Download

1 / 21

210 likes | 315 Vues

Consultancy & training for women in horticulture, dairy, coffee, and potato farming financial services. Research methodology, importance of agriculture, financial issues, and recommended high-impact products discussed. Challenges, opportunities, and conclusions shared.

E N D

Consultants and Trainers Helping Women to Grow! Financial services in agriculture value chains Domestic Horticulture Extensive Livestock Potato Dairy Coffee Tuesday 25th May 2010

RESEARCH METHODOLOGY • Desk study of relevant materials and past studies, literature review • Depth interviews with stakeholders and chain actors • Survey (potato farmers) • Engagement of stakeholders at various sectoral forums e.g. exhibitions • Case study

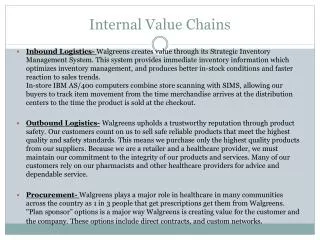

Potato sub-sector Market Retailer NM=24.52% Stall Owner NM=22.52% Farmer NM=75.2% Wholesaler/Transporter NM=18.09% Supermarket GM=259.33% Processor - Fries NM= 100% • Background

Potato sub-sector • AVAILABLE PRODUCTS • Large players can access funds from banks and MFIs • Generally no specialised products for sub-sector except by AFC (Nanyuki and Molo areas only) • Group loans through ROSCAs helpful to farmers • Microcredit by MFIs especially for traders • Government funds e.g. Njaa Marufuku, ASCU • RECOMMENDED HIGH-IMPACT PRODUCTS • Value Creation – Inputs and irrigation • Value Preservation – Cold storage and efficient transport • Value Addition – Processing and marketing • FINANCIAL ISSUES

Potato sub-sector - CONCLUSION • MAJOR CHALLENGES TO SECTOR FINANCE • Low productivity – Inputs, clean seeds • Lack of cold storage for seed and ware potato • Climate risks – drought, floods, frost • Price instability/Market access • Excessive intermediaries - brokers • LINKAGES AND OPPORTUNITIES • Horizontal – Farmer cooperatives for linkage • Vertical –e.g. Deepa Industries e.g. Midlands • CONCLUSIONS • Mobilisation of farmers crucial to financial access • Cold storage and vertical linkages – long term • More development organisations needed

DAIRY SUB-SECTOR Chilling Processing Transport Production Distribution Retail • Background and Value Chain

DAIRY SUB-SECTOR-finance • AVAILABLE PRODUCTS • Many specialised products available • Processor guaranteed loans and advances on delivery e.g. Equity, Coop Bank • Input finance – inputs supplied on credit e.g. Githunguri Dairy • SACCOs loans – for capital and operations • Equity investments e.g. Aureos Capital, members • Micro-leasing e.g. Juhudi Kilimo – Purchase cow • Dairy loans by MFIs e.g. Sisdo • Wholesale loans e.g. MESPT – ABD for ASALs • Various projects e.g. EADD, KDSCP, MESPT, SDCP, IQAM • RECOMMENDED HIGH-IMPACT PRODUCTS • Value Creation – Purchase of superior breed • Value Preservation – Chilling plants/Cold transport • Value Addition – Processing long-life products

DAIRY SUB-SECTOR-conclusion • MAJOR CHALLENGES TO FINANCE • Low productivity – Inputs, clean seeds • Production seasonality – gluts, low prices • Unlinked farmers are locked out • Excessive informality in distribution (hawking) • Low investment in long-life processing capacity • Diminished market prospects – supply inconsistency • LINKAGES AND OPPORTUNITIES • Mobilise horizontal and vertically unlinked farmers • International and regional markets • CONCLUSIONS • Marketing is the key threat to finance for the sector • Producer prices below production costs • Inclusion of milk in strategic food reserves urgent • More dairy hubs necessary for increased access to finance • Replication of success models e.g. Githunguri DFCS/Fresha

Domestic horticulture Wholesale Processing Transport Production Distribution Retail • Background and Value Chain Market Value as of 2007

