Download

1 / 44

440 likes | 713 Vues

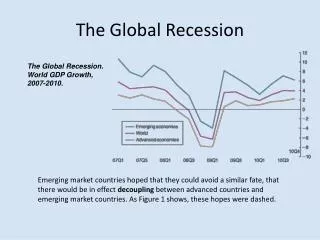

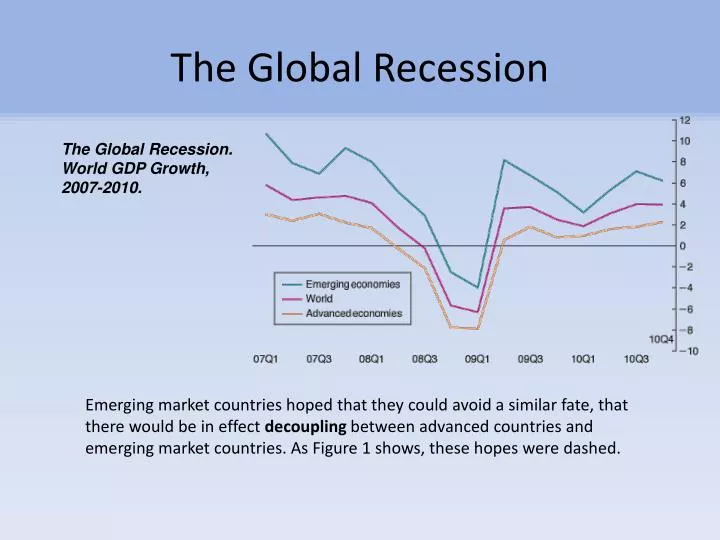

The Global Recession. The Global Recession. World GDP Growth, 2007-2010. . Emerging market countries hoped that they could avoid a similar fate, that there would be in effect decoupling between advanced countries and emerging market countries. As Figure 1 shows, these hopes were dashed.

E N D

The Global Recession The Global Recession. World GDP Growth, 2007-2010. Emerging market countries hoped that they could avoid a similar fate, that there would be in effect decoupling between advanced countries and emerging market countries. As Figure 1 shows, these hopes were dashed.

The Global Recession Stock Prices and the Recession, 2007-2009. From early 2007 to the end of 2008, stock prices lost more than half of their value. While they have recovered, they are still far below their peak.

The Trigger. U.S. House Price declines U.S. housing prices, 2000-2009. Housing prices increased sharply from 2000 to 2006, only to decline, equally sharply, from 2006 on.

The Trigger. U.S. House Price declines • These developments were much less benign than most economists thought. • First, housing prices could go down. • Second, in many cases, the mortgages were in fact much riskier than either the lender pretended, or the borrower understood. • The estimated output cost of the crisis is around $30 trillion, roughly 1/2 of annual world GDP, and 100 times the initial mortgage losses! • While the trigger was the U.S. housing price decline, its effects were enormously amplified.

The Subprime Triggered Crisis: A Perfect Storm Confluence of causes • Past bailouts Greenspan Put Bulletproof system!?!?? • Financial innovations: Finance as end in itself • Income lagging spending: Household debt…National debt • Easy credit...Fed Funds Rate kept low • Market fundamentalism • Weak global aggregate demand The Players • Mortgage brokers/Banks—Securitizers/GSEs/Rating Agencies Trigger and collapse Bailouts: Wall Street, not Main Street Stimulus Slump: Koo—Balance Sheet Recession Kindleberger—Minsky—Fisher Akerlof-Shiller: Animal Spirits Eggertsson-Krugman: Debt, Deleveraging and the Liquidity Trap Krugman: End This Depression Now!

