Download

1 / 31

320 likes | 502 Vues

The Next Generation of Earnings Management – Cash Flow Manipulation. July 25, 2007 New York City. Anthony Catanach. Associate Professor and Carnegie Fellow Villanova University. Council Member Biography

E N D

The Next Generation of Earnings Management – Cash Flow Manipulation July 25, 2007 New York City Anthony Catanach Associate Professor and Carnegie Fellow Villanova University

Council Member Biography • Dr. Catanach is a professor in the Villanova University School of Business, as well as a visiting professor in accounting and control at INSEAD. His teaching and research interests relate primarily to business risk management, financial statement analysis, and earnings management issues. He has been a licensed Certified Public Accountant since 1980 and a Certified Management Accountant since 1991. • His professional experience includes five years as an audit manager with KPMG and six years in the banking industry. While in public accounting, he provided auditing, tax, and consulting services to the financial services industry. Upon moving to the banking industry, Dr. Catanach worked as a chief financial officer and chief operating officer for several large bank holding companies. He has delivered executive programs for numerous professional, private, and public organizations in the United States, Europe, and Asia, and currently serves as a national instructor for several global professional services firms. • In addition to being a Pew Scholar and Carnegie Fellow, he has received numerous awards for his research, teaching, and curriculum innovation efforts, and is currently co-editor of Advances in Accounting Education. © 2007 Gerson Lehrman Group Inc., All Rights Reserved

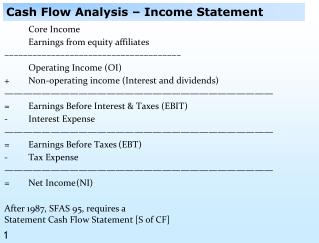

Table of Contents • The increasing trend of overstating operating cash flows • Examples of creative cash flow disclosures • A checklist to assess the quality of OCF disclosures © 2007 Gerson Lehrman Group Inc., All Rights Reserved

Increasing number of global firms have been found guilty of overstating operating cash flows (OCF). • General Motors, Ford – misclassification of loans • Rite Aid, Halliburton – securitization transactions • General Mills, Universal Security – investment returns • Managers realize that analysts are scrutinizing OCF given recent revenue recognition and restatement issues. • Analysts need sustainable OCF numbers for forecasting. • But accounting rules (both US GAAP and IFRS) allow companies to massage the presentation of their cash flows in the financial statements.

General framework will be an investigation of: • Overdrafts – are they operating or financing? • Investment securities – affect of classification on OCFs? • Notes receivable – does the type of receivable affect cash flow reporting? • Receivable securitization – operating, investing, or financing activity? • Other cash flow reporting games – • Is the company delaying its liability payments? • Does the company “play games” with formatting its SCF?

Overdrafts are a financing agreement since a company owes money to a BANK, not VENDORS. • Potential Problems with Overdrafts • US GAAP - Classifying overdrafts as accounts payable (operating activities) leads to potential over and understatements of operating cash flow when the indirect method is used. • IFRS – Can be offset against cash and cash equivalents thus bypassing disclosure in SCF.

Orthodontic Centers of America Financing Activity So How Does This Affect OCF? Source: OCA, 10-K, 2003

Source: OCA, 10-K, 2003 Difference between total accounts payable and accrued expenses in 2002 to 2003. OCF overstated because an increase in overdrafts reduces this number. OCF for the period should really be $47,001!

$947 Million in Bank Overdrafts Hidden In Balance Sheet and Debt Note

Potential Problems With Investment Securities • Investment classification choices (trading, available-for-sale (AFS), or hold-to-maturity (HTM)) depend on intent. • Classification presents potential problems in the statement of cash flows when non-financial companies report trading securities as operating activities (even though GAAP), because these transactions are not likely to recur.

Nautica Enterprises, Inc. Source: Nautica, 10-K, 2002 Let’s see how this was reported in previous years…

Source: Nautica, 10-K, 2000 This resulted in the overstatement of OCF by $28.4 million (57%) in FYE 2001 and $21.1 million (34%) in FYE 2000.

Receivable Classification and Securitization also pose cash flow reporting problems • Manufacturing companies commonly finance sales to its own customers (dealers). These are operating activities. They also finance sales to dealers’ customers. These are investing activities. Companies commonly report changes in all financing receivables as investing activities. If dealer financings are reported as investing activities, this may overstate OCF. • In a securitization, receivables are pooled and an undivided interest in the pool is sold, thus creating a security backed by receivables. Securitization is accounted for as a sale of receivables, so the proceeds are reported as OCF. Are these are temporary or permanent boosts to OCF? Are securitizations really financings?

General Motors Corporation Source: GM, 10-K, 2003 How much of this net investment in receivables should be investing vs. operating?

According to the FY 2003 receivables note: GM overstated OCF by $4.1 billion (117%) in FYE 2003. Increase should be reported as a deduction when using the indirect method. Source: GM, 10-K, 2003

Look at What GM’s FYE 2004 Notes Say… Source: GM, 10-K, 2004

Source: 2006 20-F (US GAAP) The issue here is whether these cash flows are really operating or financing…

Source: 2006 20-F (US GAAP) Net change in finance receivables for 2006 861,703 ¥225,374 of the increase is related to wholesale loans that should be reported in OCF! So, OCF are really ¥2,290,106 rather than ¥2,515,480 as originally reported…this is almost a 10% overstatement in 2006 OCF!

