Download

1 / 0

80 likes | 1.93k Vues

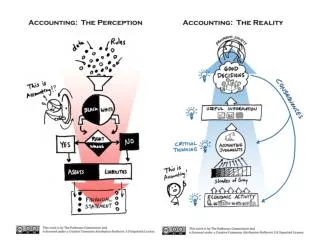

Chapter 11 DEPRECIATION, IMPAIRMENTS, AND DEPLETION Sommers – Intermediate I. Is Accounting Helpful for Valuation?. Conceptual Framework (FASB)

E N D