Download

1 / 14

300 likes | 957 Vues

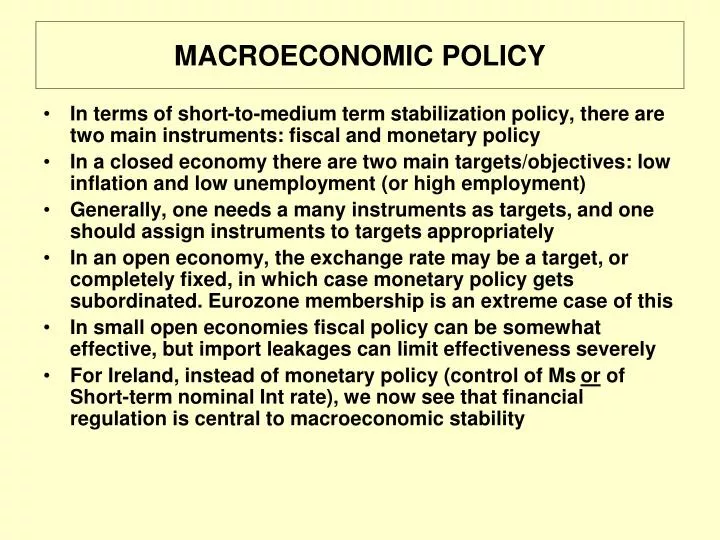

MACROECONOMIC POLICY. In terms of short-to-medium term stabilization policy, there are two main instruments: fiscal and monetary policy In a closed economy there are two main targets/objectives: low inflation and low unemployment (or high employment)

E N D

MACROECONOMIC POLICY • In terms of short-to-medium term stabilization policy, there are two main instruments: fiscal and monetary policy • In a closed economy there are two main targets/objectives: low inflation and low unemployment (or high employment) • Generally, one needs a many instruments as targets, and one should assign instruments to targets appropriately • In an open economy, the exchange rate may be a target, or completely fixed, in which case monetary policy gets subordinated. Eurozone membership is an extreme case of this • In small open economies fiscal policy can be somewhat effective, but import leakages can limit effectiveness severely • For Ireland, instead of monetary policy (control of Ms or of Short-term nominal Int rate), we now see that financial regulation is central to macroeconomic stability

POLICY ACTIVISM VERSUS RULES • The Keynesian approach as traditionally understood was activist: use fiscal policy to stabilize aggregate demand and counter macroeconomic shocks • The reaction against Keynesianism in the 1960s was based on two things: • its lack of success in dealing with an emerging inflation problem • problems such as imperfect information and time lags • We concentrate on the latter point which is a general one: it applies to monetary as well as fiscal policy • An activist monetary policy would seek to lower interest rates or expand the money supply in response to a forecast or actual fall in aggregate demand. • Similarly an activist fiscal policy would seek to change taxes and/or government expenditures in response to demand shocks

LAGS IN POLICY RESPONSE (1) • Suppose there is a fall in aggregate demand which occurs at a certain time t • This becomes apparent only when date for time t are available (data lag – say 1 to 3 months) • Do the data represent only a blip or something more enduring? (recognition lag - another 1 or 2 months?) • Response: a fiscal response may require legislation. Some taxes are difficult to adjust between fiscal years; expenditure adjustments are slower – Ireland 2009/10. (Legislative lag – 3 to 12 months?) • Transmission: decision on budget day may not take effect for several months (Transmission lag, 2 to 6 months?) • Final effect: for example changes in Ms affect real output with a long and variable lag (Effectiveness lag: up to 2 years)

LAGS IN POLICY RESPONSE (2) • For monetary policy, the data, recognition and effectiveness lag can sum to 2+ years. For fiscal policy, the data, recognition and legislative lags can sum to 18 months to 2+ years • There is also evidence for the USA that in the case of Monetary Policy • (a) the lags have got longer • (b) the effect on real GDP of a given change in Interest rates has got smaller • Much of this is specific to the USA, but even if Eurozone monetary policy were as effective as the USA 1961-75, less than half the effect would have occurred within a year. • These problems have lead to: • (a) analysis of the time-inconsistency problem • (b) a focus on policy rules, especially the Taylor Rule • (c ) fiscal policy: the EU Growth and Stability Pact

