Download

1 / 40

400 likes | 526 Vues

Regulation and Regulatory Reforms in Developing Countries. Antonio Estache European School on New Institutional Economics ESNIE 2009 Cargèse May 2009. Overview. Focus on regulation in key infrastructure industries Some background data on the main reforms of the last 15 years

E N D

Regulation and Regulatory Reforms in Developing Countries Antonio Estache European School on New Institutional Economics ESNIE 2009 Cargèse May 2009

Overview • Focus on regulation in key infrastructure industries • Some background data on the main reforms of the last 15 years • A zoom on regulatory reforms • A further zoom on the institutional dimensions of regulatory reform in developing countries

The reforms of the 1990s • Three main “standard” reforms: • Relying more on competition • In the market when possible • For the market otherwise • End to old fashion self-regulation when regulation was still needed • create “independent” regulatory agencies • deal more explicitly with the incentives for efficiency in the design of regulation (i.e. replacing cost + by price caps) • Opening up to private sector to get access to private financing to fasten service coverage increases

Mixed to poor success of the efforts to attract the private sector…% of countries with Private Participation in Infrastructure (2004)

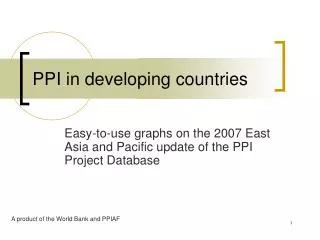

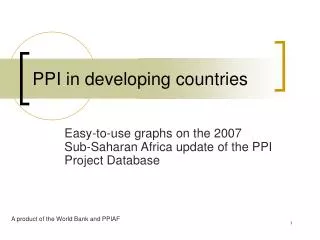

Investment commitments to infrastructure projects with private participation in developing countries in real and nominal terms, 1990–2007 Total: US$1,475 billion committed through +/- 4,100 projects… adds up to less than 20% of the investment in the sector…. 158 144 111 Source: World Bank and PPIAF, PPI Project Database.

Telecoms and energy dominate investments levels 2007 US$ billions Source: World Bank and PPIAF, PPI Project Database.

Energy and transport dominate the number of projects Projects Source: World Bank and PPIAF, PPI Project Database.

East Asia and Latin America are the favorite destinations 2007 US$ billions Source: World Bank and PPIAF, PPI Project Database.

One slide on the crisis and infrastructure investments…not good news… Private flows to LDCs forecast PPI in infrastructure et PIB growth 2007 US$ billions Percentage US$ billions Source: World Bank and PPIAF, Impact of the financial crisis on PPI database, PPI Projects database, and Institute of International Finance.

The regulation independence war also only enjoyed only a mixed success(% of countries with Independent Regulatory Agency)

In a nutshell….How did it work out? • Fiscal cost: ok in short term but not ok over the longer run • Efficiency: reasonably ok although increased shift from price caps to hybrids dominated by strong costs pass thru rules • Equity: key problem and essentially a regulatory design issue • Accountability: not good either…and again a regulatory design issue

The winners and losers in terms of Actors • The actors in the payoff matrix • The users (access: (+ but not as much as expected and distributional issues), affordability(-), quality (+)) • The taxpayers (cash!: + in SR, -/+ in LR) • The workers (jobs + cash: - in SR, + in LR) • The operators (cash in the SR and IRR> COC in the LR for a few! (+ in SR, ? for LR) • The local owners (cash! + in SR and LR) • The foreign owners (cash! + in SR, +/- in LR) • The bankers (cash! + in SR and LR) • The politicians (cash! + in SR and LR) • The donors (???)

Emerging Issues • For users: • Residential users: Distributional issues • Non-residential users: could do much better • For operators: • Demand uncertainty • Cost levels revisions to address overruns • Projects design revisions • Exchange rate risks and other economic shocks • De facto expropriation risks • For government: • Uncertainty about demand and costs! • Uncertain net fiscal effects • Fiscal space: the illusion of private sector invest • Weak regulatory capacity, commitment and strong capture • But counterfactual may be worse!

How can regulation theory help in the diagnostic and …how can it help fix things?

