Download

1 / 154

1.54k likes | 1.66k Vues

P a g e | 1 Inter n a tio n a l A s s oci a t ion of R isk a nd Compl i a n c e Pro f e s s io n a ls ( I A RCP) 1200 G St re e t NW Su i te 800 W a s h i ng t o n, D C 200 0 5 - 67 0 5 U SA T e l : 202 - 449 - 9750 w w w .ri s k - co m pl i a nce - a s s o c i a tion . co m.

E N D

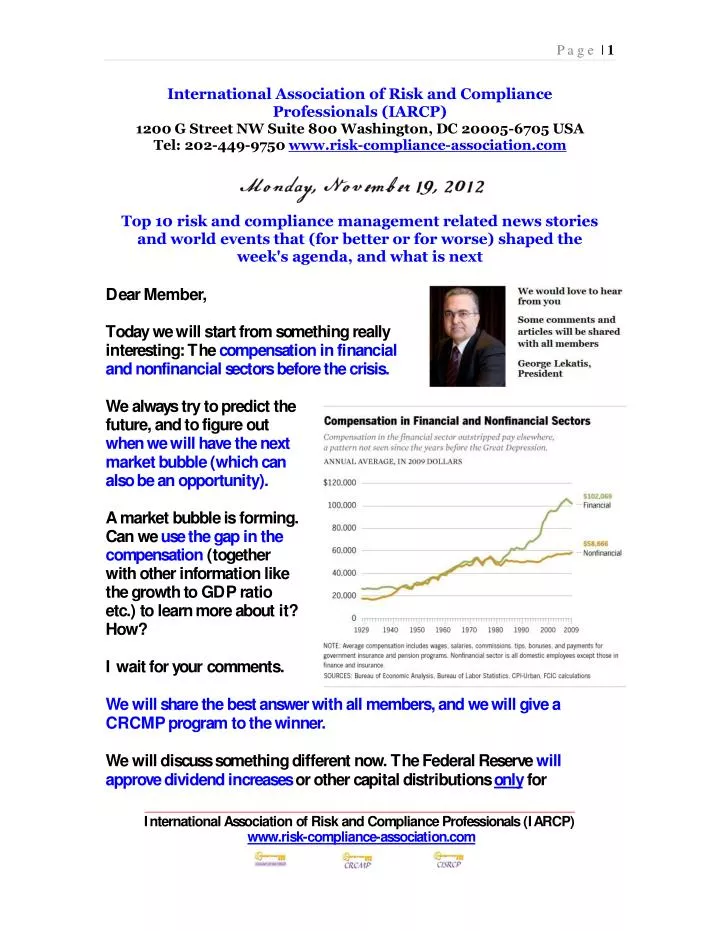

P age |1 InternationalAssociationofRiskandCompliance Professionals(IARCP) 1200GStreetNWSuite800Washington, DC20005-6705USATel:202-449-9750www.risk-compliance-association.com Top10riskandcompliancemanagementrelatednewsstoriesandworldeventsthat(forbetterorforworse)shapedthe week'sagenda,andwhatisnext DearMember, Todaywewillstartfromsomethingreallyinteresting:Thecompensationinfinancialandnonfinancialsectorsbeforethecrisis. Wealwaystrytopredictthefuture,andtofigureoutwhenwewillhavethenextmarketbubble(whichcanalsobeanopportunity). Amarketbubbleisforming.Canweusethegapinthecompensation(togetherwithotherinformationlikethegrowthtoGDPratioetc.)tolearnmoreaboutit?How? Iwaitforyourcomments. Wewillsharethebestanswerwithallmembers,andwewillgiveaCRCMPprogramtothewinner. Wewilldiscusssomethingdifferentnow.TheFederalReservewillapprovedividendincreasesorothercapitaldistributionsonlyfor InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |2 companieswhosecapitalplansareapprovedbysupervisorsandwhoareabletodemonstratesufficientfinancialstrengthtocontinuetooperateasfinancialintermediariesunderstressedmacroeconomicandfinancialmarketscenarios,evenaftermakingtheplannedcapitaldistributions. Thisisveryinteresting. Ononehand,undertheBaseliiirules,banksneedtohavemorecommonequityTier1capital.Sobanksmustattractinvestors. Ontheotherhand,itbecomesmoreandmoredifficulttopaydividends. Isitaflaw,anoxymoron?Whichareyourthoughts? Wewillsharethebestanswerwithallmembers,andwewillgiveaCRCMPprogramtothewinner. YoucanreadmoreaboutthedividendsatNumber1below. Also… “Acyclisthasmadeastrongstarttotherace. But,asithappens,hehasoverestimatedhisstrength. Afterawhile,hehastopedalharderjusttoavoidfallingover. Hisenergiesareflaggingandheisonthepointofcollapsingfromexhaustion. Hismistakewastotreatalong-distanceraceasaseriesofever-shorteningsprints. Hishorizonwastooshort;thecumulativeeffortisfinallycatchingup.Andyet,hestruggleson. Theglobaleconomyisnotsodifferentfromthissportsman. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |3 Itgainednewforcefromapowerfulwaveofglobalisationandthe suppressionofinflation. Buttheresurgenceofthefinancialcyclemadeitfeel,forawhile,stronger thanitreallywas. Marketparticipantsandpolicymakersdidnotseethroughthisillusion. And,everytimethatafinancialboomturnedtobust,theywouldsimplytryharder,re-applyingthesameoldnostrums. Theirhorizonsweretooshort;andthecumulativeimpactoftheireffortsiscatchingupwiththem:stocksofprivateandsovereigndebthavebeengrowingbeyondsustainablelevelsandthepolicyroomformanoeuvrehasbeenshrinkingdramatically” Whosaidthat? ClaudioBorio,fromtheBankforInternationalSettlements,inonereallygreatpresentation… …wherehecoverseconomiccyclesaswell! Hecontinues-atNumber3ofourlist:“Ourhistorianwouldgooneleveldeeper. Hewouldask:“Arebankingcrises,likeTolstoy’sfamousunhappyfamilies,alldifferent?Oraretheymorelikehishappyones,whichareallalike?” Youmustreadit!!! WelcometotheTop10list. