Download

1 / 9

90 likes | 333 Vues

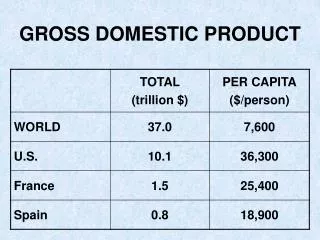

Gross Domestic Product By: Mrs. Erin Cervi. Gross Domestic Product. G = Gross- TOTAL D = Domestic- Made in a country P = Product- Production of a final good/service during a specific period of time . (GDP) measures our nations (and others around the world) total economic performance

E N D

Gross Domestic Product By: Mrs. Erin Cervi

Gross Domestic Product G= Gross- TOTAL D= Domestic- Made in a country P= Product- Production of a final good/service during a specific period of time. (GDP) measures our nations (and others around the world) total economic performance It is an economic indicator! 1991 U.S. gov’t switched from GNP to GDP GNP: included production of all U.S. resident’s no matter where they were located WE WANTED TO KNOW WHAT WAS GOING ON IN OUR COUNTRY! Bureau of Economic Analysis (BEA): Calculate the GDP in the U.S.

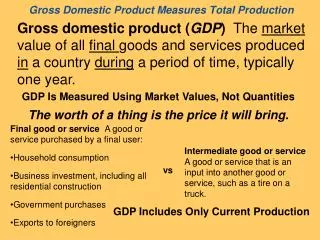

Counted Toward GDP NOT Counted Toward GDP • Intermediate goods (NO DOUBLE COUNTING) • Old goods/resale goods (already counted before) • U.S. companies abroad • Financial assets (stocks, bonds, CDs) • Non-market activity • unpaid labor/do-it-yourself projects, finding own home, buying own stocks, volunteer work • under the table transactions b/c no record of transaction (babysitting) • Public transfer payments (SS, Medicaid, unemployment) • Private transfer payments (gift of money) • only final goods and services (C, I,G, (X-M)) • New (produced that year) • Capital resources count if they are NEW • Domestically produced • Foreign companies w/in U.S. borders • Commissions (broker fees, real estate agent fees) • Inventories (produced, just not sold)

Gross Domestic Product (GDP) • GDP is measured by totaling money spent on four categories. • GDP= C+I+G+ (X-M)

Productivity and Wages–the Big Disconnect Consumption • Definition: The spending by households on goods and services. • A new car, food, clothes, college tuition, sporting event, health insurance. • Makes up 2/3rds of GDP At the beginning of the 1980’s, just over 60% of the U.S. Gross Domestic Product was consumer spending. Today, consumer spending is close to 70% of GDP. http://www.irle.berkeley.edu/events/spring08/feller/

Investment • Investment sometimes refers to the purchase of financial products, such stocks, bonds, or even gold, with the hope of making money in the future. • Regarding GDP, investment is defined as: purchases that contribute to the overall performance of an economy. • There are THREE things that count as investments • Spending by businesses on capital resources/machinery, factories, equipment, tools, computers, technology, new buildings. • Individuals buying a new house • INVENTORIES: A company's merchandise, raw materials, and finished and unfinished products which have not yet been sold.

Government Spending • Definition: Spending by all levels of government on goods and services • Direct payment for goods/services • Military, roads, healthcare

Net Exports • Definition: Spending by people outside the United States on US produced goods (exports, or X) • Minus spending by people in the United States on foreign goods and service (imports, or M) • (X-M) = Net Exports

How is GDP an economic indicator? • When the GDP is rising, a national economy is growing. • If the U.S’s GDP increases 3-5% each year =optimal b/c we are growing at a healthy, sustainable rate (a rate that can be kept up). • When GDP increases 2% and below it is considered to have a sluggish/declining economy. • Even better indicator: real GDP per capita=real GDP/population