But that’s not all…what about the receivable “sales?” Source: 2006 20-F (US GAAP) Are these “sales” of retail receivables really “sales,” or should they be considered borrowings? Also, are the “sales” a normal part of recurring operations to generate cash? Can they be considered OCF?

Source: Halliburton, 10-K, 2003 Halliburton overstated OCF by $180 million (13%) in FYE 2002. Note the reversal in 2003, clearly a financing transaction.

Company’s have begun manipulating reported operating cash flows by substituting changes in operating assets and liabilities for changes in current assets and liabilities. Source: HCA, 10-K, 2006 None of the changes tie to the balance sheet either!

Source:Fair isaac 2006 10K This Company is violating GAAP format AND slowing payments!

Other OCF Reporting Issues • Capitalized Operating Costs - Certain costs can be either capitalized or expensed, e.g., construction period interest, software development costs, etc. If capitalized, these cash outflows are reported as investing cash flows, thus overstating OCF. • Insurance Reimbursements - Cash receipts from insurance settlements related to long-term asset investments (buildings, plants, etc.) should be reported as investing inflows, not OCF. • Acquisitions - Changes in current assets and liabilities must be adjusted for effects of acquisitions to avoid potential understatement of OCF.

Other OCF Reporting Issues (continued) • Vendor Related Payables - Determine if OCF are increasing because payment on vendor payables is slowing. Financing provided by a supplier in the form of a note is reported as an increase in OCF rather than a financing inflow. • Income Tax Considerations - Taxes payments or refunds related to non-operating items (i.e. investment activities) are typically included in OCF. Tax benefits associated with stock option deductions are considered OCF. However, benefits may reflect either cash inflows or a deferred tax asset. • Non-Recurring Operating Transactions - Restructuring charges, etc.

Beware of IFRS Flexibility in Formatting! Source: Experian 2006 Interim Report Note that Net Income is NOT reconciled to OCF!

A Useful Checklist of Things to Consider: • Compare net income and operating cash flows. • Identify and investigate large and unusual reconciling items. • Test reconciling amounts by tracing balances to differences in balance sheet and note disclosures. • Verify that reconciling items relate only to operating assets. • Scrutinize OCF to assess their reasonableness given the company’s operations and potential manipulation strategies: • Are inflows related to decreases in receivables, inventories, and prepaids? • Are inflows related to increases in payables and accruals.

About GLG Institute GLG Institute (GLGiSM) is a professional organization focused on educating business and investment professionals through in-person meetings. It is designed to revolutionize the professional education market by putting the power of programming into the hands of the GLG community. GLGi hosts hundreds of Seminars worldwide each year. GLGi clients receive two seats to all Seminars in all Practice Areas. GLGi’s website enables clients to: • Propose Seminar topics, agenda items and locations • View and RSVP to scheduled and proposed Seminars • Receive a daily briefing with new posts on your favorite tickers, subject areas and from trusted Council Members • Share Seminar details with colleagues or friends © 2007 Gerson Lehrman Group Inc., All Rights Reserved

Gerson Lehrman Group Contacts Debbie Liston, CPA Senior Research Manager Accounting & Financial Analysis (AFA) Gerson Lehrman Group 850 Third Avenue, 9th Floor New York, NY 10022 212-880-6527 dliston@glgroup.com Christine Ruane Senior Product Manager Gerson Lehrman Group 850 Third Avenue, 9th Floor New York, NY 10022 212-984-8505 cruane@glgroup.com © 2007 Gerson Lehrman Group Inc., All Rights Reserved

IMPORTANT GLG INSTITUTE DISCLAIMER – By making contact with this/these Council Members and participating in this event, you specifically acknowledge, understand and agree that you must not seek out material non-public or confidential information from Council Members. You understand and agree that the information and material provided by Council Members is provided for your own insight and educational purposes and may not be redistributed or displayed in any form without the prior written consent of Gerson Lehrman Group. You agree to keep the material provided by Council Members for this event and the business information of Gerson Lehrman Group, including information about Council Members, confidential until such information becomes known to the public generally and except to the extent that disclosure may be required by law, regulation or legal process. You must respect any agreements they may have and understand the Council Members may be constrained by obligations or agreements in their ability to consult on certain topics and answer certain questions. Please note that Council Members do not provide investment advice, nor do they provide professional opinions. Council Members who are lawyers do not provide legal advice and no attorney-client relationship is established from their participation in this project. You acknowledge and agree that Gerson Lehrman Group does not screen and is not responsible for the content of materials produced by Council Members. You understand and agree that you will not hold Council Members or Gerson Lehrman Group liable for the accuracy or completeness of the information provided to you by the Council Members. You acknowledge and agree that Gerson Lehrman Group shall have no liability whatsoever arising from your attendance at the event or the actions or omissions of Council Members including, but not limited to claims by third parties relating to the actions or omissions of Council Members, and you agree to release Gerson Lehrman Group from any and all claims for lost profits and liabilities that result from your participation in this event or the information provided by Council Members, regardless of whether or not such liability arises is based in tort, contract, strict liability or otherwise. You acknowledge and agree that Gerson Lehrman Group shall not be liable for any incidental, consequential, punitive or special damages, or any other indirect damages, even if advised of the possibility of such damages arising from your attendance at the event or use of the information provided at this event. © 2007 Gerson Lehrman Group Inc., All Rights Reserved