First: recognize a few basic principles emerging from theory… • Information asymmetry matters and can matter a lot! • When a regulated operator has privileged information: it usually gets a rent from it • Information asymmetry seems to be a much bigger issue in LDCs • Rents exist…but are not necessarily bad! • Regulation can be designed to get operator to use the rent (within limits…) in a Pareto improving way • Limited commitment ability of a regulator is an essential driver of the effectiveness of regulation in terms of efficiency, equity and fiscal costs • It may be a good idea to limit a regulator’s powers to avoid undue use of information through capture associated with a limited ability to commit 15

How can these issues be modeled? Ideally, we need a general model to see how a monopolist will behave to maximize rent from weak institutional capacity But we need to make sure that the main institutional capacity issues generally recognized by experts on LDCs can be addressed explicitly within the model This also means we need to explicitly separate the regulator from the government to check for regulator specific problems In addition, we want try to reconcile the policy recommendations emerging from research focusing on narrow issues using issues specific models 16

So what are the institutional weaknesses we need to track down? A survey of policy and theoretical literature identifies: Limited capacity/skills to regulate Limited accountability Limited ability to commit Limited enforcement capacity Limited fiscal efficiency Each of these dimensions needs to hit on a specific variable in the general model 17

Some basic stylized facts on these institutional weaknesses? (1) • Limited capacity to regulate or to enforce • Regulators are severely under-resourced … • … which can lead to increased firm rents. • Limited commitment • Many contracts have been renegotiated… • … tends to increase the cost of capital… • … but could this effect have been decreased by independent regulation… • … and better checks and balances??? 18

Some basic stylized facts on these institutional weaknesses? (2) • Limited accountability • Regulators (and governments) are often not accountable… • … which decreases efficiency and inequality • Limited fiscal space • High cost of public funds… • … partly explains why SOEs have not expanded network enough… • … but increasing access is not profitable for privatized firms… • … partly because of conflicts between affordability and access… • … independent regulation appears to help 19

A Basic Model of Monopoly Regulation:(1)The Monopolist • Monopolist produces a quantity q of a good with a fixed costs of F and a marginal cost of C(q) • Monopolist cost-function is also driven by: • e = firm effort (i.e. moral hazard variable) • Exerting effort e causes firm disutility of ψ(e) (ψ’>0 , ψ’’>0 , ψ’’’ ≥ 0 ) => this is the controlable part of costs • β = underlying cost outside of firm’s control (i.e. adverse selection variable such as technology or factor prices=> this is the uncontrolable part of costs • β= β (low cost) with probability v, or high cost with probability 1-v. C(q) = (β-e)q + F • Monopoly utility is U = qp - (β-e)q – F – Ψ (e) + t With p=price and t=transfer • Participation constraint: U>0 (once β is revealed) 20

A Basic Model of Monopoly Regulation:(2) Consumers • Consumer welfare: • S(q) = gross surplus = • P (q) = inverse demand function • λ >0 is the opportunity cost of public funds • Consumers maximize welfare p=P(q)=S’(q) (3) Government • Benevolent government welfare function: • Government always observes F & c = (β - e) • !!!but government does not observe not β or e (i.e. composition of cost) • In order to learn β and e, the government employs a regulator… 21

A Basic Model of Monopoly Regulation: (4) The Regulator • Intuitively, the idea is that the main focus of the regulator is the cost function and the variables it can control β and e • The firm’s cost βis revealed to the regulator with probability ξ • If the regulator learns β,it chooses whether or not to reveal it to the government • Signal is `hard information’ – i.e. regulator cannot report a cost-level that it has not observed • Government can incentivise regulator to reveal signal by paying s if β is revealed • Social cost is λs due to cost of public funds • Firm can incentivise regulator to hide signal by paying bribe • Such side-transfers are illegal and hence costly=> regulator receives only a fraction 0 < k < 1 of bribe • We assume the gvt decides on the set of contracts offered to the firm BEFORE the regulator makes its report on costs => gvt can influence regulator’s choice on info revelation 22

