Download

1 / 21

210 likes | 245 Vues

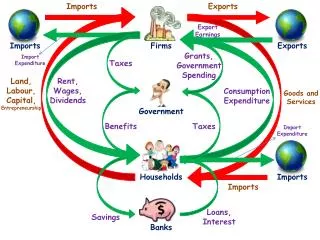

Taxation of households. Stuart Adam Institute for Fiscal Studies. Outline. Earning Spending Saving. Taxation of earnings. Key lessons from the past 30 years: Hours of work are inelastic Participation is elastic for some groups Low-skilled mothers The young and the old

E N D

Taxation of households Stuart Adam Institute for Fiscal Studies

Outline • Earning • Spending • Saving

Taxation of earnings Key lessons from the past 30 years: • Hours of work are inelastic • Participation is elastic for some groups • Low-skilled mothers • The young and the old • Optimal tax models developed to incorporate this • Taxable income elasticities matter at the top • Effort, form of remuneration,… • Little scope for raising top tax rates?

Taxation of earnings • Hours of work are inelastic • But marginal rates above 95% still too high! • So reduce benefit / tax credit withdrawal rates • Participation is elastic for some groups • And incentives for low-paid work are very weak • So increase working tax credit • And start means-testing at higher earnings

Taxation of earnings • Problem: less aggressive means-testing increases the number subject to means tests • More people facing high marginal rates • But the intensive margin matters less • More people facing admin and take-up problems • Take-up problem eased if more people entitled? • Look at administrative reform: return tax credits to fixed awards? Integration of benefits / tax credits / income tax?

National Insurance • Has become very much like income tax • Either make it a proper social insurance system • Or merge it with income tax • Reduced admin and compliance costs • Transparency • Significant barriers • Assessing pension entitlements • Employer contributions and the self-employed

Indirect taxes • Starting-point: Atkinson & Stiglitz (1976) • If income-related tools are available for redistribution, no equity rationale for commodity tax differentiation • If leisure weakly separable from all other goods, no efficiency rationale either • Otherwise, tax complements with leisure more • Other arguments for non-uniformity • Externalities • Merit goods • Goods produced not in a competitive market • Difficult-to-tax services • Other arguments for uniformity • Practical: definitions and misrepresentation • Political: reduce scope for special pleading

VAT • The UK zero-rates far more than other countries • Main distribution-motivated breaks seem unjustifiable • Food, children’s clothes, domestic fuel • Could compensate the poor via higher child benefit, pensions and tax allowances and still have money left over • Others are more defensible • Medicines, cycle helmets, supplies to charities, financial services • There is a case for some new ones – childcare? • Two plausible approaches • Rationalise the rate structure – raises substantial net revenue, but not necessarily fewer departures from uniformity • Radical simplification – New Zealand shows almost perfect uniformity achievable

VAT The EU context is important in two areas: • Restrictions on the UK rate structure • And on supply-side subsidies as an alternative • Missing trader fraud • Fraction of VAT is collected at each point in the supply chain, so any one trader gains little by evading • But exports are zero-rated, so an importer can disappear with the VAT on the whole value • Stop zero-rating exports: set an EU-wide minimum (VIVAT)

Taxation of saving Again, start with Atkinson & Stiglitz (1976)… • Saving just defers consumption • A tax on saving means taxing earnings spent tomorrow more than earnings spent today • Under certain conditions, this decision to delay consumption tells us nothing about ability to earn • So taxing saving is an inefficient way to redistribute • Tax those with high earnings/spending, not those who choose to spend their earnings later

On the other hand… Conditions for Atkinson-Stiglitz don’t hold: • If work decisions depend on the timing of consumption • If consumption substitutes for leisure then tax retirement saving to encourage work • If high-ability people have higher saving rates (eg more patient, longer life expectancy) • Then saving indicates high ability, not just consumption preferences • In a dynamic setting with uncertainty • e.g. if private productivity information received after savings decisions, a tax on wealth of those who claim low productivity in 2nd period discourages mimicking low productivity • Outside standard life-cycle savings models • Credit constraints; myopia; self-control problems; framing effects