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |4 AgenciesProvideGuidanceonRegulatoryCapital Rulemakings TheU.S.federalbankingagenciesissuedthreenoticesofproposedrulemakinginJunethatwouldreviseandreplacethecurrentregulatory capitalrules. TheproposalssuggestedaneffectivedateofJanuary1,2013. AfullversionoftheGroupof20communique: “We,theG20FinanceMinistersandCentralBankGovernors,mettoassessprogressonthefulfillmentofthemandatesgiventousbyour Leaders,topromoterobustgrowthandjob creationandtoaddressongoingeconomicand financialchallenges.” Ontime,stocksandflows:Understandingtheglobalmacroeconomicchallenges ClaudioBorio BankforInternationalSettlements InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |5 PCAOBRegulatoryInitiatives JamesR.Doty,Chairman PractisingLawInstitute,NewYork,NY Introductorystatement MarioDraghi,PresidentoftheECB, VítorConstâncio,Vice-PresidentoftheECB, FrankfurtamMain StevenMaijoor,ESMAChairDevelopmentsinEuropeanFinancialReportingRegulationandEnforcement MeettheExperts,London SpeechbytheChancelloroftheExchequer,RtHonGeorgeOsborneMP (totheRoyalSociety) InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |6 TheChallengesofUnderstandingLaborMarketTrends DennisLockhart,PresidentandChiefExecutiveOfficer FederalReserveBankofAtlanta LargeExposureRegime GroupsofConnectedClientsandConnectedCounterparties Interestingparts AIMAANNOUNCESAIFMD IMPLEMENTATIONPROJECT TheAlternativeInvestmentManagementAssociation(AIMA),theglobalhedgefund association,hasannounceditsAIFMDImplementationProjectaheadofthereleaseofthefinalimplementationtextoftheAlternativeInvestment FundManagersDirective(AIFMD)bytheEuropeanCommission. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |7 AgenciesProvideGuidanceon RegulatoryCapitalRulemakings TheU.S.federalbankingagenciesissuedthreenoticesofproposedrulemakinginJunethatwouldreviseandreplacethecurrentregulatory capitalrules. TheproposalssuggestedaneffectivedateofJanuary1,2013. ManyindustryparticipantshaveexpressedconcernthattheymaybesubjecttoafinalregulatorycapitalruleonJanuary1,2013,withoutsufficienttimetounderstandtheruleortomakenecessarysystems changes. Inlightofthevolumeofcommentsreceivedandthewiderangeofviewsexpressedduringthecommentperiod,theagenciesdonotexpectthatanyoftheproposedruleswouldbecomeeffectiveonJanuary1,2013. AsmembersoftheBaselCommitteeonBankingSupervision,theU.S.agenciestakeseriouslyourinternationallyagreedtimingcommitmentsregardingtheimplementationofBaselIIIandareworkingasexpeditiouslyaspossibletocompletetherulemakingprocess. Aswithanyrule,theagencieswilltakeoperationalandother considerationsintoaccountwhendeterminingappropriateimplementationdatesandassociatedtransitionperiods. