Download

1 / 24

240 likes | 267 Vues

DSBD Perspective on the Proposed Red Tape Impact Assessment Bill Presentation to the Portfolio Committee 15 FEBRUARY 2017. Presentation Structure. PURPOSE BACKGROUND RED TAPE A GLOBAL CHALLENGE INITIATIVES TO REDUCE RED TAPE COMMENTS ON SOME CHAPTERS AND SECTIONS OF THE BILL

E N D

DSBD Perspective on the Proposed Red Tape Impact Assessment Bill Presentation to the Portfolio Committee 15 FEBRUARY 2017

Presentation Structure • PURPOSE • BACKGROUND • RED TAPE A GLOBAL CHALLENGE • INITIATIVES TO REDUCE RED TAPE • COMMENTS ON SOME CHAPTERS AND SECTIONS OF THE BILL • OVERALL PERSPECTIVE ON THE PROPOSED BILL

Purpose The purpose of this presentation is to provide the perspective of the Department of Small Business Development (DSBD) on the proposed Red Tape Impact Assessment Bill as tabled to the Portfolio Committee (PC) on 15 February 2017 by the Democratic Alliance (DA).

2. Background 2.1The Bill has been introduced in the National Assembly and published in Government Gazette No. 39907 of 7 April 2016. It will apply to all organs of State, members of Parliament and Committees of Parliament and self-regulatory bodies. 2.2 The Bill seeks to provide for the assessment of regulatory measures developed by executive, legislatures and self-regulatory bodies in order to determine and reduce red tape for businesses. It further seeks to provide for the establishment of Red Tape Impact Assessment (RIA) Units.

3. Red Tape: A Global Challenge 3.1 There are indications that unduly strict regulations often harm SMMEs and Co-operatives specifically emerging enterprises within the different sectors. The government recognises this issues, as highlighted in the National Development Plan (NDP), that the policy and regulatory environment needs to be coordinated and simplified in order to grow the economy. 3.2 The unfavourable regulatory environment with its high costs and risks of doing business does not only affect SMMEs and Co-operatives but also discourage investment, trade and economic growth; impedes innovation and potential job creation. 3.3 Governments all over the world encounter challenges with regards to designing regulatory systems that are beneficial to the business community and society at large. On the other hand it is also recognised that regulations that are adequately designed promote economic growth and welfare by addressing market failures and enhance competitiveness (OECD, 2015).

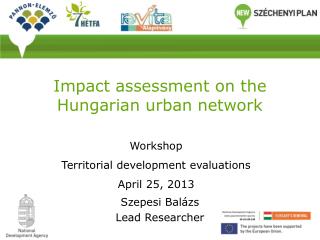

3a. Red Tape: A Global Challenge 3.4 According to the World Bank study (May, 2015) which focuses on measuring the cost of red tape: “If governments of 90 economies had applied best practice in regulating business entry in 2012, more than 45 million days of entrepreneurs’time could have been saved. Around 74 million days could have been saved in transferring property, around 207 million days in importing and exporting, around 468 million days in resolving commercial disputes through the courts and around 772 million days in preparing, filing and paying business taxes.” 3.5 The above highlights the burden placed on the business community by government regulations that depart from some of the best practices. 3.6 The World Bank further stipulates that the gap between best practices and countries' actual practices in business regulation suggests that these firms in 90 economies could have saved $ 180 billion in 2012, if more efficient sets of business regulations were effected.

Improving Business Registration/Entry World Bank, 2015

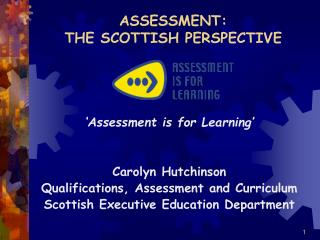

SBP 2004 study on red tape 71% More difficult

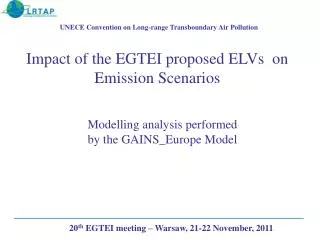

Ways of avoiding/reducing regulatory compliance costs – SBP 2014 study

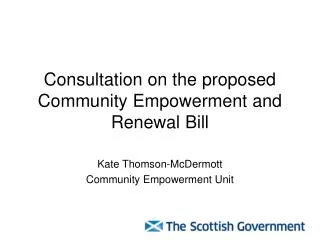

International best practice for improving business registration http://en.wikipedia.org/wiki/Single-window_system

