Download

1 / 24

310 likes | 1.38k Vues

Earned Value and the Control Account Manager (CAM). George Stubbs, CBT Workshop. About George Stubbs the Presenter. Over 45 years Program Management Experience. 5 Years United States Air Force. 6 Years Raytheon. 8 Years Boeing. 7 Years Martin Marietta. 9 Years Independent Consultant.

E N D

Earned Value and the Control Account Manager (CAM) George Stubbs, CBT Workshop

About George Stubbs the Presenter • Over 45 years Program Management Experience. • 5 Years United States Air Force. • 6 Years Raytheon. • 8 Years Boeing. • 7 Years Martin Marietta. • 9 Years Independent Consultant. • 12 Years Senior Partner The CBT Workshop. • The CBT Workshop • A leading supplier for affordable skilled Earned Value Management System (EVMS) resources specializing in EVMS services, training, and tools support. The CBT Workshop www.cbtworkshop.com

Earned Value and the Control Account Manager • Why Be a CAM? • What is a Control Account Manager (CAM)? • The Control Account (CA). • What are a CAMs Responsibilities? • CAMs Activities and the Control Account. • The CAM and Control Account Performance. • CAM’s Monthly Requirements. • CAM Software Tools. • The CAM Notebook. • CAM Training. • What Makes a CAM Successful. • How to Undermine the CAM

Why Be a CAM? • First step into Management. • Opportunity to learn all aspects of project management. • Responsible for technical, schedule and cost performance. • Part of a progression of increasing responsibility. • CAMs become Program/Business Managers. • Program/Business Managers become Executives.

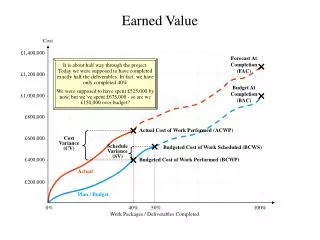

What is a Control Account Manager (CAM)? • The CAM plays a critical role in an Earned Value Management System. • Responsible for the planning, coordination and achievement of all work within a Control Account. • Provides a single authority for all scope, technical and cost issues for the Control Account. • Accountable to the Program Manager for Control Account Performance. • Authorized by and accountable to the PM for resources to complete cost, schedule and technical objectives. • Participates in Program Reviews, Integrated Baseline Reviews (IBRs), Validations and other project or management reviews. • Preparing for these reviews is a critical piece of the CAM’s role.

The Control Account (CA) • Virtually all aspects of the contractor's management control system come together at the CA level. • Is a management control point at which budgets (resource plans) and actual costs are accumulated and compared to earned value for management control purposes. • A control account is a natural management point for planning and control since it represents the work assigned to one responsible organizational element for a single program WBS element. • Performance is planned, measured, recorded, and controlled at the CA level.

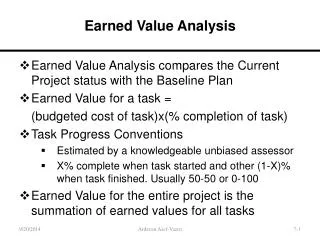

Establish the PMB Contract Price Total Allocated Budget (TAB) Fee / Profit / Margin Over Target Baseline (OTB) (if applicable) Contract Budget Base (CBB) Negotiated Contract Cost (NCC) Authorized Unpriced Work (AUW) EV Starts Here Performance Measurement Baseline (PMB) Management Reserve (MR) Distributed Budget (DB) Undistributed Budget (UB) The CAM Starts Here Control Accounts Summary Level Planning Packages Planning Packages Work Packages Discrete Work Apportioned Work Level of Effort Work The CBT Workshop www.cbtworkshop.com

What are a CAMs Responsibilities? • Must be given full responsibility for managing the cost, schedule and technical performance of the Control Account. • Supports all customer meetings and data requests pertaining to the Control Account. • Has authority to review and approve all work assignments, documents and commitments involving the Control Account. • Authorized by and accountable to the PM for resources to complete cost, schedule and technical objectives.

CAM Responsibilities (cont) • Review and approve all resources charged to the Control Account and assure their accuracy. • Prepare Control Account variance analyses. • Develop, implement and manage corrective actions, as appropriate. • Prepare Estimates to Completion for remaining Control Account work scope. • Provide forecast dates for accomplishing activities and milestones in the Control Account Schedule.

CAM Responsibilities (cont) • Prepare Estimates to Completion for remaining Control Account work scope. • Provide forecast dates for accomplishing activities and milestones in the Control Account Schedule. • Inform management of significant problems concerning Control Account performance. • Lead or participate in Make / Buy decisions.