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |8 TheFederalReserveBoardonFridaylaunchedthe2013capitalplanning andstresstestingprogram,issuinginstructionstofirmswithtimelinesforsubmissionsandgeneralguidelines. TheprogramincludestheComprehensiveCapitalAnalysisandReview(CCAR)of19firmsaswellastheCapitalPlanReview(CapPR)ofan additional11bankholdingcompanieswith$50billionormoreoftotalconsolidatedassets. Theaimoftheannualreviewsistoensurethatlarge,complexbankinginstitutionshaverobust,forward-lookingcapitalplanningprocessesthataccountfortheiruniquerisks,andtohelpensurethatinstitutionshavesufficientcapitaltocontinueoperationsthroughouttimesofeconomicandfinancialstress. Capitalisimportanttobankingorganizations,thefinancialsystem,andthebroadeconomybecauseitactsasacushiontoabsorblossesandhelpstoensurethatanysuchlossesarebornebyshareholders,nottaxpayers. InstitutionsintheCCARandCapPRprogramswillbeexpectedtohavecredibleplansthatshowtheyhavesufficientcapitaltocontinuetolendtohouseholdsandbusinessesevenunderseverelyadverseconditions,andarewellpreparedtomeetBaselIIIregulatorycapitalstandardsastheyareimplementedintheUnitedStates. Firms'capitaladequacywillbeassessedagainstanumberofquantitativeandqualitativecriteria,includingprojectedperformanceunderthestressscenariosprovidedbytheFederalReserveandtheinstitutions'internalscenarios. BoardsofdirectorsoftheinstitutionsarerequiredtoreviewandapprovecapitalplansbeforesubmittingthemtotheFederalReserve. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |9 "TheFederalReservehasbeenfocused--andwillremainfocused--onensuringthenation'slargestfinancialinstitutionshaveenoughcapitalto weathersevere,unexpectedconditionsandstillcontinuelendingtohouseholdsandbusinesses,"Gov.DanielK.Tarullosaid. The19bankholdingcompaniesintheCCARhaveincreasedtheiraggregatetier1commoncapitalto$803billioninthesecondquarterof2012from$420billioninthefirstquarterof2009. Thetier1commonratioforthesefirms,whichcompareshigh-qualitycapitaltorisk-weightedassets,hasmorethandoubledtoaweightedaverageof10.9percentfrom5.4percent. OnepartoftheCCARandCapPRreviewsisanevaluationbytheFederalReserveofinstitutions'planstomakecapitaldistributions,suchasdividendpaymentsorstockrepurchases. TheFederalReservewillapprovedividendincreasesorothercapitaldistributionsonlyforcompanieswhosecapitalplansareapprovedbysupervisorsandwhoareabletodemonstratesufficientfinancialstrengthtocontinuetooperateasfinancialintermediariesunderstressedmacroeconomicandfinancialmarketscenarios,evenaftermakingtheplannedcapitaldistributions. Inachangefromprioryears,followingtheFederalReserve'sassessmentoftheinitialcapitalplans,CCARfirmswillhaveoneopportunitytomakeadownwardadjustmenttotheirplannedcapitaldistributionsfromtheirinitialsubmissionsbeforeafinalFederalReservedecisionismade. Asin2012,theFederalReservewillreleasesummaryresultsforthe19CCARfirmsincludingitsprojectionsofcapitalratios,losses,andrevenuesundertheFederalReserve'sseverelyadversescenario. In2013,theFederalReservewillreleasetwosetsofpost-stressdatafor eachfirm. