Download

1 / 18

180 likes | 378 Vues

Fair Value Accounting: Volatility and Smoothing. Allan Brender ETH Zurich 7 June 2004. The Story of a Company’s Financial Progress. Investors require a standard basis for this story to have comparability among companies Hence, IOSCO pressure on IASB

E N D

Fair Value Accounting:Volatility and Smoothing Allan Brender ETH Zurich 7 June 2004

The Story of a Company’s Financial Progress • Investors require a standard basis for this story to have comparability among companies • Hence, IOSCO pressure on IASB • Establish uniform international standards for financial reporting, for all business activities

The Story of a Company’s Financial Progress • Financial statements and reporting have uses other than to inform investors: • Regulation • Taxation • Management compensation • These can lead to distortions and manipulation of the system

International Accounting Standards Board • Establish international financial reporting standards or international GAAP • Standards are for business activities • Standards for insurance contracts, not insurance companies • Some insurance company products (e.g. deferred annuities) are not insurance contracts • Some elements (e.g. equalisation reserves) will not be considered to be liabilities

Financial Instruments • IAS 32, 39 – financial instruments (other than insurance contracts) • IAS 32: disclosure and presentation • IAS 39: recognition and measurement

Measurement of Value • If a financial asset is held to maturity, it can be measured at amortised cost • Trading is not a consideration here • IASB’s general position is that most assets and financial liabilities can be traded; market value should be the measurement standard

Market Value or Fair Value • An active market in a particular financial asset or liability may not exist • Determine fair value, the price that willing arm’s-length buyer and seller might agree to • The value of certain exotic assets is determined through use of models – questionable • Revision to IAS 39 : verifiable market value

IAS 39 • Hold to maturity – value at amortised cost • Available for sale – market value, but changes do not pass through profit or loss (until time of sale) • Trading – value at market with changes passing through profit or loss • New proposed fair value option

IFRS 4 – Insurance Contracts • Phase 1(2005): • Continue current liability valuation • Do not net reinsurance • Phase 2 (?): • Forward-looking valuation • Assumptions: best estimate plus market margin • Discounting at market rates • Recognize own credit rating (?)

What is Fair Value? • London Life (LL) – 4th largest Canadian life insurer • Royal Bank of Canada (RBC)– largest Canadian bank • Great West Life (GWL)– 3rd largest Canadian life insurer • RBC agreed to buy LL for CAD$ 2.4 billion • GWL bought LL for CAD$ 2.9 billion

What is Fair Value? • What assumptions should be used in valuation? • The market’s • The company’s • How will we determine market value margins? • How will these compare to margins for adverse deviation?

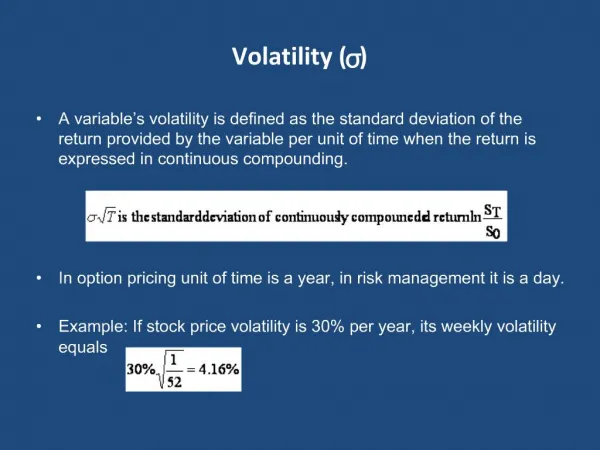

Volatility • Using fair values will introduce considerable volatility in financial reporting • Asset / liability matching (ALM) can reduce volatility if it is recognized in accounting • Canadian Asset Liability Method • BUT accounting theory holds assets and liabilities to be independent • Not necessarily consistent with market behaviour

Volatility • Under current version of IAS 39, volatility would be distorted • Proposed fair value option • Contains an embedded derivative • Financial liability linked to assets valued at fair value • Exposure to changes in fair value is substantially offset by changes in value of another financial asset or liability

Smoothing: response to volatility Consider the following example: • Stochastic valuation of variable annuities with minimum maturity guarantees • Based upon CTE(x) = TVaR (x) = E{X X>x}

Smoothing: response to volatility • Current industry proposal to formally smooth capital requirements • Supporting arguments are based upon imprecision of the calculation • Do not recognize the volatility is a reflection of the market • “If one is comfortable with smoothing capital volatility, then income volatility should be smoothed as well and possibly more so”

Protecting the Integrity of the Financial Reporting System • Auditors • Actuaries • Analysts • Regulators

Discussion www.osfi-bsif.gc.ca