Download

1 / 51

510 likes | 524 Vues

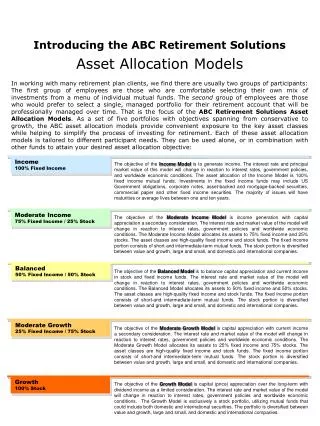

Asset Allocation in Retirement Portfolios. American Association of Individual Investors Washington, D.C. May 19, 2007 Craig L. Israelsen, Ph.D. Brigham Young University. Overview. Historical performance of major assets, the value of diversification, and the “Small Cap Premium”

E N D

Asset Allocation in Retirement Portfolios American Association of Individual Investors Washington, D.C. May 19, 2007 Craig L. Israelsen, Ph.D. Brigham Young University

Overview • Historical performance of major assets, the value of diversification, and the “Small Cap Premium” • Target Date Funds • The “Value Premium” • Alternative assets in a portfolio (commodities, real estate) • A tale of two portfolios (if we have time)

Analysis of Accumulation Portfolios • 25-year old participant • $45,000 starting annual income • Annual savings rate of 6% of income • Income increases 4% annually • 40-year investment period (age 25-64) • This analysis examines 8 40-year periods (from 1960-2006)

Various Accumulation Portfolios • Portfolio #1: 100% Large Cap US Equity • Portfolio #2: 60% Equity/40% Fixed Income • (40% Lrg US, 10% Sml US, 10% Non-US, 30% Bonds, 10% Cash) • Portfolio #3: Target Date Fund Glidepath from age 25 to 65 • (portfolio moves from high equity to high fixed income using all five asset classes) • Portfolio #4: 100% Bonds

Typical Target Date Fund Methodology 40% Equity 25% Equity

The ending date of the “Accumulation” period is critical (i.e. 2002)

Will an investor endure the setbacks in “equity heavy” portfolios?

Analysis of Portfolio Drawdown during Retirement • $500,000 Portfolio at age 65 • 5% Annual Withdrawal Rate ($25,000) • 3% Inflation Rate of Annual Withdrawals • 20-year analysis period (age 65-84) • This analysis examines 28 20-year periods (from 1960-2006)

Typical Target Date Fund Methodology 40% Equity 25% Equity

Drawdown Retirement Portfolios at age 65 Target Date Fund (“Glidepath” after age 65) (Average Equity Allocation of 35%/Average Fixed Income Allocation of 65%) 40% Equity/60% Fixed Income (20% Lrg US, 10% Sml US, 10% Non-US, 50% Bonds, 10% Stable Value) 25% Equity/75% Fixed Income (15% Lrg US, 5% Sml US, 5% Non-US, 50% Bonds, 25% Stable Value) 100% Fixed Income (100% Bonds)

Maximum Drawdown RiskRetirement Portfolio in Withdraw Mode • The timing of negative returns is the key issue. • If the negative returns occur early, the outcome can be disastrous. • If the negative returns occur later, chances of recovery are much higher.

Early years with negative returns cause the decline in a withdrawal portfolio account balance

The sensitivity of WHEN returns occur shows up in the drawdown phase

Target-Date Funds (Distinct Funds only) 180 160 140 120 100 80 60 40 20 0 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Target-Date Funds: Inception Year Target-Date Funds: Cumulative Total

The “Non-Target Date Funds” is a comparison group consisting of 72 funds which have the Dow Jones Moderate Portfolio as their “best-fit” index. Among target date funds, the most common best-fit index was the Dow Jones Moderate Portfolio.

Observations… • Compared to the Dow Jones Target Date Indexes, the typical target date fund is underweighted in mid cap and small cap stocks. • Therefore, it’s not surprising that the average target fund has underperformed the DJ Target Indexes in recent years.

Large Cap US Equity (1980-2006) Growth = Average of Dow Jones Large Growth Index and DJ Wilshire Large Growth IndexValue = Average of Dow Jones Large Value Index and DJ Wilshire Large Value Index

Mid Cap US Equity (1980-2006) Growth = Average of Dow Jones Mid Growth Index and DJ Wilshire Mid Growth IndexValue = Average of Dow Jones MidValue Index and DJ Wilshire Mid Value Index

Small Cap US Equity (1980-2006) Growth = Average of Dow Jones Small Growth Index and DJ Wilshire Small Growth IndexValue = Average of Dow Jones Small Value Index and DJ Wilshire Small Value Index

Observation… The typical target date fund is underweighted in value stocks, at least based on the performance of value-oriented stocks over the past 27 years.

Irony • Based on the typical composition of existing target date funds, “alternative” asset classes would include increased exposure to… mid and small cap stocks AND stocks with a value tilt… Or at least increased exposure.

Two classic “alternative” assets in a retirement (i.e. withdrawal) portfolio Commodities & Real estate

In light of the needed returns to recover from a loss… Retirement portfolios that are sustaining systematic withdrawals have two main goals: 1)Avoid large losses and • Produce a sufficiently high return to maximize the likelihood of not outliving the portfolio.

The risk/return characteristics of major asset classes from 1970-2006 (adding commodities and REITs) ASSUMING BUY-and-HOLD

Multi-Asset 60 Eq/40 Bond = 20% Lrg US, 10% Sml, 10% Non-US, 10% Comm, 10% REIT, 30% Bond, 10% CashAggressive Equity = 20% Lrg US, 20% Sml, 20% Non-US, 20% Commodities, 20% REIT

A Tale of Two Portfolios Vanguard & Homestead Alternative “pathways” to investing

The Homestead Portfolio$1 minimum requirement to open each fund (automatic monthly investment)

Vanguard: $12,000 up front OR Homestead: $4 per monthVanguard Portfolio: 80 bps lower return, 470 bps higher volatility