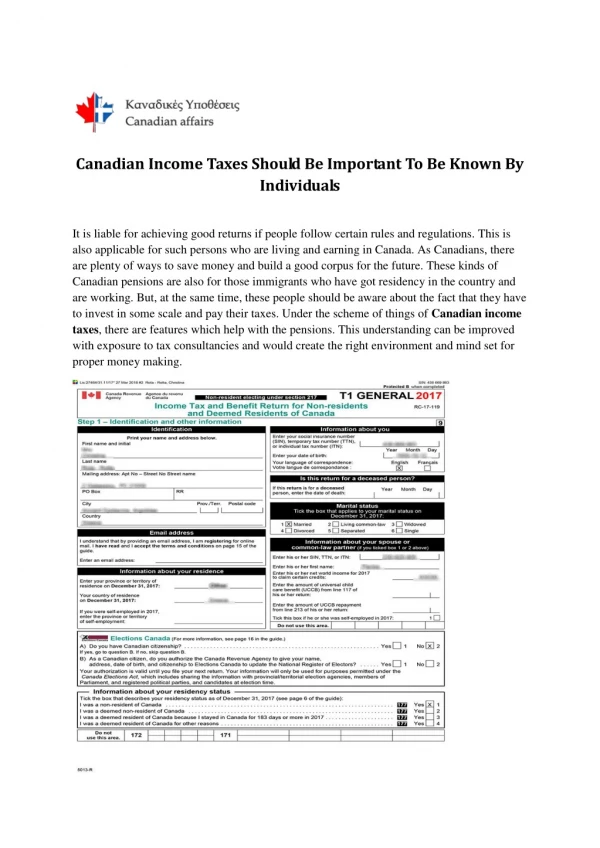

Download

1 / 17

190 likes | 650 Vues

FRS 112 Income Taxes. Introduction : This chapter deals with the computation of tax expense that is deferred and not with the computation of tax payable according to the tax rules The differences in taxable profit and accounting profits are either permanent items or temporary items.

E N D

FRS 112 Income Taxes Introduction: • This chapter deals with the computation of tax expense that is deferred and not with the computation of tax payable according to the tax rules • The differences in taxable profit and accounting profits are either permanent items or temporary items

1.Malaysian Tax System • Companies are allowed to deduct tax on dividends paid provided they have sufficient tax credit • Tax credit = gross - net dividend • Refer example on ABC on page 210 where there is a tax credit on investment income

2.Introduction to Deferred Tax (“DT”) • The difference in the tax payable (based on taxable income) and tax expense (based on accounting profit) is due to timing differences • Timing / temporary differences (“TD”) = certain expenses may not be allowable deductions and certain income are not taxable in the current period but may be deductible / taxable in the next period • Permanent difference are ignored in the computation of DT • Refer example on TD (pg 212 to 213) and illustration (pg 213)

Before FRS 112 was formulated, there were alternate methods of treating DT as follow:- • - Flow through (nil provision) • where tax payable = tax expense • - Limited or partial provision • where DTL does not crystallise,no provision is required • provide to the extant of the liability will probable become payable • - Full provision • Recommended by FRS 112

3 Accounting for DT • 3.1 Underlying Principles • DTL - if the recovery of the carrying amount of the asset or liability gives rise to a higher tax payment in future • DTA - if the recovery of the carrying amount of the asset or liability gives rise to a lesser tax payment in future • Recognition:- • - income statement (if due to CA and depreciation) • - revaluation reserve (if due to revaluation surplus) • - Goodwill (if arising on business combination)

3.2 Taxable TD (“TTD”) and Deductible TD (“DTD”) • TD are differences between the carrying value (“CV”) of assets and liabilities in the balance sheet and the tax base (“TB”) • DT is calculated based on “balance sheet liability method” on all TD. PD are ignored • TTD = CV of assets > TB or • TTD = CV of liabilities < TB, give rise to DTL • DTD = CV of assets < TB or • DTD = CV of liabilities > TB, give rise to DTA • Refer example on pg 217 and example 1

4 Recognition of DTL • DTL = Tax rate X TTD • DTL is not recognised on PD • Some depreciable assets may not qualify for CA because on initial recognition of an asset or liabilities, the tax rule do not recognise them as asset or liability. As such, TB=0 and no DTL [S14(b) exemption] • Para 14, The following TTD do not give rise to DTL: • -Goodwill for which amortisation or impairment is not deductible for tax purpose

-The initial recognition of an asset or liability in a transaction which: • -- is not a business combination, and • -- at the time of the transaction, affects neither accounting profit nor taxable profit 4.1 Assets Carried at FV • The surplus on revaluation is not subjected to tax and the TB is not adjusted, CV>TB (para 19) • For non-depreciable property, the surplus is subject to RPGT only. If not intend to dispose, provide at the minimum rate of 5%. Example: Freehold land, CV>TB (para 20) • Para 21, For a building which no not enjoy CA

-The TB on initial recognition is nil and NO DTL is recognised [Para 14 (b) exemption] • - However, if the building was revalued, the surplus will give rise to TTD • -If not commitment to sale , DTL at current income tax rate • - If there is a commitment to sale , DTL at current income tax rate (based on the additional depreciation arising from the surplus in the intervening periods prior to the date of the disposal) plus RPGT • Refer example 2

4.2 Business combination • The cost of the business combination is allocated to the FV of the identifiable net assets plus contingent liabilities, that may be different from the carrying value and TB. • This will give rise to TD and affect the goodwill on consolidation • TB for goodwill = 0, but DTL is NOT recognised [Para 14 (a) exemption]

4.3 Compound Instrument • The interest charged in the income statement and the amount paid will differ • Only the amount of interest paid will qualify for tax deduction • On initial recognition of the liability, there will be a difference between CV and TB • Refer example 3

5. Recognition of DTA • DTA is recognised only IF it is probable that taxable profits will be available against which the DTD can be utilised • The following DTD do not give rise to DTA: • -Negative goodwill • -The initial recognition of an asset or liability in a transaction which: • -- is not a business combination, and • -- at the time of the transaction, affects neither accounting profit nor taxable profit • Refer example of DTD on page 224 to 225

6.Measurement • DT is calculated at the current tax rate • 6.1 Change in tax rate • Where there is a change if tax rate, the DTL b/f is adjusted for the change through income statement • It is a change in accounting estimate and so the retained profit is not adjusted • The carrying amount of the DTA is to be reviewed at each balance sheet date • 6.2 Discounting • DTA / DTL are not discounted

6.3 Items credited or charged directly to equity • If DT related to equity items, then the DT is accounted for in the reserve and not the income statement • Refer example on page 226 • Refer example 4 & 5

7 DT arising from a business combination • TD may arise especially where the FV of assets is different from the CV and TB. • The acquirer will generally recognise the DTA and DTL as identifiable assets and liabilities, thus affect the goodwill • Refer example 6

7.1 DTA on Losses of Acquirer • Acquirer having trade losses • Find it probable to recover the tax losses against future taxable profits of the acquiree • DTA recognised by acquirer will affect the computation of goodwill • 7.2 DTA on Losses of Acquiree • Acquiree having trade losses • The gross amount of goodwill is adjusted for DTA • However, the acquirer cannot recognise a negative goodwill nor increase negative goodwill by the subsequent adjustment for the DTA • Refer illustration

8 Presentation and Disclosure • Pls read page 231 • Pls refer notes to financial statements