Download

1 / 8

80 likes | 175 Vues

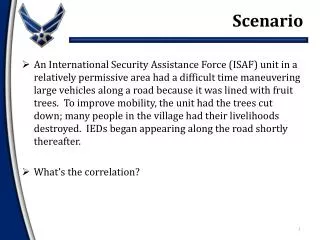

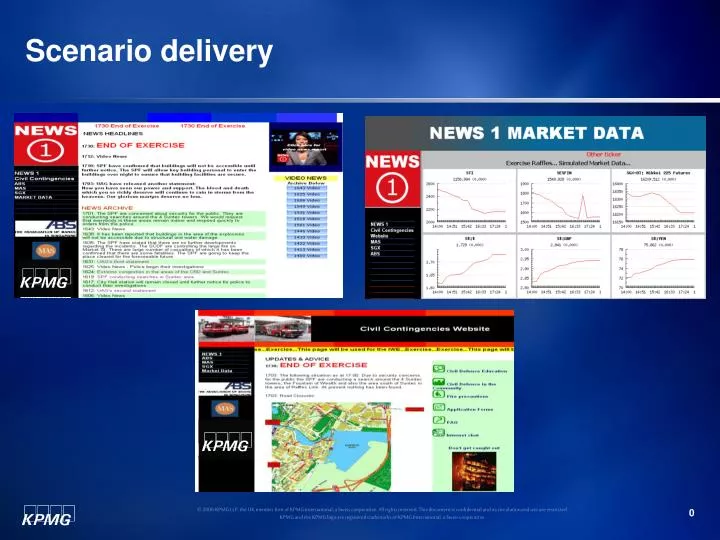

Scenario delivery. Exercise scenario cell. Exercise Director. Logistics Manager. Scenario Cell Manager. Facilitators’ Liaison Manager. Facilitators’ Liaison Team. Logistics Team. Injector Cell. Civil Authorities MHA SCDF SPF LTA. SGX Cell. Journalist Cell. MAS Cell.

E N D

Exercise scenario cell Exercise Director Logistics Manager Scenario Cell Manager Facilitators’ Liaison Manager Facilitators’ Liaison Team Logistics Team Injector Cell Civil Authorities MHA SCDF SPF LTA SGX Cell Journalist Cell MAS Cell

Post-exercise • Participant ‘on-the-day’ poll • Press conference • Detailed debrief questionnaire • Report

Key learning points – crisis response • Markets expect regulators to take a lead • Regular, effective communications are vital to support market stability and maintain market confidence • Critical information to be retrieved from the financial institutions, so the extent of damage is assessed • Co-ordination within the financial industry and with emergency services is essential • Business continuity is not only an information systems issue, but also a human resources issue

Why does sector-wide resilience matter? • Financial system highly interconnected • All financial markets participants are dependent upon the ability of counterparties to make payments and settle transactions • Borrowers need lenders • Buyers need sellers • Financial infrastructure providers underpin the system • Does not make sense to plan in isolation • [From a presentation by David Strachan, Sector Leader Financial Stability, Financial Services Authority, March 2007]

Why does cross-border resilience matter? • Events in UK markets have global ramifications and vice versa • Crucial that international regulatory community can respond in a coordinated and effective way to global disruption • Actions taken internationally need to be mutually reinforcing • [From a presentation by David Strachan, Sector Leader Financial Stability, Financial Services Authority, March 2007]

Conclusions • “KPMG's paper rightly concentrates upon firm-specific issues as the essential building block for improving resilience • But it also highlights the importance of thinking and engaging more widely across the UK financial sector and across borders” • “At the FSA we believe that the work we have undertaken in cooperation with key firms on benchmarking and testing has contributed – and will continue to contribute – to enhancing sector-wide resilience • Our key priority going forward will be to strengthen the ability of authorities to respond effectively to major cross-border events” • [From a presentation by David Strachan, Sector Leader Financial Stability, Financial Services Authority, March 2007]

Presenter’s contact details Rick Cudworth Partner, KPMG LLP (UK) Service Leader, Business Continuity +44 (0)7715 704805 Rick.Cudworth@kpmg.co.uk www.kpmg.co.uk