Download

1 / 15

150 likes | 401 Vues

International Debt Markets (or part II of chapter 13). Agenda. What is Eurocurrency ? International debt market instruments: Bank loans & Syndicated Credits. Euro-note Market Instruments. International Bond Market Instruments. Project financing. Eurocurrency Markets.

E N D

International Debt Markets (or part II of chapter 13)

Agenda • What is Eurocurrency? • International debt market instruments: • Bank loans & Syndicated Credits. • Euro-note Market Instruments. • International Bond Market Instruments. • Project financing.

Eurocurrency Markets • Eurocurrencies: domestic currencies of one country on deposit in 2nd country. • Pros:flexible maturities & higher yields & gov’t regulation-free. • E.g.:Eurosterling, Euroeuro,Euroyen, Eurodollar. • Eurodollar deposits =/= demand deposits! • Can’t transfer by check. • Underlying balance kept @ US correspondent bank. • History: why Eurocurrency market so popular? • Eastern-Europe holders post-WW2 deposited US$ funds in London. • Central banks kept reserves in Eurodollar deposits. • 1957: Bank of England imposed tight controls on sterling lending. • 1960s: US BOP problems segmented US debt market.

Bank Loans & Syndications (floating-rate, short-to-medium term) International Bank Loans. Eurocredits. Syndicated Credits. Euronote Market (floating-rate, short-to-medium term) Euronotes. Eurocommercial Paper (ECP). Euro Medium Term Notes (EMTN). International Bond Market (fixed & floating-rate, medium-to-long term) Eurobond. - straight fixed-rate issue. - floating-rate note (FRN). - equity-related issue. Foreign Bond: Yankee, Samurai. International Debt Markets

Bank Loans & Syndicated Credits • Eurocredits • Loans denominated in eurocurrencies & extended by banks in countries other than country of denominating currency. • Tied to LIBOR. • Short-term maturities: ~ 6 months. • Narrow spreads, usually less than 100 basis points. • Syndicated credits • Arranged by lead bank w/ other banks participation. • Interest expense tied to LIBOR. • Upfront fee. • Commitment fee (on unused portion).

Euronote Market • Medium- & short- term debt instruments. • Two types • Underwritten facilities. • Non-underwritten facilities: Euro-commercial paper (ECP) & Euro Medium-term notes (EMTN) • Euronote • Short-term, negotiable promissory notes in eurocurrency. • E.g.: Revolving Underwriting Facility & Note Issuance Facility. • Cheaper than syndicated loans. Why? • Euro-commercial paper (ECP) • Maturities of 1,3, & 6 months. • Euro Medium-term notes (EMTN) • Maturities: 9 months to 10 years. • Allows continuous issuance. • Coupons paid on set calendar dates. • Issued in small chucks ($2-5m).

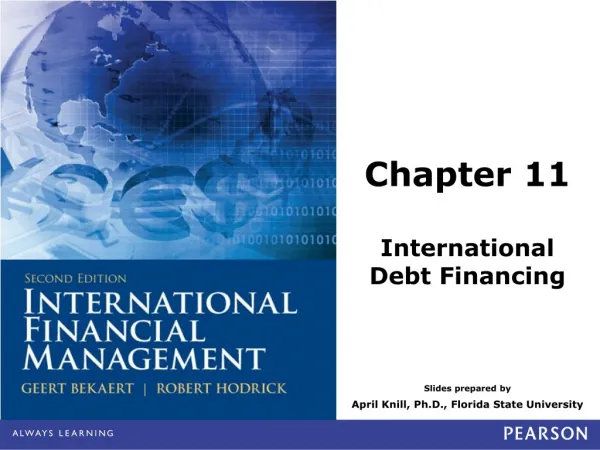

International Bond Market • World bond market 50% larger than world equity market. • Bonds currencies 2001: US$ (49%), Euro (37%) & Yen (5%). • Popular: no regulatory interference, lax disclosure, tax anonymity. • Bond types: • Eurobonds • Sold to investors in national capital markets other than country of denominating currency. • E.g. Evian (France) issues $-denominated bonds in UK & Japan. • Types: • Straight Fixed-rate issue. • Floating rate note (FRN). • Equity related issue – convertible bond. • Foreign bonds • Sold w/in country of denominated currency, however issuer is from another country. • E.g. Air Portugal offers bond in US priced in $. • Include: Yankee bonds (sold in US), Samurai bonds (Japan), & Bulldogs (UK).

Currencies to denominate bonds? Source: BIS Quarterly Review, December 2002

Types of Eurobonds issued? Source: BIS Quarterly Review, December 2002

Eurobonds • Straight Fixed Rate Debt • “Plain vanilla” bond w/ specified coupon & maturity. • Most Eurobonds are bearer bonds => coupon dates annual.Why? • Vast majority (65+%) of new international bond offerings are straight fixed-rate. • Floating Rate Notes (FRN) • Like adjustable rate mortgage. • Allows shifting interest rate risk to borrower. • Reference rates are 3- & 6-month US$ LIBOR. • Equity-Related Bonds • Convertibles • Allow exchange bond for shares in issuer’s firm. • Sell @ lower coupon rate of interest. Why? • Bonds w/ equity warrants • Allow holder keep bond & buy shares in issuer’s firm @ specified price.

Eurobond Credit Ratings • Main providers: Moody’s, Fitch, Standard & Poor’s. • Moody’s:nine categories from Aaato C. • Investment grade ratings: Aaa Baa. • Focus on default risk, not exchange rate risk. • Default rate is higher for foreign currency debt than local currency debt. • Inflation is key factor.

US Regulation on Int’l Bonds • Eurobonds: US citizen cannot buy them in US primary market => U.S. citizen could buy on secondary market. • Yankee bonds: Yankee bonds sold to US citizens are registered. • Bearer vs. Registered: No registration for bearer bonds. => Investor anonymity. Opens door for tax evasion… • Tax Concerns: until 1984, US had 30% withholding tax on interest to nonresident holder of US T-bonds.

Project Financing • Financing arrangement for long-term, large-scale capital projects, generally w/ high risk. • Used by MNE in development of infrastructure projects in emerging markets • Projects highly leveraged (60+% debt). Why? • Scale of project precludes single equity investor. • Many projects funded by governments.

Project Financing Characteristics • Separation of project from its investors • Project legally & financially separate. • Allows project to obtain own credit rating & cash flows. • Long-lived & capital intensive • Cash flow predictability from third-party commitments • Third party commitments are usually suppliers or customers of project • Finite projects with finite lives

Things to remember… • What is Eurocurrency? • International debt market instruments: • Bank loans & Syndicated Credits. • Euro-note Market Instruments. • International Bond Market Instruments. • Project financing.