Download

1 / 2

20 likes | 26 Vues

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

E N D

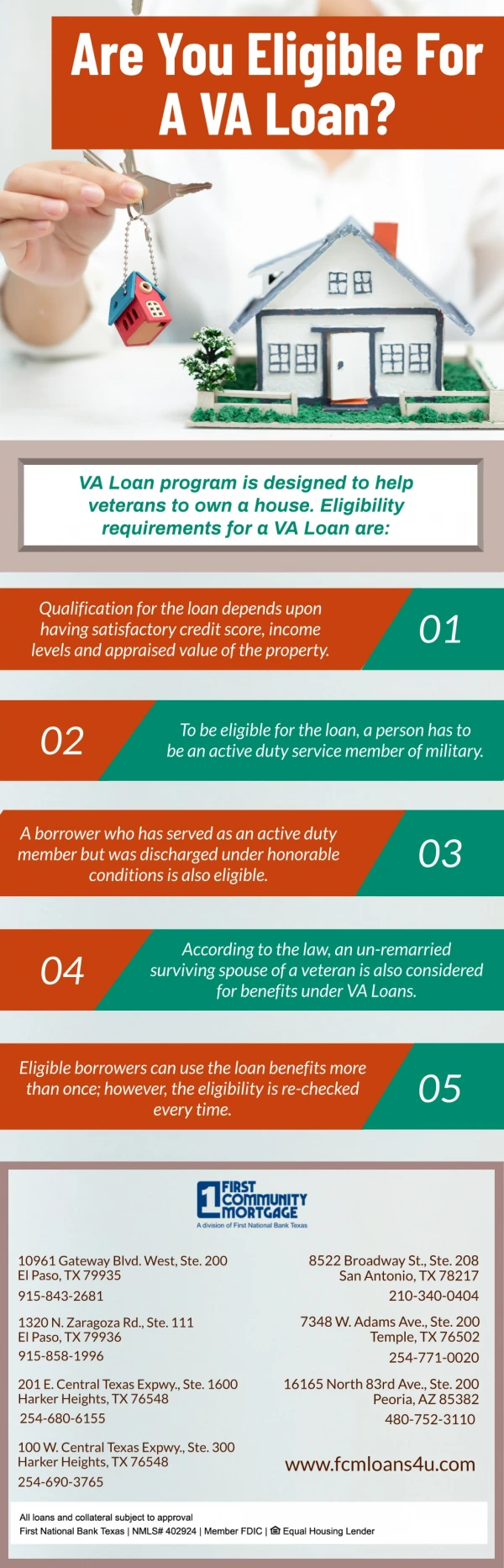

How Do You Qualify for a VA Loan? Buying a home is a great investment, an effective way to build long-term wealth, and an effective hedge against inflation. When buying a home, most people will need to take out a mortgage to finance their purchase. And complete VA loan qualifications. And, while there are many different mortgage programs available to consumers, veterans have an extra option. Which is designed specifically to help them buy real estate. That is the VA Home Loan program. VA Loan Qualifications Overview A VA home loan is a mortgage loan that is guaranteed by the Veteran’s Association. Making them a low risk option for lenders, which allows them to offer attractive rates to borrowers. These types of loans are guaranteed by the VA. But can be received through banks, savings and loans providers, and mortgage companies. The VA loan products available offer the same options as traditional mortgages. Including adjustable rate mortgages, fixed rate mortgages, second mortgages, and refinanced mortgages. While VA home loans are normally used to buy single family homes. They can also be used to purchase condos, townhomes, or even manufactured housing. Service Time Requirements Once a loan is approved and booked it acts just like any other mortgage. However, the VA loan qualifications process is much different than the process for a traditional mortgage. The main qualification that all borrowers must satisfy is related to the amount of time in the service. To qualify for a VA home loan, you must have 90 days of consecutive service in the US Armed Forces during wartime, 181 days of consecutive service during peacetime, or have spent more than six years in the National Guard or National Reserves. The VA program is also available to the spouse of a service member who passed away in the line of duty or as a result of a disability related to an incident that occurred while in service.

Certificate of Eligibility (COE) When looking to purchase a home by taking out a VA home loan, the first thing you should do is apply for and receive a Certificate of Eligibility also known as a “COE”. A COE is a certificate that will provide lenders with verification that you have met all the service obligations necessary to qualify for a VA home loan. The certificate application can be received from either a VA Loan specialist or directly through the Veteran’s Association. Other Requirements Beyond providing a COE that proves your service-time qualifications, you will also have to meet other various qualifications set forth by the VA. The Veterans’ Association does not necessarily follow the same rigid underwriting guidelines that a bank or mortgage company does, but they do have some underwriting rules that they tend to follow. In most cases, the VA will want a borrower to have a housing debt-to-income ratio of 41% or lower, which is higher than most banks offer. However, the VA will also spend more time reviewing your “after expense monthly cash flow” to ensure you have enough money to meet your basic expenses. The VA will also take into consideration your credit score, although they do not have the same requirements for a high credit score as a bank does.