Download

1 / 36

360 likes | 522 Vues

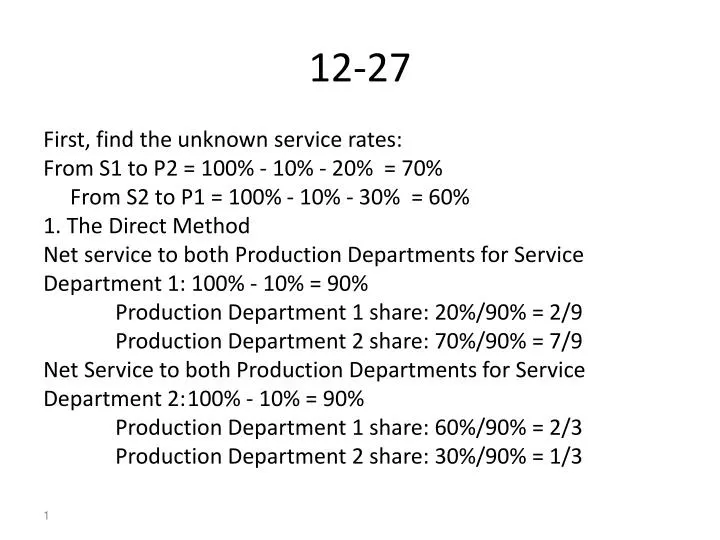

12-27. First, find the unknown service rates: From S1 to P2 = 100% - 10% - 20% = 70% From S2 to P1 = 100% - 10% - 30% = 60% 1. The Direct Method Net service to both Production Departments for Service Department 1: 100% - 10% = 90% Production Department 1 share: 20%/90% = 2/9

E N D

12-27 First, find the unknown service rates: From S1 to P2 = 100% - 10% - 20% = 70% From S2 to P1 = 100% - 10% - 30% = 60% 1. The Direct Method Net service to both Production Departments for Service Department 1: 100% - 10% = 90% Production Department 1 share: 20%/90% = 2/9 Production Department 2 share: 70%/90% = 7/9 Net Service to both Production Departments for Service Department 2: 100% - 10% = 90% Production Department 1 share: 60%/90% = 2/3 Production Department 2 share: 30%/90% = 1/3

Direct Method Production department 1 Production department 2 Service department 1 $180,000 x 2/9 = $40,000 $180,000 x 7/9 = $140,000 cost allocation Service department 2 $60,000 x 2/3 = $40,000 $60,000 x 1/3 = $20,000 cost allocation Add: Initial Production $50,000$120,000 Dept. Costs Total Cost for Each $130,000 $280,000 Production Dept.

Step MethodService Dept 1 goes first on the basis that it has the highest total cost: Service Dept 2 Production Dept 1 Production Dept 2 Allocation of Service Dept 1 $180,000 x .1 $180,000 x .2 = $36,000 $180,000 x .7 = $126,000 = $18,000 Allocation of Service Dept 2 ($60,000 + $18,000) ($60,000 + $18,000) x 2/3 = $52,000 x 1/3 = $26,000 Add: Initial Production $50,000 $120,000 Dept Costs Total Cost for Each $138,000 $272,000 Production Department

12-35 1. Physical Unit Method (10,000 total units) $80,000 x 5,000/10,000 = $40,000 allocated to X $80,000 x 4,000/10,000 = $32,000 allocated to Y $80,000 x 1,000/10,000 = $ 8,000 allocated to Z X Y Z . Allocated Cost $40,000 $32,000 $ 8,000 Additional Cost 9,000 7,000 8,000 Total $49,000 $39,000 $16,000 Unit Cost $9.80 $9.75 $16.00 Sales Price $11.00 $11.25 $30.00 Unit Gross Profit $1.20 $1.50 $14.00

12-35 2. Sales Value at Split off Method (total sales value at split off $90,000) $80,000 x $25,000/$90,000 = $22,222 allocated to X $80,000 x $41,000/$90,000 = $36,445 allocated to Y $80,000 x $24,000/$90,000 = $21,333 allocated to Z X Y Z . Allocated Cost $22,222 $36,445 $21,333 Additional Cost 9,000 7,000 8,000 Total $31,222 $43,445 $29,333 Unit Cost $6.244 $10.861 $29.333 Unit Gross Profit $4.756 $.389 $ .667

