Download

1 / 24

240 likes | 499 Vues

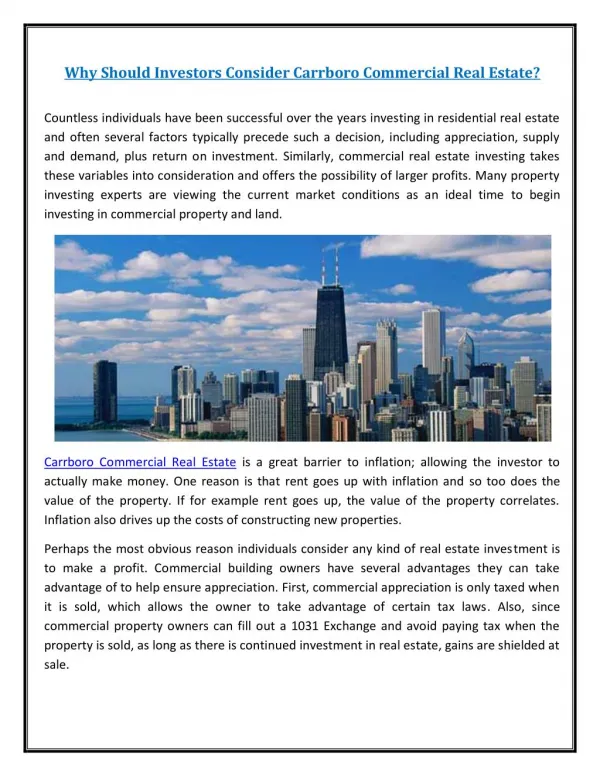

HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKET NOVEMBER 2009 Veterans Day. Presented by: Andrews & Galvin Appraisal Services, LLC 16 Spring Lane, Farmington, CT john@agvalues.com 860-677-5522. REAL ESTATE MARKET PRESENTATION OVEVIEW Hartford County – Fall 2009.

E N D

HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKETNOVEMBER 2009Veterans Day Presented by: Andrews & Galvin Appraisal Services, LLC 16 Spring Lane, Farmington, CT john@agvalues.com 860-677-5522

REAL ESTATE MARKET PRESENTATION OVEVIEWHartford County – Fall 2009 • What Just Happened – Where are we Now? • Market Real Estate Segments • Review of Trends

Last Years Theme - What Segment of the Coaster Do You Operate In?

IM STICKING WITH THE COASTERSReality Is All Hartford Market Segments Are Heading in the Same Direction Fall 2009

Last Year Question - Feeling the Trend?This Year – There is No QuestionWe are Feeling It!

Total Number of SalesTracked by Conn-compsNovember 1989 to 2009

Results of Phone Surveys • Last Year – Uncertainty over Financial Markets and Some Over President Elect • Changes in Financial Markets We Understand - Liquidity • Since Presidential Elect – External Changes Causing Uncertainty Most Do Not Understand – Automotive, Unemployment, Housing, Health Care, War … • Too Many Changes Too Fast • Consequently – Hartford Commercial Real Estate Market is Nearly On Hold – lack of liquidity - Resulting in Large Disconnect Between Market Participants

So What Are the Uncertainties? Stimulus Package-Residual Impact of Clunkers • Automobile Market Here in Hartford – More Vacant Space • Obsolete Space – Vacant Auto dealerships - • Less Used Car Inventory–low end? • Les Cars to Repair – Less Demand for Automotive Garages • Less Demand For Auto Parts – Increase in Vacant Retail Space • Starting to See Foreclosures in This market segment - 1099 • Defense – Middle East • UTC – Renewed Headquarters Lease in Gold Building – but closing some operations • Several Manufactures Pulling Back Work from Smaller Job Shops

Housing Stimulus • The $8,000 Credit – • Did it Just Shift Remaining Demand Up? • Did it Increase home furnishing, appliance, etc. spending ? • Did it Consume Remaining Supply • Will the $6,500 cause many to sell and then rent – retired focusing on future expenses? • New $8,000 credit to have same impact on housing prices as it did on automotive pricing – at least locally – Just Shift Prices Up? • Did Help New Residential Projects