RESPONSE OF USA GDP TO 1% INCREASE IN SHORT-TERM INTEREST RATE

TIME-INCONSISTENCY • A highly discretionary policy carries the danger of Time-Inconsistency • Time Inconsistencydescribes the temptations of policy makers to deviate from a policy after it is announced and private decision makers have reacted to it • e.g. one implements a restrictive monetary policy to lower inflation and inflationary expectations • After a year or so inflation starts falling but unemployment has risen • The policy is then reversed, before the full longer-term benefits are realised • This gives rise to problems about the credibility of policy activism

THE TAYLOR RULE AND MONETARY POLICY • Monetary policy has two main objectives: low inflation and low unemployment. There are obvious short-to-medium tem trade-offs. • The economist John Taylor (1996) has proposed a rule for Central Banks, whereby short-term (T-bill) rates respond to (a) the gap between actual/forecast inflation and some target inflation rate (b) the gap between actual/forecast unemployment and some target rate (the “natural” rate) • The monetary authorities set i*, where i* = r + • The monetary authorities have targets for: • (i) the real interest rate, r and an estimate of equilibriumr* • (ii) the inflation rate, * • (iii) real GDP, Y* (= “natural” or full-employment GDP); Y/Y* = target output ratio = 1

THE TAYLOR RULE • r = r* + ( – *) + log(Y/Y*) and i* = r + • So: i* = + r* + ( – *) + log(Y/Y*) • Suppose r* = 0.03, Y = Y* so (Y/Y*) = 1, * = 0.02, = 0.06; = = 0.5 • then: i* = 0.06 + 0.03 + 0.5(0.06 – 0.02) = 0.11 • Short-term nominal interest rate is 0.11 or 11% • But suppose (Y/Y*) = 0.9 i.e. recession • then: i* = 0.06 + 0.03 + 0.5(0.06 – 0.02) + 0.5 log(0.9) = 0.11 – 0.5(0.046) 0.085 or 8.5% • Suppose = 0.01, (Y/Y*) = 0.9 • then: i* = 0.01 + 0.03 + 0.5(0.01 – 0.02) – 0.5(0.046) 0.035 – 0.5(0.046) 0.01 or 1% • Do Central Banks follow a Taylor Rule? • Should Central Banks target Asset Prices? Efficient Markets Hypothesis suggests not: but recent experience says otherwise

FISCAL RULES: EU STABILITY AND GROWTH PACT (1) • The Keynesian revolution pointed to fiscal policy activism rather than fixed rules. • Fundamental insight: a Budget which is “balanced” year by year implies pro-cyclical fiscal policy. • The EU stability and growth pact (1997) had two main features: • (a) general budget deficit not to exceed 3% GDP • (b) public debt not to exceed 60% GDP (or to be convergent downwards towards 60%) • Basic objective: to achieve a degree of fiscal discipline in Eurozone which would avoid any undermining of EMU • Problem: a too rigid approach, which could lead to counter-cyclical fiscal policies. • However more “flexible” approaches were perhaps seen as giving too much scope for fudging.

FISCAL RULES: EU STABILITY AND GROWTH PACT (2) • The 2005 reforms to the SGP maintain the 3% deficit and 60% debt targets • However in respect of the deficit, account may be taken of: • (a) the effects of economic cycles • (b) underlying debt ratios • (c) deficit-finance of productivity-enhancing capital projects • However to minimise the ability to “fudge”, governments have to submit detailed stability and convergence programmes which outline fiscal policy over several years, and these proposals are assessed by the Commission • Clearly (b) and (c) would have suited Ireland up to 2007/8 • Recent events have blown away the short-term realisation of the targets, but Ireland has submitted a programme to get back to 3% by 2014.