SCHMIDT MACHINERY COMPANYAnalysis of Operating ResultsJune 2007 Flexible Master Actual Budget Budget Unit sales 9009001,000 Sales (900 x $840) $756,000 $720,000 $800,000 Total variable expenses 414,000405,000450,000 Contribution margin $342,000 $315,000 $350,000 Fixed expenses 180,000150,000150,000 Operating income $162,000 $165,000 $200,000 Total Master (Static) Budget Variance $38,000U Flexible-budget Sales Volume Variance Variance $3,000U $35,000U

13-37 (1) (2) Actual Purchases Actual Purchases at Actual Cost at Standard Cost (AQ) x (AP) (AQ) x (SP) (3,350 lbs. x $30/lb.) (3,350 lbs. x $25/lb.) Purchase Price Variance = (1) – (2) = $16,750U (3) Actual Usage Flexible-Budget at Standard Cost Amount (AQ) x (SP) (SQ) x (SP) (3,375 lbs. x $25/lb.) (3,600 lbs. x $25/lb.) Usage Variance = (2) – (3) = $5,625F

13-37 (1) (2) (3) Actual Input Flexible-budget Actual Input Cost at Standard Cost Amount (AQ) x (AP) (AQ) x (SP) (SQ) x (SP) (4,200 hrs. x $42/hr.) (4,200 hrs. x $40/ (4,500 hrs. x $40/hr.) Quantity (Efficiency) Price (Rate) Variance = (1) - (2) Variance = (2) - (3) = $8,400U = $12,000F Total Flexible-Budget Variance = (1) - (3) = $176,400 - $180,000 = $3,600F

Class problem Bluecap Co. used a flexible budget system. The following information pertains to 2007 which was prepared at the 80% level of operation: Number of units 8,000 Total standard direct labor hours 24,000 Flexible budget variable factory overhead $103,200 Total factory overhead rate per direct labor hour $15.10 This implies that overhead is being applied on the basis of direct labor hours and that it takes 3 hours for each product (24,000 hours/8,000 products

Class problem In preparing a budget for 2008 Bluecap decided to raise the level of operation to 90% to manufacture 9,000 units for 27,000 direct labor hours. During 2007, Bluecap spent 28,000 direct labor hours and manufactured 9,600 units. The actual factory overhead was $14,000 greater than the flexible budget amount for the units produced, of which $6,000 was due to fixed factory overhead. The total budget for fixed factory overhead in 2008 is: A) $230,400. B) $259,200. C) $265,200. D) $276,480. E) $288,000.

Class problem In preparing a budget for 2008 Bluecap decided to raise the level of operation to 90% to manufacture 9,000 units for 27,000 direct labor hours. During 2007, Bluecap spent 28,000 direct labor hours and manufactured 9,600 units. The actual factory overhead was $14,000 greater than the flexible budget amount for the units produced, of which $6,000 was due to fixed factory overhead. The total budget for fixed factory overhead in 2008 is: A) $230,400. B) $259,200. Same as 2007 Calculated total overhead rate per hour x budgeted hours - budgeted variable overhead or ( $15.10 x 24,000 hours) – 103,200 = 362,400 – 103,200 C) $265,200. D) $276,480. E) $288,000.

Class problem The standard fixed overhead application rate in 2008 is: A) $4.30 per direct labor hour. B) $4.50 per direct labor hour. C) $6.90 per direct labor hour. D) $9.30 per direct labor hour. E) $9.60 per direct labor hour.

Class problem The standard fixed overhead application rate in 2008 is: A) $4.30 per direct labor hour. B) $4.50 per direct labor hour. C) $6.90 per direct labor hour. D) $9.30 per direct labor hour. E) $9.60 per direct labor hour.