The Subprime Triggered Crisis: A Perfect Storm Finding Fault • Past bailouts Too big/Too interconnected to Fail • Black Monday (October 19, 1987) • Asian CrisisContagionLongTermCapitalManagement (1997-8) • dot.com bubble … it takes a bubble • Financial innovations • Overnight funding • Off-balance sheet vehicles – no capital requirements • Default insurance • Collateralized Debt Obligation (CDOs) • Chemistry: JunkAAA Financial Engineering

The Subprime Triggered Crisis: A Perfect Storm Finding fault • Easy Credit • Global saving glut • Fed policy: fear of deflationcheap raw material for banks • Market fundamentalism • Greenspan “put”—we’ll clean up the mess • Lax regulation • Weak global aggregate demand—saving glut • Accumulation of reserves—memories of ‘97

A “Global Saving Glut” The best of times Capital Inflows Easy Money Policy Escalating House Prices Eager Home Buyers Ambitious Mortgage Brokers Developer Clout Innovative Banks Securitization MBSs Rating Agencies Gov’t Sponsored Enterprises Bank Regulators

The best of times Capital Inflows Escalating House Prices Easy Money Policy Eager Home Buyers Ambitious Mortgage Brokers Developer Clout Innovative Banks Rating Agencies Securitization MBSs Gov’t Sponsored Enterprises Bank Regulators

Amplification Mechanisms. Leverage, Complexity, and Liquidity • When housing prices declined, and some mortgages went bad • High leverage implied a sharp decline in the capital of banks. • This forced them to sell some of their assets that were often hard to value. • They had to sell them at very low prices—often referred to as re sale prices. • The complexity of the securities (MBSs, CDOs) and of the true balance sheets of banks (banks, and their SIVs) made it very difficult to assess the solvency of banks, and their risk of bankruptcy. • Interbank lending froze. • On September 15, 2008, Lehman Brothers, a major bank with more than $600 billion in assets, declared bankruptcy. • Leading financial participants concluded that many, if not most, other banks and financial institutions were indeed at risk. • These guys knew the shape they themselves were in...if they couldn’t trust themselves, how could they trust counterparties??? • INTERBANK LENDING FROZE

Amplification Mechanisms. Leverage, Complexity, and Liquidity Amplification mechanisms The Ted Spread, 2007-2009. The rate spread, which reflects the risk banks perceived in lending to each other, went sharply up in September 2008. Banks became very reluctant to lend to each other. The TED Spread: The difference between the riskless rate (measured by the rate of 3-month government bonds) and the rate at which banks are willing to lend to each other (known as the Libor rate...which we now know was understated!)

U.S. Consumer and Business Confidence, 2007-2009. From a Financial to a Macroeconomic Crisis The Decrease in U.S. GDP The financial crisis led to a sharp drop in confidence, which bottomed in early 2009.

Responses Lender of Last Resort / Spender of Last Resort • Tax Rebate $124 bil. • Fed Fund Rate Cuts • Fannie/Freddie $200 bil. • Bear-Stearns $29 bil. • AIG $174 bil. Fed “Facilities” • Primary Dealer Credit Facility (PDCF) $58 bil. • Treasury Security Loan Facility (TSLF) $133 bil. • Term Auction Facility (TAF) $416 bil. • Asset- Backed Commercial Paper Funding Facility (CPFF) $1,777 bil. • Money Market Investor Funding Facility (MMIFF) $540 bil. • More Fed Fund Rate Cuts … Hold At ~0% • Fed Purchases of Long-Term Securities: GSEs & MBSs $600 bil. • Term Asset-Backed Securities Loan Facility (TALF) $200 bil. • Emergency Economic Stabilization Act/TARP $700 bil. Government Loans Government Equity • Stimulus Package $787 bil. aka The American Recovery and Reinvestment Act (ARRA) • TARP II • Stress Tests

Feeding a Crisis: Alphabet Soup • Finance and its discontents SIV, Repo, MBS, CDO, CDO2, CDS, S&P, AAA, ARM, TED–LIBOR FOMC, FF, FDIC, GSE, AIG, G-7 • Bailout “facilities” PDCF, TSLF, TAF, CPFF, MMIFF, TALF • Legislation TARP, ARRA • Ben Bernanke: The Fed and the Crisis http://www.federalreserve.gov/newsevents/lectures/federal-reserve-response-to-the-financial-crisis.htm

The Subprime Triggered Crisis: The Players Charles Kindleberger, Manias, Panics and Crashes A Minsky Story in Five Acts: In general…in particular • Displacement—A breakthrough • Financial innovation: securitization—sell off risk • Credit Expansion & BOOM • Low interest rates—defend against deflation • Shadow banking/SIVs/MBSs/CDOs/CDSs • Speculative Mania—self-fulfilling Euphoria • Teaser loans/ARMs/Home equity loans/Flipp’n’ to the bank • Distress—a Minsky/Lehman/Wile E. Coyote moment

