Download

1 / 2

20 likes | 47 Vues

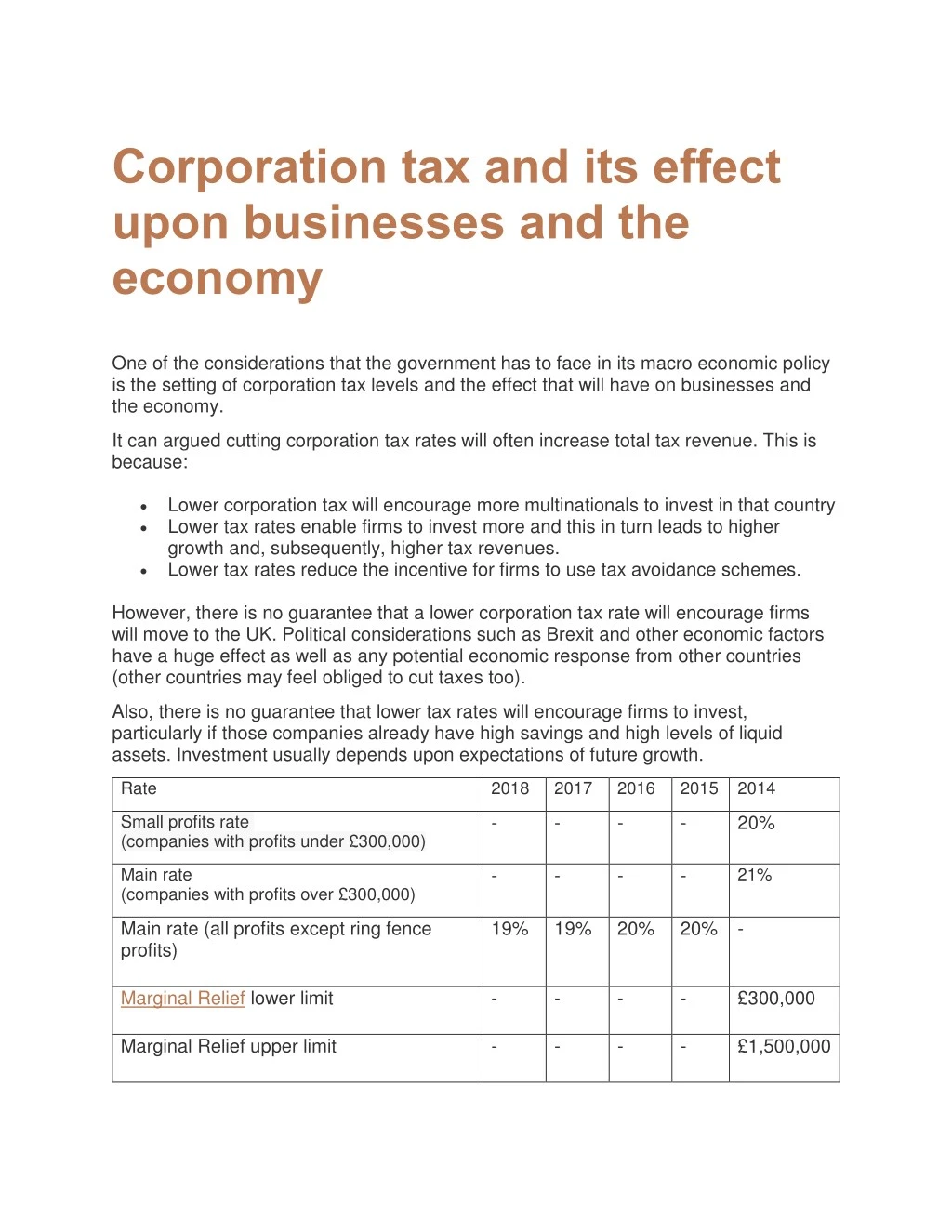

One of the considerations that the government has to face in its macro economic policy is the setting of corporation tax levels and the effect that will have on businesses and the economy.

E N D

Corporation tax and its effect upon businesses and the economy One of the considerations that the government has to face in its macro economic policy is the setting of corporation tax levels and the effect that will have on businesses and the economy. It can argued cutting corporation tax rates will often increase total tax revenue. This is because: •Lower corporation tax will encourage more multinationals to invest in that country •Lower tax rates enable firms to invest more and this in turn leads to higher growth and, subsequently, higher tax revenues. •Lower tax rates reduce the incentive for firms to use tax avoidance schemes. However, there is no guarantee that a lower corporation tax rate will encourage firms will move to the UK. Political considerations such as Brexit and other economic factors have a huge effect as well as any potential economic response from other countries (other countries may feel obliged to cut taxes too). Also, there is no guarantee that lower tax rates will encourage firms to invest, particularly if those companies already have high savings and high levels of liquid assets. Investment usually depends upon expectations of future growth. Rate 2018 2017 2016 20152014 Small profits rate (companies with profits under £300,000) - - - - 20% 21% Main rate (companies with profits over £300,000) - - - - Main rate (all profits except ring fence profits) 19% 19% 20% 20% - Marginal Relief lower limit - - - - £300,000 Marginal Relief upper limit - - - - £1,500,000

Standard fraction - - - - 1/400 Special rate for unit trusts and open-ended investment companies 20% 20% 20% 20% 20% In terms of how the local business can respond to corporation tax then, clearly, it is a good idea to have a discussion with your accountant to explore the best approach to compliance with HMRC requirements and coming up with a solution that is as efficient as possible for your business. Charterhouse specialises in tax management and so we have strong skills in this area. For reference, here are the latest rates that were introduced on 1st April 2018. There are different rates for ring fence companies and you can find further details at the HMRC site here: https://www.gov.uk/government/publications/rates-and-allowances- corporation-tax/rates-and-allowances-corporation-tax If you have any questions about corporation tax or, indeed, any other taxation matters, then please do get in touch and we will be able to give you chapter and verse on the current requirements. Charterhouse works in partnership with its clients to provide cutting edge tax expertise along with complete accountancy services. Located in Harrow and Beaconsfield and serving clients in Watford, Wembley, High Wycombe and throughout the UK, Charterhouse writes blog articles to help provide insights and expert advice.