Health Care Reform • Creates Uncertainty in the Hartford Real Estate Market • Will it Change Future Demand for Office Space by Insurance Users? • Employment Base – Location Quotient – Will it Change? • What About B and C Office Near Hospitals and Suburbs? • Retail Base – Will it Decline? • Municipalities–Tax Base Change? • Medical Space Demands Change? • Hospitals Repositioning

So – Market is Nearly Stagnant – definitely Slowed Down • Lets Look at some Sales Activity Starting with Industrial, Office, Apartments & Retail • Review of Lender Survey & Positive Trends

Typical Industrial Sales Activity 2009 Total Industrial Sales 2008: 87 Average Price / SF: $39.23 Average Size / Sale: 15,873 SF

Industrial Survey Results • CBRE – Market Overview 3rd Qtr 2009 • Overall Vacancy Rate 12.55% 1st Qtr – Jumped 13.9% 3rd Qtr • -- (8% in the West / 17% in the North) • Industrial Rental Rates $4.22 to $5.16 with Avg @ $4.81/SF NNN • -- (Down 4% or $0.20/SF on Average – Tenants have Control) • Absorption – Negative 946,951 SF YTD • -- (However - 300,000 SF New Constriction-Tire Rack in Windsor) • Cushman & Wakefield – Market Beat 2nd Qtr 2009 • Overall Vacancy Rate 12.1%, up from 10.2% (1,395 Buildings Surveyed) • Absorption – negative 1,230,681 +/- SF • Rental Rates - $4.37/SF to $4.70/SF, NNN – declining • Jump in Vacancy due to a Couple of Large Users Closing – 3,000 jobs in Enfield lost

Apartment Trends • Marcus & Millichap 3rd Qtr 2009 • 2007: 3,263 Units Sold For $240,789,000 or $73,794/Unit • 2008: 1,500 Units Sold For $128,196,000 or $85,464/Unit (perception unemployment would increase demand for rental units as single-families were foreclosed) • 2009: 1,226 Units Sold For $87,630,375 or $71,477/Unit • Total Decline: 3% To date • Reporting 2.9% decline in asking rents and 1.3% increase in vacancy

Hartford County Retail Market Few Large Retail Sales 825-875 Queen St, Southington Sold August 2009 for $16,500,000 171,989 SF built 1969 on 17.6 Acres 97% Occupied / 10.45% OAR All Cash Deal – Bob’s Discount, Fashion Bug, Outback, Ruby Tuesday, Radio Shack, TJ Maxx, Bed, Bath & Beyond, Golden Nails, plus others Couple Smaller Retail Sales 7 Mill Pond Drive, Granby sold June 2009 $2,000,000 or $181.52/SF – Built 2004 11,018 SF Building on 1.89 Acres Previous sale May 2005 for $170.45/SF 2009 OER: 9.75% 2005 OER: 8.25%

What Are Lenders Doing?Hartford County Market – Fall 2009 • Tighter Terms Becoming Accepted As Norm • Loan-To-Value Ratios 65% - 75%- Only One Stated 80% • Results in Higher Debt Service Coverage Ratios – 1.25x and up – preferably 1.3x 1.35x – Some over 1.4x • Points – ½ to a 1.5 points or more • Rates – Spreads all increased and tied to FHLBB 5 yr mostly – 5 year fixed – fewer pre-payment clauses • Securing Triangle between Lenders-Appraisers-Ordering Function • Recourse is now the Norm • Overall Cash Analysis on Borrower – Slowing Approval Process • Why – less competition – Lack of Non-regulated Funding • Conduit Market – Restructuring – CMBS? • Small Markets – Short Sales – Work it out • Unlike Early 1990’s – There are Fewer Banks to Take Property Back • Regulations – OK to have Performing Loans With LTV of 100% +

What is Different Between1991-1992 and 2009-2010 • Regulators Perspective – Letting Lenders Create Work Out situations Instead of Foreclosing - (May be the one Factor the Downturn is Short-lived on Commercial Side) • Fewer Banks – Less Speculative Lending • Businesses are More Global Oriented due to Internet – Communications – Acceptance • Low Inventory of Property – Less Speculative Building • Back to More Sensible Investor Expectations – (more weight on return over longer holding period as opposed to increasing rents and then a quick resale)

Thank you …& Think Positive Andrews & Galvin Appraisal Services, LLC 16 Spring Lane, Farmington, CT john@agvalues.com 860-677-5522