CAMs Activities and the Control Account • Approve the Control Account Authorization documents. • Co-approve the Make / Buy Plan for material used to perform the Control Account scope of work. • Approve Control Account Budget Change Notices and Requests. • Authorize and coordinate work performed by functional departments on Work Directives within the Control Account. • Determine the work schedule and prioritize work within each Work Directives issued for the Control Account. • Approve hours charged to the Work Directives supporting the Control Account. • Identify potential technical, schedule and cost risks and enter them into the FCS Risk Management Process.

The CAM and Control Account Performance • Complete the Control Account scope of work within the schedule period and resources authorized. • Complete the Control Account scope of work. • Achieve the technical performance goals for the defined scope of work. • Achieve the technical quality. • Assure the reported Earned Value performance is based on qualified back-up data. • Mitigate all technical, schedule and cost risks associated with the Control Account.

CAM’s Monthly Requirements • Updating Schedule Status Convert Planning Packages to Work. • Revise Planning, Prepare CAPs, BCRs and WADs. • Review & Approve BCRs & WADs. • Enter CAP Planning Changes. • Forecast Milestone Status. • Mid-Month Schedule Forecast Update.

CAM’s Monthly Requirements • Update Schedule Status. • Complete Schedule. • Review & Correct Weekly Charges. • Review/Submit Changes to CAM Reports. • Review Preliminary Variance Analysis/PVA. • Prepare Variance Analysis Reports. • Review/Update/Approve PVA. • Review & Approve VARs.

CAM Software Tools • Earned Value • Deltek Cobra. • Oracle Primavera Cost Manager. • Deltek MPM. • Artemis Costview. • SAFRAN. • DekkerTrakker. • EcoSys. • Scheduling. • Microsoft Project. • Microsoft Project Server. • Oracle Primavera Project Manager. • Deltek OpenPlan. • Artemis Projectview. • Analysis and Review • forProject. • Deltek Risk Plus. • Deltek Active Risk Manager. • Deltek PM Compass. • Steel Ray. • Acumen. • Deltek wInsight. • IMS StopLight.

The CAM Notebook • The Control Account Manager (CAM) notebook is the key document for assisting the CAM in the integration and management of the control account. • The CAM notebook enables “single thread” analysis of the technical scope, integrated master schedule (IMS), resource loading profile, earned value (EV) performance data, and subcontractor costs. • An accurate, current, and complete CAM Notebook is critical to the successful management of the contracted work. • The review of the CAM Notebook and identification of the resulting risks are key parts of the IBR process to verify and validate the technical, cost and schedule baselines

Why is CAM Notebook Important? • Gives a clear picture of whether the control account’s technical scope, schedule , risk and resources are integrated, play together and make sense. • When understood by the government action officer (AO) and the CAM, brings both parties to a clear mutual understanding of all aspects of the task. • Ensures a foundation of information for continuity if the CAM or AO is reassigned or not available for some reason. • Documents what is going on and documents that all aspects of the task are being considered and harmonized and managed.

What is in a CAM Notebook? • Organization Documentation. • Integrated Master Plan. • Statement of Work (SOW). • Work Breakdown Structure (WBS) and WBS Dictionary. • Work Authorization Document. • Control Account Plan. • Basis of Estimate and other cost baseline supporting information. • Integrated Master Schedule. • Latest Earned Value Performance Report. • Subcontractor and Material Documentation. • Risk and Opportunity Management Documents. • Others as needed.

Types of CAM Notebooks • Hard Copy. • Difficult to keep current. • Bulky. • Requires continual maintenance to keep current. • Manpower requirement are high. • S0ft Copy (virtual CAM notebook). • One time set up. • Data is maintained through the companies internet. • CAM data resides on the CAM desktop. • Currency is maintained by a single responsible individual for each item. • All CAM related data is at the CAM’s fingertips.

CAM Training • Detailed s/w training for any software applications the CAM is going to be a hands on user. • Introductory training for any software applications that is not hands on. • EVMS basic through advanced. • Training in all reporting and analysis requirements that affect the CAM. • Integrated Baseline Review. • Mock CAM interview. • Validation Review (if required).

What Makes a CAM Successful • When CAMs are rewarded for their additional work. • Being a CAM is a “Stepping Stone” to becoming a Program Manager. • When Management supports them. • When the Program rely on them to manage their area of responsibility.

How to Undermine the CAM When Management pays lip service to earned value. When the Program fights earned value. When Management focuses on metrics not performance. When program levels do not understand how EV works and what it does. When Performance or Actuals are tailored to fit desired metrics. When CAMs are not rewarded for their additional effort. When Management makes EVMS related decisions without feed back from the CAMs.

Contact Information • www.cbtworkshop.com • gstubbs@cbtworkshop.com • 1-303-877-7201 Mobile • 1-888-644-5613 The CBT Workshop www.cbtworkshop.com

Q&A The CBT Workshop www.cbtworkshop.com