The Subprime Triggered Crisis: The Players Charles Kindleberger, Manias, Panics and Crashes A Minsky Story in Five Acts: In general; in particular • Displacement—A breakthrough • Financial innovation: securitization—sell off risk • Credit Expansion & BOOM • Low interest rates—defend against deflation • Shadow banking/SIVs/MBSs/CDOs/CDSs • Speculative Mania—self-fulfilling Euphoria • Teaser loans/ARMs/Home equity loans/Flipp’n’ to the bank • Distress—a Minsky/Wile E. Coyote moment • House prices plateau—Disappointed expectations • Panic & Crash—rush to liquidity…but there’s no liquidity • Firesale • Foreclosures • Contagion • Debt Deflation • Bailout Helicopter Ben

Minsky’s World Quasi – rents: cash flows available to pay debts PI – [supply] price of investment goods PK – [demand] price of kapital goods Borrower’s risk Lenders risk Hedge finance: E(cash flows) > Payment commitment Speculative finance: E(cash flows)<Commitment … but > Interest commitment Roll over debt Ponzi finance: E(cash flows)<Interest commitment … Expect to increase debt Financial fragility: mix of Hedge – Spec – Ponzi Good times Confidence Risk-taking Fragility

The Minsky FootprintRealized expectations Increased profits & Reduced risk BOOMDisappointed expectations Reduced profits & Confidence BustRush to liquidity Debt deflation Pk Borrower’s Risk Internal funds Marginal lender’s risk Lender’s Risk PI Investment “If the demand price of a capital asset … is not less than its replacement costs, new investment will take place.”

Akerlof and Shiller, Animal Spirits • Confidence – Keynes-Minsky • Hopes, Exuberance, Fears • Waves of optimism and pessimism • Corruption - Bad Faith Loss of Trust • S&Ls – Enron – Sub-prime • Fairness • Punish cheaters, even at own expense • Relative position • Money illusion • “Illusion” is real in view of nominal contracts/accounts • Stories • New eras – Irrational exuberance Downward wage rigidity

Disinflation, Deflation, and the Liquidity Trap • According to your textbook, the built-in mechanism that can lift economies out of recessions is this: • Output below the natural level of output leads to lower inflation. • Lower inflation leads in turn to higher real money growth. • Higher real money growth leads to an increase in output over time. • (M/P) up i down I up Y up…until full employment restored • This mechanism, however, is not foolproof.

A Long Slump • Spending decisions depend on real interest rate • Demand for real balances depends on nominal rate The Textbook Effects of Lower Inflation on Output When inflation decreases in response to low output, there are two effects: (1) The real money stock increases, leading the LM curve to shift down, and (2) expected inflation decreases, leading the IS curve to shift to the left. The result may be a further decrease in output.

A Long Slump The Liquidity Trap Money Demand, Money Supply, and the Liquidity Trap When the nominal interest rate is equal to zero, and once people have enough money for transaction purposes, they become indifferent between holding money and holding bonds. The demand for money becomes horizontal. This implies that, when the nominal interest rate is equal to zero, further increases in the money supply have no effect on the nominal interest rate.

A Long Slump: Liquidity Trap and Deflation The Liquidity Trap and Deflation In the presence of a liquidity trap, there is a limit to how much monetary policy can increase output. Monetary policy may not be able to increase output back to its natural level. Suppose the economy is in a liquidity trap, and there is deflation. Output below the natural level of output leads to more deflation over time, which leads to a further increase in the real interest rate, and leads to a further shift of the IS curve to the left. This shift leads to a further decrease in output, which leads to more deflation, and so on. In words: The economy caught in a vicious cycle: Low output leads to more deflation. More deflation leads to a higher real interest rate and even lower output, and there is nothing monetary policy can do about it.