Class problem The standard fixed overhead application rate in 2008 is: A) $4.30 per direct labor hour. B) $4.50 per direct labor hour. C) $6.90 per direct labor hour. D) $9.30 per direct labor hour. E) $9.60 per direct labor hour. $252,900/27,000 hours

Class problem The standard variable overhead application rate in 2008 is: A) $4.30 per direct labor hour. B) $4.50 per direct labor hour. C) $6.90 per direct labor hour. D) $9.30 per direct labor hour. E) $9.60 per direct labor hour.

Class problem The standard variable overhead application rate in 2008 is: A) $4.30 per direct labor hour. Same rate as 2007 $103,200/24,000 hours B) $4.50 per direct labor hour. C) $6.90 per direct labor hour. D) $9.30 per direct labor hour. E) $9.60 per direct labor hour.

Class problem The total flexible budget overhead variance in 2008 is: A) $11,440 unfavorable. B) $14,000 unfavorable. C) $15,040 favorable. D) $17,280 favorable. E) $17,440 unfavorable.

Class problem The total flexible budget overhead variance in 2008 is: A) $11,440 unfavorable. B) $14,000 unfavorable. Given C) $15,040 favorable. D) $17,280 favorable. E) $17,440 unfavorable.

Class problem The variable overhead spending variance in 2008 is: A) $ 6,000 unfavorable. B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. E) $17,440 unfavorable.

Class problem The variable overhead spending variance in 2008 is: A) $ 6,000 unfavorable. B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. AQ x AH - AH x SQ 9,600 x 3 x $4.3 + $8,000 - $28.000 x $4.30 $131,840 - $120,400 E) $17,440 unfavorable.

Class problem The factory overhead spending variance in 2008 using a three-variance analysis is: A) $ 3,200 favorable. B) $11,440 unfavorable. C) $15,040 favorable. D) $17,280 favorable. E) $17,440 unfavorable.

Class problem The factory overhead spending variance in 2008 using a three-variance analysis is: A) $ 3,200 favorable. B) $11,440 unfavorable. C) $15,040 favorable. D) $17,280 favorable. E) $17,440 unfavorable. Variable + fixed $11,440 + 6,000

Class problem The variable overhead efficiency variance in 2008 is: A) $ 3,440 favorable. B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. E) $17,200 unfavorable.

Class problem The variable overhead efficiency variance in 2008 is: A) $ 3,440 favorable. AH x SR - SH X SR 28,000 x $4.30 - 9,600 x 3 x $4.30 $120,400 - $123,840 B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. E) $17,200 unfavorable.

Class problem The fixed overhead spending variance in 2008 is: A) $ 6,000 unfavorable. B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. E) $17,440 unfavorable.

Class problem The fixed overhead spending variance in 2008 is: A) $ 6,000 unfavorable. Given B) $ 8,000 unfavorable. C) $ 9,200 favorable. D) $11,440 unfavorable. E) $17,440 unfavorable.

Class problem The fixed overhead production volume variance in 2008 is: A) $11,280 favorable. B) $17,280 favorable. C) $28,800 unfavorable. D) $34,800 unfavorable. E) $57,840 favorable.

Class problem The fixed overhead production volume variance in 2008 is: A) $11,280 favorable. B) $17,280 favorable. Budgets FO - FO Aplied = $259,200 - 9,600 x 3 x $9.60 = $259.200 - $276.480 C) $28,800 unfavorable. D) $34,800 unfavorable. E) $57,840 favorable.

Assignment • For next class do 14-30 Part 1, 14-31Parts 1 & 2 and 14-32 Part 1

14-31 2.Fixed factory overhead (FOH) flexible-budget variance = FOH spending variance = $2,000U

14-32 • Standard Variable factory overhead rate per direct labor hour: = $15,000/2,500 hours = $6.00/DLH Standard fixed factory overhead rate per direct labor hour: = $90,000/2,500 hrs. = $36.00/DLH Standard factory overhead rate per direct labor hour (DLH) $42.00/DLH Standard direct-labor hours (DLH) per unit: = 2,500 hours/5,000 units = 0.5 DLHs per unit

14-32 Spending variance from 14-30 and 14-31 Variable $ 600F Fixed 2,000U Total $1,400U Variable efficiency variance = $1,800U Fixed Production volume variance = $3,600U