures to be taken and controls to be implemented regarding the use of heat by contractors, just to name a few. Before you sign anything, you should check with your insurance adviser that the cover you are required to arrange is going to be possible to ensure that you are not left exposed. Is wider cover available? Insurance of the works Should your household insurance prove too restrictive for your needs, wider cover may be available under a specialist renovation policy. Cover can be arranged for the existing structure only or the existing structure including the works. Many homeowners rely on their contractor to insure the works. However, if you want to control the claims process and have the claim paid to you rather than your builder following a loss, you should consider arranging cover yourself. Want to know more? Let’s talk: t. 01256 483969 e. hello@advantageuk.net Any views or opinions expressed in this briefing are for guidance only and are not intended as a substitute for appropriate professional guidance. We have taken all reasonable steps to ensure the information contained herein is accurate at the time of writing but it should not be regarded as a complete or authoritative statement of law. Advantage Risk Solutions Ltd is authorised and regulated by the Financial Conduct Authority (FCA). Firm reference number 629688. www.advantageuk.net ISSUE 04 June 2016