Negatively sloped AD: • Inflation down • Burden of debt on debtors up They spend less • Wealth of creditors up but they’re not spenders

TopsyTurvy Economics:Debt Deflation at Zero Lower Bound • Monetary stimulus doesn’t matter when interest rate on bonds is zero: • Currency Up but Deposits Down M up a little • H up $GDP unaffected or down • Reserves Up Bank Credit Down • It’s like “pushing on a string” • Paradox of thrift: • Deleveraging: S up Y down P down (M/P) up ... But i can’t fall so no recovery • Paradox of deleveraging: Fire sale of assets only lowers their prices Deflation • The more debtors pay the more they owe. • Perverse Aggregate Demand (upward sloping: falling price reduces spending) • Debtors can’t spend and creditors won’t spend (unless real interest rate is negative) • Paradox of toil: Increased supply drives down price and reduces output and employment • Paradox of flexibility: The more wages and prices fall in slump, the worse things get • Prescriptions: • Fiscal stimulus • Increased gov’t debt inflationary expectations • Central bank commitment to irresponsible stance inflationary expectations • Debt forgiveness: principal reductions

Has potential real GDP shifted downward? • Prolonged unemployment loss of skills • Then we’re not in a slump...get used to it • ...But we got back on track after • the Great Depression • It took WWII High employment/learning • scientific breakthroughs • ...is there a lesson here?

The Great Depression U.S. Unemployment, Output Growth, Prices, and Money, 1929 to 1942 Year UnemploymentRate (%) Output Growth Rate (%) Price Level Nominal Money Stock 1929 3.2 9.8 100.0 26.6 1930 8.7 7.6 97.4 25.7 1931 15.9 14.7 88.8 24.1 1932 23.6 1.8 79.7 21.1 1933 24.9 9.1 75.6 19.9 1934 21.7 9.9 78.1 21.9 1935 20.1 13.9 80.1 25.9 1936 16.9 5.3 80.9 29.5 1937 14.3 5.0 83.8 30.9 1938 19.0 8.6 82.2 30.5 1939 17.2 8.5 81.0 34.1 1940 14.6 16.1 81.8 39.6 1941 9.9 12.9 85.9 46.5 1942 4.7 13.2 95.1 55.3

Stimulus and Retrenchment: Recession in Depression Regime Change

The Great Depression The Contraction in Nominal Money • The puzzle is why deflation ended in 1933. • One proximate cause may be the set of measures taken by the Roosevelt administration such as establishing the National Industrial Recovery Act (NIRA) of 1933. • Another factor may be that while unemployment was still high, output growth was high as well. • Another factor may be the perception of a “regime change” associated with the election of Roosevelt.

The Japanese Slump • The robust growth that Japan had experienced since the end of World War II came to an end in the early 1990s. • Since 1992, the economy has suffered from a long period of low growth—what is called the Japanese slump. • Low growth has led to a steady increase in unemployment, and a steady decrease in the inflation rate over time.

The Japanese Slump: Output Growth since 1990 (percent) The Japanese Slump From 1992 to 2002, average GDP growth in Japan was less than 1%.

Unemployment and Inflation in Japan since 1990 (percent) The Japanese Slump Low growth in output has led to an increase in unemployment. Inflation has turned into deflation.

The Japanese Slump • The numbers above raise an obvious set of questions: • What triggered Japan’s slump? • Why did it last so long? • Were monetary and fiscal policies misused, or did they fail? • What are the factors behind the modest recovery?

The Rise and Fall of the Nikkei Stock Prices and Dividends in Japan since 1980 The increase in stock prices in the 1980s and the subsequent decrease were not associated with a parallel movement in dividends. • The fact that dividends remained flat while stock prices increased strongly suggests that a large bubble existed in the Nikkei. • The rapid fall in stock prices had a major impact on spending—consumption was less affected, but investment collapsed.

The Japanese Slump The Failure of Monetary and Fiscal Policy Fiscal policy was used as well. Taxes decreased at the start of the slump, and there was a steady increase in government spending throughout the decade. Fiscal policy helped, but it was not enough to increase spending and output.

The Failure of Monetary and Fiscal Policy Government Spending and Revenues (as a percentage of GDP) in Japan since 1990 Government spending increased and government revenues decreased steadily throughout the 1990s, leading to steadily larger deficits. • Output growth has been higher since 2003, and most economists cautiously predict that the recovery will continue. This raises the last set of questions. What are the factors behind the current recovery? • There appear to be two main factors. A Regime Change in Monetary Policy The Cleanup of the Banking System