Complete Institutions Benchmark:Symmetric information • In this version, the country does not suffer from any of the 4 institutional weaknesses • If regulator reveals β, there is symmetric information Government maximizes welfare W, s.t. binding participation constraints (PC) dW/dq=0 leads to usual markup price over mrgnal costs ( = elasticity of demand) =>since for a given β, the only variable the regulator can focus on is effort (e) => dW/de=0 to get the optimal effort the gvt aims which leads to - ψ’(e)=q (i.e. efficient effort) - U=0 (i.e. no rent) => Price is set above MC to cover for cost of transfers which is itself set to avoid any rent and H or L firms efforts are both optimal 23

Complete Institutions Benchmark: Now…Asymmetric information (1) • If regulator does not reveal β: • Asymmetric information • For a firm to be interested in any offer by the gvt, the offer has to satisfy the incentive compatibility constraints (ICC) • Here and • i.e. firm is incentivized to reveal β truthfully • Std result: the binding PC is for high cost firm and ICC is for low cost firm • Low cost firm is given positive rent: ; • an information rent which does not apply to high cost firm 24

Complete Institutions Benchmark:Asymmetric information (2) • Now…if regulator reveals information, low cost firm gets no rent • Low cost firm has incentive to bribe the regulator to keep β hidden • Willing to bribe regulator up to • Government is willing to pay conditional transfer to regulator to prevent the regulator accepting bribe, i.e. • Regulator only get k with 0<k<1 due to transaction costs • Paying the regulator allows the gvt to avoid a cost to society of λk ; rent given to firm is costly to society since there is opportunity cost of public funds • Now we can calculate the optimal gvt choice of q and e • Do so by computing the expected welfare E(W) given ξ and v • dE(W)/dq=0 and get usual markup formula for price • And…dE(W)/de=0 and get a complex formula (2) 25

Complete Institutions Benchmark:Asymmetric information (3) • What does this equation mean????, • Marginal disutility to effort of the firm (ψ’) can be impacted by a set of variables of relevance to the government • This includes the fact that the rent that the low cost firm receives is costly to society (comes from distortive taxation) • The gvt wants to minimize it • To reduce the rent, the gvt can make the high cost firm production (q) level less appealing to the low cost firm (work on e and hence Ø(e)) 26

Complete Institutions Benchmark:Asymmetric information (4) • We end up with an actual level of effort is lower than the efficient one • The 2nd term is increasing in v since the more likely the firm is to be low cost, the less likely the distortion in effort will occur and hence the gvt can allow the distortion to be greater • Note: gvt can act directly on cost looking at effort BUT it can also introduce an incentive scheme to get the firm to do the right thing on its own • Rather than setting p, cost or transfers, the gvt can set the price and come up with a reimbursement rule which makes the firm decide on the optimal effort level to max the rent (from low powered to high powered) • Note: in this particular model, the level of incentive is equivalent to the level of effort 27

Now we have a model…so what? • Let’s use the model to review the impact of each institutional weakness and the optimal policy response to each weakness • Let’s see how consistent these various optimal policies • Let’s see how these optimal policies match the standard policies recommended and often adopted by regulators in developing countries

What if limited regulatory capacity? • Limited regulatory capacity implies • (a) lower ξ , the proba that the regulator observes the firms’ type or • (b) no observation of C = (β - e) • So what? • (a) From equation (2), lower ξimplies higher powered incentives needed since collusion btw firm and regulator occurs less often and hence anti-collusion payments less of a concern • (b) Non-observation of c implies high-powered incentives by definition – price caps are the only option • => less capacity makes a stronger case for high powered incentive regulatory regimes 29

What if limited accountability? (1) • Less accountability of the regulator can imply greater value of k(the cost to the government to cut the ease of making bribes) Less likely to be optimal to prevent capture because so expensive to do so Lower social welfare and greater frequency of capture • Assume that with probability ζ regulator is `dishonest’ and will take bribes and with probability 1- ζ is `honest’ and will not …but the gvt does not know the regulator type Strange result…with less accountability…may no longer necessarily be optimal to prevent regulator’s capture through payments to this regulator! 30

What if limited accountability (2) • Now what if the problem of limited accountability is not about the regulator but about government non-benevolence? • Less accountability of government can thus be modelled as greater value ofγ => can be modelled as misaligned objective function and favouring of firm over consumers: W=V+γU • Government favoring of firm implies cares less about rent, hence lower distortion of effort: • Now E(W) also includesγ and dE(W)/de=0 leads to drivers of marginal disutility to effort of the firm (ψ’) as follows: greater γresults in higher powered incentives to cut costs =>but associated with higher risks of regulatory capture… 31

