Download

1 / 17

170 likes | 295 Vues

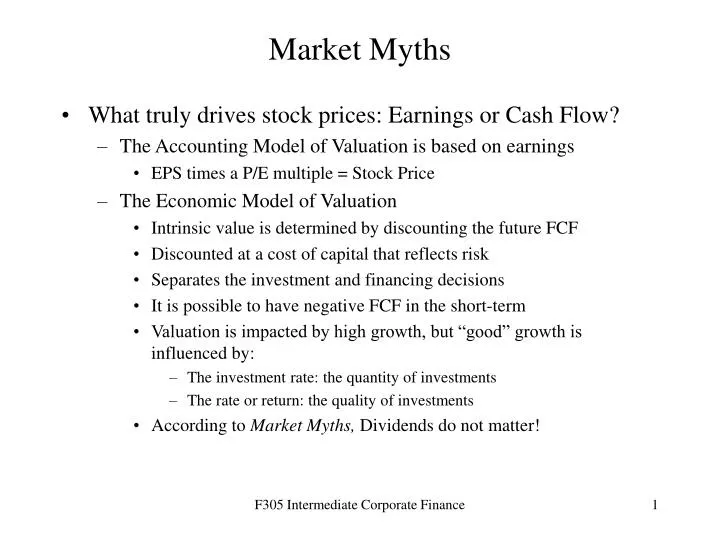

Market Myths. What truly drives stock prices: Earnings or Cash Flow? The Accounting Model of Valuation is based on earnings EPS times a P/E multiple = Stock Price The Economic Model of Valuation Intrinsic value is determined by discounting the future FCF

E N D

Market Myths • What truly drives stock prices: Earnings or Cash Flow? • The Accounting Model of Valuation is based on earnings • EPS times a P/E multiple = Stock Price • The Economic Model of Valuation • Intrinsic value is determined by discounting the future FCF • Discounted at a cost of capital that reflects risk • Separates the investment and financing decisions • It is possible to have negative FCF in the short-term • Valuation is impacted by high growth, but “good” growth is influenced by: • The investment rate: the quantity of investments • The rate or return: the quality of investments • According to Market Myths, Dividends do not matter! F305 Intermediate Corporate Finance

Evidence in Favor of the Economic Model • Companies switching to LIFO experience a 5% increase in price at the time of announcement • The stock prices of companies that make acquisitions through asset purchases are not penalized vs. companies that perform a “Pooling” F305 Intermediate Corporate Finance

Why Earnings, EPS and Earnings Growth are Misleading Measures of Performance • If valuation is based on discounted free cash flow, why is there such as strong reaction to earnings pronouncements? • Earnings and cash flows, while distinct and different, are nonetheless closely linked • Accounting statements provide historical perspective • They serve as the starting point for financial analysis • Most investors pay close attention to company financial pronouncements! F305 Intermediate Corporate Finance

Pro-Forma Financial Reporting • Companies provide pro-forma results in addition to those filed with regulatory agencies • Often strip out one time charges and expenses • Restructurings • Stock-option expenses • Write-downs for impairment issue • Motorola • 15 consecutive quarters with a special item reported! • Since 1999, adjustments total $11.3 billion • Do these reflect the normal course of business or not? F305 Intermediate Corporate Finance

Pro-Forma Financial Reporting • Other pro-forma “tricks” • Pension fund accounting • Loans to customers • The “big bath” This just names a few of the techniques used to potentially mislead investors! F305 Intermediate Corporate Finance

Accounting for Stock Options • The impact of options are currently excluded by most companies • How are options currently accounted for? • The impact of options appears in a footnote to the financials • Profits to employees are taxed as ordinary income • Exception for incentive stock options if the stock is held for one year after the option is exercised. Most options are not this type • If taxed as ordinary income, they provide a deduction for the company as compensation expense • Compensation is calculated by subtracting the exercise price from the market price of the options on the first date on which are known both • the number of shares the employee is entitled to receive • the option or purchase price F305 Intermediate Corporate Finance

Accounting for Stock Options • But what happens is subsequently the stock price drops? • FASB proposal in 1993 was to calculate the value of the options (perhaps using Black-Scholes) and expense them over the vesting period. This was rejected and the disclosure was relegated to the footnotes • Value of the options depend on the stock price, the option strike price and time to maturity (and other B-S variables) F305 Intermediate Corporate Finance

