Download

1 / 12

140 likes | 212 Vues

Fractional Reserve Banking. When banks hold only a small portion of deposits to cover potential withdrawals and then loan the rest of the money out. Bank Balance Sheets.

E N D

Fractional Reserve Banking When banks hold only a small portion of deposits to cover potential withdrawals and then loan the rest of the money out.

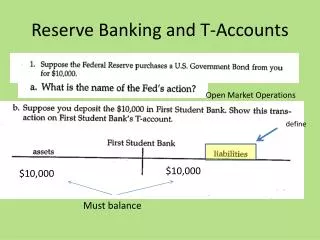

Bank Balance Sheets Bank balance sheets are an accounting of a bank’s liabilities and assets. On a bank balance sheet, assets always equal liabilities (they balance). On the left side of a bank balance sheet, you will find the bank’s assets. Assets are all of the things the bank owns that are of value. On the right side of the bank balance sheet, are the liabilities. They are essentially a bank’s debts.

Bank Balance Sheets - Assets Required Reserves are a percentage of checkable deposits (checking account deposits) set by the Federal Reserve’s reserve requirement. Excess Reserves is the amount of total reserves the bank can loan out. Required reserves plus excess reserves equals total reserves (sometimes just called reserves). Loans given to customers are on the assets side of the balance sheet because these promises to pay are worth the amount of the loan.

Bank Balance Sheets - Assets Securities are bonds held by the bank which are essentially loans to a business or the government. Physical Assets include the bank building, desks, chairs, computers, and even those pens with the chain attached. These are the physical objects (capital) the bank owns.

Bank Balance Sheets - Liabilities Checkable Deposits (Demand Deposits) are checking account deposits. The percentage of money banks must hold (set by the Fed’s reserve requirement) that comprise the required reserves. Other Deposits (sometimes listed as “savings deposits”) are deposits from customers that go in to non-checking accounts. There are no required reserves on these “other deposits.”

Bank Balance Sheets - Liabilities Other Liabilities include loans and other debts owed by the bank. Don’t confuse these with loans found on the assets side of the balance sheet which are loans owed to the bank. Owner Equity is money (profit) owed to the owners (or shareholders) of the bank.

If Bob deposits $1,000 cash into his checking account: 1. What is the RR? 2. Will the M1 money supply initially ↑, ↓, or stay the same? 3. What is the value of Required Reserves after his deposit? 4. What is the value of Excess Reserves after his deposit? 5. How much more can the bank lend out after his deposit? 6. What is the maximum change in the money supply from his deposit? 10% Same $2,100 $3,900 $900 $9,000

The Fed buys back $1,000 worth of bonds from this bank: 1. What is the value of Required Reserves now? 2. What is the value of Excess Reserves now? 3. How much more can the bank initially lend out? 4. What is the maximum change in the money supply? $2,000 $4,000 $1,000 $10,000