Domestic horticulture - finance • AVAILABLE PRODUCTS • Many specialised products available • Asset finance loans for greenhouses (Amiran kit) by Coop Bank, Equity, KWFT etc • Agriculture loans by many MFIs e.g. Sisdo, Pawdep • Wholesale loans e.g. MESPT-ABD for ASALs • Seasonal and modified loans e.g. pay as you harvest from AFC, Pawdep, KADET etc • Micro-leasing for assets such as drip irrigation e.g. Juhudi Kilimo • Business loans for horticulture traders e.g. AFC, Equity • RECOMMENDED HIGH-IMPACT PRODUCTS • Value Creation – Greenhouses and drip irrigation • Value Preservation – Cold chains for domestic • Value Addition – Juice extraction, drying, fruit concentrates etc

Domestic horticulture-conclusion • MAJOR CHALLENGES TO FINANCE • Climate risks – droughts, floods, extreme cold • Market risks – postharvest gluts too low prices • Wastage 30-40% post-harvest losses • Lack of diversification by farmers despite the many opportunities e.g. herbs, over 40 vegetables • Low value addition despite high potential • Poor market linkages – horizontal and vertical • High quality just for exports - • LINKAGE AND OPPORTUNITIES • Mobilise farmers for horizontal and vertical linkage • Importation of concentrates for juices??? • CONCLUSIONS • Over-reliance on rain-fed system need to be reduced • Mobilisation of farmers require further effort • Linkages will be key to accelerating finance • Greater integration into higher value chain activities • Cold chains are an urgent issue for sustainability

Coffee sub-sector Milling Marketing Pulping Production Roasting Retail/Export • Background and Value Chain

COFFEE SUB-SECTOR- finance • AVAILABLE PRODUCTS • Few specialised products available • Advances/Seasonal loans by Coffee Development Fund (CODF) <= 2 kg per coffee tree • Coffee Rehabilitation loan by CoDF < 1kg per tree • Cash-crop loans by AFC for 2-8 years • Advances on delivery by millers e.g. Nyambene Mills • SACCO loans e.g. Taifa SACCO • Supplier credit available to most farmers • Grant - Value Chain Based Matching Grant Fund • RECOMMENDED HIGH-IMPACT PRODUCTS • Value Creation – Warehouse receipting system, Input finance (guaranteed lending) • Value Preservation – Upgrade pulping technology • Value Addition – Coffee shop setup and operation

Coffee sub-sector-conclusion • MAJOR CHALLENGES TO FINANCE • Climate risks – droughts, floods, extreme cold • Poor attitude towards coffee farming and the industry • Deep mistrust among chain actors • Outdated pulping technology • Exposure to global economic risks. Export overreliance • Lack of traceability. No pay for quality • Poor corporate governance by cooperative • Too much government • LINKAGE S AND OPPORTUNITIES • Coffee act to be changed to allow farmers to control the product along the entire value chain • Coffee shops – more players are needed • CONCLUSIONS • Domestic market and diversification of international markets • Transparency regarding margins by chain actors

EXTENSIVE LIVESTOCK Slaughter Distribution Trade Production Butchery Retail/Export • Background and Value Chain

Extensive livestock - finance • AVAILABLE PRODUCTS • Few specialised products available • Livestock purchase loan for traders – Equity/CARE • Livestock business/project loan by Kenya Livestock Finance Trust • MFI loans for poultry farming (tied to farming cycle) • Supplier credit available to poultry farmers • Grant – By Government for restocking after drought • Livestock insurance by Equity and UAP Insurance • RECOMMENDED HIGH-IMPACT PRODUCTS • Value Creation – Loans for quality breeds • Value Preservation – Micro-leasing for freezers • Value Addition – Equipment to add value e.g. meat mincers and electronic scales by butcheries

Conclusion - FINANCE • Farmer mobilisation most crucial for financial access • Climate change adaptation key risk mitigation • Market driven development of financial services • Training of MFIs on agriculture finance critical • Grant should be used as last resort • Record-keeping by farmers too poor

Conclusion - general • Consider entire portfolio of value chain for a farmer • Ongoing regional integration to impact on value chains • Harmonisation of NGO activity in value chains. Cooperation vs competition • Collapse of government extension services hurting all sub-sectors