Dilution: The “Other Expense” • Fully diluted EPS reflects only those stock options that are “in the money” • Could exclude many options! F305 Intermediate Corporate Finance

Inconsistent Reporting – Challenges in Comparing Statements • Winn-Dixie and Boeing deduct the estimated value of employee stock options from income each reporting period • If Starbucks did the same, net income would have been reduced in 2001 by 30% • At Cisco, net income would have been reduced by 42% YTD through July • UPDATE! • Many companies this summer decided to start expensing options in light of accounting scandals including, Cinergy, Bank One, GM, Proctor and Gamble, Coke, GE and Amazon • These announcements and the expensing of the options did not have a negative impact of the per share price! • Do investors already take these expenses into account? F305 Intermediate Corporate Finance

Inconsistent Reporting – Challenges in Comparing Statements • K-mart and Target call the year ending 1/31/01 2000. Wal-Mart calls it 2001 • Amazon excludes net interest expense from pro-forma results. Most companies do not • Amazon actually reported two different pro-forma results for the first quarter of 2001. A loss of $49M and a loss of $76M. According to GAAP, their loss was $234M F305 Intermediate Corporate Finance

Four “Tricks of the Trade” • The Big Bath • Vendor Financing • Pension Funds Gains • Timing of Revenue and Expense Recognition F305 Intermediate Corporate Finance

The Big Bath • Make a bad year worse, in order to improve the future • On April 16, 2001 Cisco announces a $1.2B charge for laying off workers, closing buildings and re-valuing Goodwill • At the same time, announce a $2.5B inventory write-off, primarily raw materials • Announce large write-offs just prior to a merger to prop up post-acquisition results F305 Intermediate Corporate Finance

Vendor Financing • Motorola • On Feb 3, 2000, Motorola announced a $1.5B order to Telsim, Turkey’s #2 Wireless Telephone carrier • In SEC filings made March 30, they disclosed loans to the same company totaling $1.7B • In October 2001, Motorola reported a 3rd quarter pro-forma loss of $153M • After including charges for impaired investments, cost reduction activities and increasing reserves for the Turkish company Telsim, the company reported a loss of $1.4B! F305 Intermediate Corporate Finance

Vendor Financing - Motorola Update! • Motorola not alone - Nokia did basically the same transactions for $700M • Motorola (and Nokia) are now suing in federal court in Manhattan • “Every indication is the the defendants, behind a façade of legitimacy, engaged repeated acts of fraud and chicanery, and thereby perpetrated and continue to perpetrate a rather massive swindle!” • Whatever happened to “due diligence”?? • “I doubt they are going to recover any meaningful amount of money” • Woytek Uzdelewicz, Bear Stearns telecom analyst F305 Intermediate Corporate Finance

Pension Fund Gains • In 2000, 1.7% of pre-tax income for IBM was the result of changing the assumption for their expected rate of return on pension fund investments from 9.5% to 10% • General Electric reported that 9% of its earnings in 2000 were from Pension plan profits (that is 2.5 times more profit than their appliance division reported!) • According to Goldman Sachs, 35 companies in the S&P 500 reportedly received 10% or more of their earnings from Pension funds • Companies are raising expected returns from investment plan investments at the very time when investment returns in general are falling • According to Warren Buffet, “I think anyone choosing not to lower assumptions is risking litigation for misleading investors” F305 Intermediate Corporate Finance

The Timing of Revenue and Expense Recognition • Change asset lives to reduce the depreciation deduction • Readers Digest Association Inc. revised their bad debt assumptions to the tune of $.16 per share in December 2000 • Verizon Wireless Inc. amortizes the costs of wireless licenses over the course of 40 years because they are renewable – but what about technological obsolescence • Computer Associates International reported EPS of $.42/share in pro-forma statements, but a loss of $.59/share in its GAAP statements based on their treatment of terms in their software sales contracts F305 Intermediate Corporate Finance

The Pay-off: The case of AOL • AOL deferred the marketing expense of sending out millions of computer disks to potential customers • By capitalizing these costs instead of expensing them, AOL boosted profits • AOL pays a small fine and re-states prior years earnings in May 2000 • AOL is able to merge with Time Warner to create AOL Time Warner in January 2002 • AOL Time Warner announces largest write-off ever in January 2002 F305 Intermediate Corporate Finance