Download

1 / 13

240 likes | 1.65k Vues

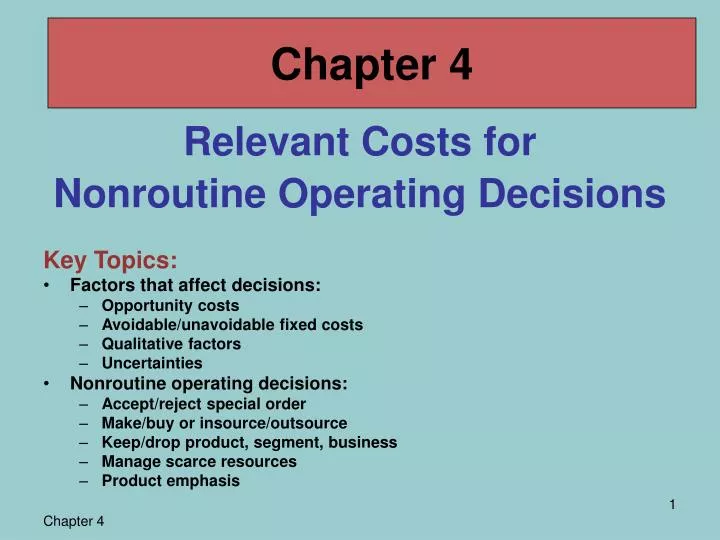

Chapter 4. Relevant Costs for Nonroutine Operating Decisions. Key Topics: Factors that affect decisions: Opportunity costs Avoidable/unavoidable fixed costs Qualitative factors Uncertainties Nonroutine operating decisions: Accept/reject special order Make/buy or insource/outsource

E N D

Chapter 4 Relevant Costs forNonroutine Operating Decisions Key Topics: • Factors that affect decisions: • Opportunity costs • Avoidable/unavoidable fixed costs • Qualitative factors • Uncertainties • Nonroutine operating decisions: • Accept/reject special order • Make/buy or insource/outsource • Keep/drop product, segment, business • Manage scarce resources • Product emphasis

Process for Non-routine Operating Decisions • Notice: The above exhibit combines the material from Chapters 2, 3, and 4 • See Exhibit 4.4 in Chapter 4 for a summary of decision rules and key factors for each type of nonroutine decision

Opportunity Costs • Opportunity cost is the profit forgone by choosing one alternative versus another • Examples: • Rent revenue lost by a landlord in the decision to use an apartment for storage • Forgone interest income when funds are used for a project instead of invested

Avoidable/Unavoidable Fixed Costs • Sometimes a decision alternative can reduce fixed costs • Examples of avoidable fixed costs: • Store manager’s salary if store is closed • Insurance on production equipment if production is outsourced and equipment is sold • Examples of unavoidable fixed costs: • Rent on excess floor space (assuming no alternative use) • Salary of CEO if one store is closed

Qualitative Factors • Examples of qualitative factors: • Effect on brand name • Employee reactions • Ability to deliver • Supplier quality • Focus on core competencies • Customer service • How can you learn to identify qualitative factors: • Classroom problems • “Real world” decisions

Uncertainties • Examples of uncertainties in non-routine decisions: • Revenue and cost estimates • Interpreting quantitative results • Relevant range of operations • Qualitative factors • Dependence among product lines • Alternative uses for capacity • Why is it important to consider uncertainties? • How can you learn to identify uncertainties?

Linear Programming Solution Using Solver • Determine the contribution margin for each product and create the objective (target) function to be maximized • List the amount of constrained resources required per product and the total amount of constrained resources available; Create formulas for the resource constraints • Set up an Excel spreadsheet • Use Excel Solver to maximize the objective function • Interpret the Solver output