4. DSBD INITIATIVES TO REDUCE RED TAPE 4.1 One of the strategic goals of the Department of Small Business Development (DSBD) is to create an enabling environment for competitive SMMEs and Co-operatives. In fulfilment of this goal, the DSBD within the 2016/17 financial year will conclude a Study, done in partnership with the Department of Planning, Monitoring and Evaluation (DPME), on legislative and regulatory protocols impeding SMMEs and Co-operatives within the national sphere of government. 4.2 The Study will highlight priorities for reform and develop an efficient and effective framework to address relevant national laws and regulations. 4.3 The DSBD is also conducting the assessment of the existing red tape reduction guidelines which was introduced as a practical implementation framework to reduce municipal red tape for the enhancement of SMMEs and Co-operatives. Priority procedures for amendment will be addressed in 2017/2018 financial year.

4a. DSBD initiatives to reduce red tape 4.4 In the 2017/2018 financial year the research focus will be on legislative and protocols impeding SMMEs and Co-operatives 4.5 Improved coordination amongst governmental stakeholders across all spheres of government to strengthen cooperation and shared vision to reduce regulatory burdens and ensure optimal conducive environment for SMMEs and Co-operatives 4.6 30-Day Payment Hotline: operated by seda in partnership with DPME. 2016 Report revealed a significant tunraround in resolving the payments to SMMEs. Over the period July 2013 to October 2016 the service facilitated payments of invoices to the value of R82.8m out of R 353.4m. 4.7 FinFind: A web-based one-stop-shop solution to improve access to finance. Assists SMMEs to become finace ready through access to expert advice

4c. Other Government Interventions 4.8 Socio-Economic Impact Assessment System (SEIAS): Managed by DPME became compulsory with effect 1 April 2015 before any bill or policy is considered by Cabinet. 4.9 SARS has introduced special SMME units. Impact: Additions 18 000 tax compliant SMMEs 4.10 Dept. of Environmental Affairs: Rapid Environmental Impact Assessments 4.11 InvestSA: Established a specialised Unit with officials seconded from regulatory departments to ease the environment for local and foreign investors

5. Comments on some of the chapters and sections of the bill 5.1 The Bill is limited to red tape reduction and does not include requirements in terms of compliance Parliamentary Protocols and the Intergovernmental Relations Framework Act. 5.2 Chapter 1: refers to “Minister” and is defined as “the Minister responsible for Small Business Development”, yet the Bill does not make reference to or include the definition of Small Business and Co-operatives as outlined in the National Small Business Act,1996 as amended or Co-operatives Act of 2005 as amended. This is imperative as the Bill proposes the Minister responsible for Small Business Development as the overseer of the legislation. 5.3 Chapter 1: “Organs of State” refers to national sphere of government that is developing or administering a regulatory measure, however there are also provincial and local government structures that develop and administer regulatory measures leading to provincial acts and regulations and municipal by-laws.

5a. Comments on some of the chapters and sections of the bill 5.4 Chapter 1: The Bill defines red tape as “information to be submitted or maintained and the procedures required to gain administrative approval or to comply with prescribed requirements….”, i.e. limiting red tape to (a) the need to submit information and (b) to comply with certain procedures. The definition of red tape is thus limiting and does not cover the full scope of red tape and its negative implications to especially SMMEs. 5.5 Chapter 2: The Bill requires the Minister to establish a unit in the Department to be known as the Red Tape Impact Assessment Unit. Reference is also made to a Regulatory Impact Assessment (RIA) unit as well as the establishment of provincial RIA units. This will require substantial additional human and financial resources to ensure compliance with the stated functions.