What if limited accountability (3) • So do we have any solutions??? • 1. recognize that limited accountability is mainly due to lack of information flows between actors! • 2. this means that we need to reduce the importance of information that any agents holds • 3. this can be achieved for instance by • Lowering the power of incentives (cost plus looks good!) • But also by the creation of new information sources (get multiple regulatory agencies to generate competition for the generation of information) • …but not easy if you have limited capacity… 32

What if limited commitment (1) 3 forms: (i) too much renegotiation, (ii) non respect of promises to firm and (iii) limited enforcement willingness => inefficiency ex-post and all firms will pretend to be high costs and hence gvt needs of give up more rent to get the right ones on board => high risk when need to make long term investments If firm invests Ito influence β, it increases the probability that it will be a low cost firm i.e. ν= ν(I) (ν’>0, v’’<0) If government can commit to rents at time of investment, will set firm’s payoffs to account for all surpluses as follows: However, if no commitment, firm only considers private payoffs, hence =>Limited commitment therefore implies under-investment NOTE: it will also lead to “ratchet effect” (if the firm reveals its type to be low cost, it knows the gvt will be more demanding => added incentive NOT to reveal information => gvt could increase welfare by promising not to use info! 33

What if limited commitment? (2) So…solutions? Note again: gvt led renegotiations are common (unhappy with high firm profits) => odds are driven by size of rent => government can only commit to give a maximum expected rent (let’s call it c) If not satisfied, gvt needs to reduce e => To satisfy this ICC, the gvt may have to favor lower incentives! This is because the threat of renegotiation constrains its ability to offer the firm the possibility of making large profits! =>in practice, this means that limited commitment may require also a reduction in power of incentives since need to give more rent than it otherwise would have to get the firms to participate in the business NOTE: empirical evidence suggests that price cap are more associated with renegotiation than cost-plus 34

What if limited commitment? (3) • More solutions? • Nationalization…since gvt end up happy with the rent they now control…=> tolerate higher profits! • Increase debt financing since gvt has to tolerate more interest payment than it tends to tolerate dividends • Increase independence of regulator • The fact is that each form of lack of commitment tends to lead to its own solution! 35

What if limited fiscal efficiency? (1) • If no money for direct subsidies…a natural solution are cross subsidies (across people or across regions) • Consider two regions – rich (1) and poor (2) • In region 2, only a share θof the population are connected. • Let Fi , ci , qi , pi be the fixed cost, marginal cost, quantity per capita and price in region i, and let F2= F2(θ) (F2’>0, F2’’>0) => F2 a fct of share of people connected • Write welfare function F W=S(q1) +λ q1 .p1 - (1+λ)(c1.q1 – F1) +θS(q2) +θλ q2 .p2 - (1+λ)(θc2.q2 – F2 (θ)) • dW/dθ=0 => (3) • Differentiate this to get • This tells us that the optimal size of network shrinks as fiscal efficiency shrinks! 36

What if limited fiscal efficiency? (2) • Solutions??? Look at a typical problem • Imagine rural area more costly, i.e. c2 > c1 , =>ideally: p2>p1 • BUT uniform price restriction to “help” the poor rural area i.e. implies rather than p2 = (1+λ)c2 • However, (from (3)) this reduces network size • With no government-firm transfers, instead of (3) we have • => there is a trade-off between affordability and access • Hence when 1+λ >μ, need cross-subsidies targeted to network expansion to increase network expansion 37

CONCLUSIONS • We know from experience that the real impacts of the various institutional limitations discussed can be large • Main real problem is that the solutions available are imperfect and OFTEN contradictory • Moreover, we still have huge gaps in our understanding of issues • No real serious link between finance and regulation in this field • Moreover, good solutions for LDCs often need to follow a different path from that taken in developed countries • Thus insufficient and possibly damaging to advocate simply for a regulatory framework that is closer to some universal ideal. • …and a lot more work to do on this topic! 40