Practical applicability • Convincing arguments that the zero-tax result is not robust • But little guidance as to the ‘correct’ optimal tax rate! • Consumption tax advocates (Meade, Bradford) did not primarily argue on the basis of theoretical optimality: “the attraction of an expenditure tax is not so much that it would remove a disincentive to saving in general but that it offers a practicable way of eliminating the differential taxation of particular forms of saving and capital income” Kay & King (1990), p.96

A tax on capital income? We might like to tax the accrued real return. But… • Hard to measure real returns in some cases • Taxing nominal returns means an ‘inflation tax’ • Hard to measure accrued capital gains • Taxing realized gains distorts towards delaying realization • Hard to identify an individual’s income within certain pooled savings vehicles • Problematic if we want a progressive tax schedule • Hard to measure the return to ‘investment’ in durable goods • notably housing • Hard to separate capital from income in some cases • eg annuities

How might we not tax saving? • Present value of lifetime earnings and expenditure are the same if all saving earns the normal return r • Ignoring bequests: a tricky issue! So three obvious mechanisms: • Just tax earnings: National Insurance contributions • Just tax expenditure: VAT • Tax expenditure, calculated as: earnings – net contributions into saving accounts • In all cases, no tax on the return that converts earning today into spending tomorrow

Earnings or expenditure? • Not all saving earns the normal return • Does this matter? Depends why return varies… • Risky returns don’t change much • If people can scale up holdings of risky assets • Not quite equivalent as tax isn’t proportional • Rents do change things • Exceptional returns due to market power, factors in fixed supply, etc • Often efficient to tax these • How much of these are at the corporate level? • Expenditure tax captures higher (or lower) returns automatically • We could also do it explicitly… • Tax savings income above a normal rate of return • Robust to at least some of the problems of a capital income tax

Tax smoothing • Pensions are taxed as deferred earnings • But the tax rate faced in retirement may be different • 40% tax in work, 22% tax in retirement • 59% tax + tax credit taper in work, 22% tax in retirement • 22% tax in work, 40% (or higher) benefit withdrawal in retirement • Can make pensions very attractive or unattractive • and favour strategic timing of pension contributions • Lifetime tax depends on the timing, as well as the level, of earning and spending • Seems both unfair and distortionary

If you can’t beat it, join it • Tax smoothing is inevitable as long as both earnings-tax and expenditure-tax vehicles exist • But implementing a consistent regime is difficult • Hard to apply earnings tax to defined-benefit pensions • Hard to apply expenditure tax to savings under the bed • With unlimited choice, everyone could smooth their tax base completely • This gives us a lifetime tax! • Almost: uncertainty is again a tricky issue

Pensions • Broadly expenditure tax treatment • But more generous • 25% tax-free lump sum • Employer contributions escape NICs at both ends • Why? Pensions need special inducement… • Must lock in the money until retirement • Compulsory annuitisation • May well be good reasons for this • But is the inducement well designed? • Why a percentage of the fund? • Why favour lump-sum withdrawal? • Why favour employer contributions? • Why related to rate of NICs?

Housing • Durables normally have VAT up front • Same present value as on stream of services • But new build zero-rated • Turnover is tiny – transition would take forever! • And value of housing services changes a lot • So tax annual consumption value instead • A reformed council tax • Possible role for other taxes too • Exceptional capital gains? • Land value? • Definitely no stamp duty!

Gifts and bequests • Starting point: transfer of tax base, or income/spending of both? • Altruism vs warm glow vs gift exchange • Accidental bequests tax bequests more than gifts? • Equality of opportunity tax function of age gap? • Lots of awkward margins • Bequests vs death-bed vs lifetime • Need threshold, but progressivity manipulation • Giving children money vs education vs clothes

Taxation of households Stuart Adam Institute for Fiscal Studies