Download

1 / 4

40 likes | 170 Vues

Chapter 6 Questions. Q1. What is an “Interest Rate” and to which kind of financial instrument does it apply? A1. It is the price that lenders receive from borrowers who use their money provided through a debt instrument (i.e., a loan in the form of a promissory note, or a long-term bond). The

E N D

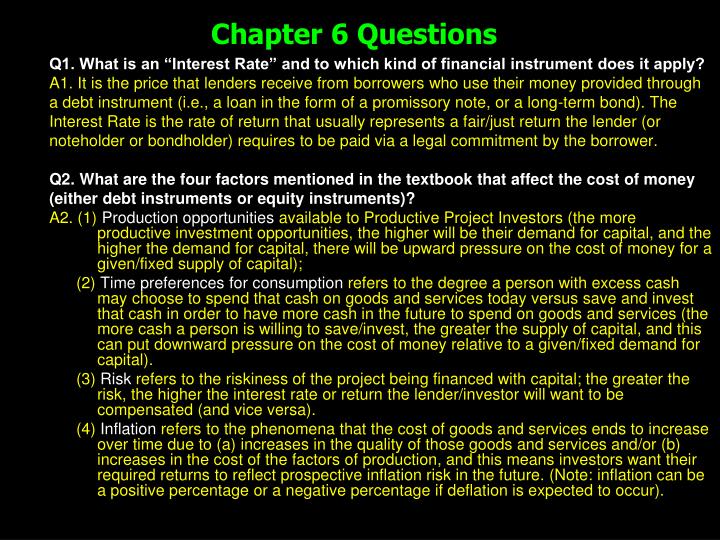

Chapter 6 Questions Q1. What is an “Interest Rate” and to which kind of financial instrument does it apply? A1. It is the price that lenders receive from borrowers who use their money provided through a debt instrument (i.e., a loan in the form of a promissory note, or a long-term bond). The Interest Rate is the rate of return that usually represents a fair/just return the lender (or noteholder or bondholder) requires to be paid via a legal commitment by the borrower. Q2. What are the four factors mentioned in the textbook that affect the cost of money (either debt instruments or equity instruments)? A2. (1) Production opportunities available to Productive Project Investors (the more productive investment opportunities, the higher will be their demand for capital, and the higher the demand for capital, there will be upward pressure on the cost of money for a given/fixed supply of capital); (2) Time preferences for consumption refers to the degree a person with excess cash may choose to spend that cash on goods and services today versus save and invest that cash in order to have more cash in the future to spend on goods and services (the more cash a person is willing to save/invest, the greater the supply of capital, and this can put downward pressure on the cost of money relative to a given/fixed demand for capital). (3) Risk refers to the riskiness of the project being financed with capital; the greater the risk, the higher the interest rate or return the lender/investor will want to be compensated (and vice versa). (4) Inflation refers to the phenomena that the cost of goods and services ends to increase over time due to (a) increases in the quality of those goods and services and/or (b) increases in the cost of the factors of production, and this means investors want their required returns to reflect prospective inflation risk in the future. (Note: inflation can be a positive percentage or a negative percentage if deflation is expected to occur).

Chapter 6 Questions Q3. What has been the historical levels of interest rates in the U.S. (1) 1972 to 1981, (2) 1981 to 2003, (3) 2003 to 2006/07, and (4) 2007 to 2009? A3. (1) 1972-1981: Increasing dramatically from moderately low levels to historically highest levels (due to inflation and high demand for borrowing); (2) 1981-2003: Steadily decreasing from highest levels to historically lowest levels (due to inflation being brought under control, U.S. federal budget deficits being reduced dramatically to zero, a recession in ‘01-’03); (3) 2003-2006/07: Steadily increasing (due to increasing U.S. federal budget deficits plus a strengthening U.S. economy meant the economy could afford more normally higher levels of interest rates); (4) 2007-2009: Dramatically reduced interest rates to lowest levels (due to the unusual financial crisis of 2007-08 and resulting dramatic economic slowdown by Productive Project Investors). Q4. Theoretically, what are the determinants of market interest rates (i.e., the main component variables or factors which comprise an interest rate)? A4. (1) The Risk-Free Inflation-Free “Real” Rate of Return (2) The Inflation Risk Premium (“IRP”) (3) The Maturity Risk Premium (“MRP”) (4) The Default Risk Premium (“DRP”) (5) The Liquidity Risk Premium (“LRP”) [ Not mentioned in text: (6) The Tax Risk Premium (“TRP”) A U.S. Treasury Bill is used to represent (1) + (2), and a Long-Term U.S. Treasury Note/Bond us used to represent (1) +(2) + (3), as these are considered to have 0% DRP

Chapter 6 Questions Q5. Compute the Real Interest Rate for a U.S. Treasury Bill if the Inflation Risk Premium is 1.00% for the next 12 months and the nominal stated interest rate for a U.S. Treasury Bill is currently 2.50%. (Assume U.S. Treasury debt obligations have a credit rating of AAA+). A5. Real Rate = 2.50% less 1.00% = 1.50% Q6. Compute the Interest Rate (stated nominal rate) for a U.S. Treasury Note (5-year maturity) and a U.S. Treasury Bond (30-year maturity) if the current U.S. Treasury Bill Interest Rate is 2.50% and the Maturity Risk Premium (5-years) is 1.75% and the Maturity Risk Premium (30-years) is 3.25%. (Assume U.S. Treasury debt obligations have a credit rating of AAA+ and assume Inflation is expected to average 1.50% for the next 2 years, then average 3.00% for the next 30 years). A6. U.S. Treasury Note (5-year) = 2.50% + 1.50% incremental IRP + 1.75% = 5.75% U.S. Treasury Bond (30-years) = 2.50% + 1.50% incremental IRP + 3.25% = 7.25% This illustrates that longer-term debt instruments usually have a higher interest rate versus shorter-term debt instruments due to higher Inflation Risk Premiums and higher Maturity Risk Premiums (and could also have higher LRPs and DRPs).

Chapter 6 Questions Q7. What does the phrase “Term Structure of Interest Rates” mean? A7. Term Structure refers to the difference between short-term debt instruments versus longer-term debt instruments, and the fact that interest rates on longer-term debt instruments are normally higher than shorter-term interest rates due to the greater risks (interest rate volatility risks = MRP; default risks = DRP; liquidity risks = LRP, etc.) that longer-term debt instruments represent for investors in longer-term debt instruments. Q8. What macroeconomic factors are mentioned in the textbook that can influence the size of investors’ required risk premiums (Inflation Risk Premium, Maturity Risk Premium, Default Risk Premium, Liquidity Risk Premium, and Tax Risk Premium)? A8. (1) U.S. Federal Reserve System policy; (2) U.S. federal government budget deficits or surpluses; (3) International factors (trade and investment in/out of the U.S.); (4) Business Activity (economic growth versus recession).