5b. Comments on some of the Chapters and Sections of the Bill 5.6 Chapter 2: The establishment of the proposed red tape impact assessments unit and or RIA units will duplicate work currently being performed by the DPME Socio Economic Impact Assessment Systems(SEIAS) process, the SEIAS Interdepartmental Steering Committee and DSBD programmes aimed at reducing red tape. The capacity has already been created within government to control and reduce the economic impact of regulatory measures through. In addition to SEIAS the DSBD already has programmes aimed at reducing red tape on all spheres of government. 5.7 Chapter 2 (8) :The RIA Units will prepare detailed reports on red tape that also cover information on the total indirect costs, substantive costs per regulatory measure or procedure and overall costs for the period. The direct and indirect costs for red tape will differ from case to case and it will not be possible to do accurate calculations of the costs. The importance is not do determine the costs but to ensure that all unnecessary cost burdens are reduced and eliminated.

5e. Comments on some of the chapters and sections of the bill 5.8 Chapter 3: The Bill is silent on SEIAS. Given the technical nature of legislation the assessment of possible regulatory burdens (limited to cost and information burdens in terms of the proposed Bill) will best be done in consultation with the drafters of the proposed legislation which is currently already required in terms of SEIAS. 5.9 Chapter 3 (1): If it is determined that a proposed legislation may impose unintended cost or information burdens a full red tape impact assessment must be conducted. The timeframe allowed for the full red tape impact assessment is 30 days. Exemptions from the 30 day time frame requirement may again only be provided by the Minister after consultation.

5e. Comments on some of the chapters and sections of the bill 5.10 Chapter 4:Provides for all legislation to be vetted by DSBD to consider and advise on its impact on small business. It furthermore requires that all past (existing) legislation and secondary legislation (regulations) must be reviewed within a period of two years. Between 1994 and 2014 more than 1 200 Acts were promulgated. Each Act is founded on a policy and has accompanying regulations where most areas of red tape can be found. The target may be difficult to achieve within the two year period as proposed by the Bill. 5.11 Chapter4:Different timeframes are proposed within the Bill, the memorandum refers to five years whilst chapter 5 clause 15(2)(c) refers to two years for activities. This clause states that after two years at least one piece of identified legislation must be repealed or replaced. The processes required for each time frame should be more clearly set out. The objective of reaching 25% of existing legislation within five years will be more difficult to achieve if after two years, only one piece of legislation must be fully addressed

5f. Comments on some of the chapters and sections of the bill 5.12 According to our definition, Red Tape is not limited to the provisions in the Act or regulations. It includes inefficient procedures and systems related to administrative management thereof which the Bill has not adequately addressed. Other administrative burdens relate to regulatory costs in the form of asking for permits, filling out forms, and reporting and notification requirements for the different government departments at national, provincial and the locals.

7. Summary: DSBD perspective on the proposed bill 7.1 The cover of the Bills deems it to be the Red Tape Impact Assessment Bill but in the body of the Bill it is called the Red Tape Reduction Bill. This is confusing 7.2 The definition provided for Red Tape is limiting and needs to be enhanced to cover the full scope of red tape. 7.3 The Bill promotes a silo approach rather than a focus on the entire ecosystem. As such the Bill is limited to assessing the cost of red tape. 7.4 The existence of numerous legislation and related regulation developed and administered within the three spheres of government requires the Bill to consider administrative simplification. 7.5 The Bill raises limited co-ordination among the three spheres of government as one of the major issues for consideration including government agencies. Internationally the provision of e-government services is continually being considered through different access points.

7a.Overall perspective on the proposed bill 7.6 The Bill needs to consider international trends including facilitating compliance as an important element or tool, especially regarding support of compliance to SMMEs and Co-operatives. 7.7 Assistance to businesses in overcoming red tape challenges is not adequately outlined within the Bill and intensive stakeholder consultative processes is still required including Business Chambers 7.8 The Bill is silent on the general provision of Chapter 4 of the current Small Business Act 29 of 2004 that enables the Minister to, “by notice in the Gazette, publish guidelines for organs of state in national, provincial and local spheres of government to promote small business. 7.9That the Department is allowed time to fast-track the revised definition in the NSBA in order to promote policy coherence

Thank you! Re a leboga!