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |10 OnesetwillreflectthecapitaldistributionassumptionsprescribedinthestresstestingrulemandatedbytheDodd-FrankWallStreetReformandConsumerProtectionActtoenhancecomparabilityofresults. Theotherwillincluderatiosbasedoneachfirm'sownplannedcapitalactionsasproposedintheirinitialCCARcapitalplansubmissions,aswellasratiosbasedonanyadjustmentsmadetoplannedcapitaldistributions. WhiletheaimsofCapPRarethesameasCCAR,thereareanumberofimportantdistinctions. Forexample,theFederalReserve'sassessmentofcapitalplansunderCapPRwillnotbebasedonsupervisoryestimatesderivedfromindependentsupervisorymodels,butinsteadsolelyonanassessmentofthefirms'owncapitalplansandinternalcapitalplanningandstresstestingpracticesthatsupportthem. Further,theFederalReservewillnotpublishasummaryofbank-specificresultsforCapPRin2013. TheFederalReservewantedtogivefirmsasmuchtimeaspossibletopreparetheirsubmissionsandthereforeisissuingtheinstructionsahead ofthereleaseofthemacroeconomicandfinancialmarketscenarios. TheFederalReservewillrequireinstitutionstousethescenariosinboththestresstestsconductedaspartoftheircapitalplansandinthestressteststhatarepartoftheDodd-FrankWallStreetReformandConsumerProtectionAct. TheFederalReserveexpectstoreleasethescenariosat4p.m.ESTonThursday,November15.InstitutionswillberequiredtosubmittheircapitalplansnolaterthanJanuary7,2013. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |11 ThefollowingisafullversionoftheGroupof20communique: We,theG20FinanceMinistersandCentralBankGovernors,mettoassessprogressonthefulfillmentofthemandatesgiventousbyour Leaders,topromoterobustgrowthandjob creationandtoaddressongoingeconomicandfinancialchallenges. Wewilldoeverythingnecessarytostrengthentheoverallhealthandgrowthoftheglobaleconomy. Ourmainfocusintheperiodaheadwillbetorebuildconfidenceandtoreducerisksandvolatilityininternationalfinancialmarkets;contributetoafasterpaceofeconomicrecoveryandjobcreation,andpromotethefoundationsforstrong,sustainable,andbalancedgrowth. Wearefirmlycommittedtoopentradeandinvestment,expandingmarketsandresistingprotectionisminallitsforms. WehavemadesignificantprogressinimplementingthecommitmentsestablishedintheLosCabosGrowthandJobsActionPlan. SubstantivemeasureshavebeenadoptedinEurope,includingthelaunchoftheEuropeanStabilityMechanism,thedecisionoftheECBonOutrightMonetaryTransactions,theagreementbyEuropeanleaderstoestablishasinglesupervisorymechanismforbanks,theadoptionandongoingimplementationoftheCompactforGrowthandJobs,andthereformsandfiscalconsolidationcarriedoutbyanumberofEuropeancountries. Othercountrieswithpolicyspacehaveimplementedactionstosupportaggregatedemand. Majorcentralbankshavetakenfurtherunconventionalmeasuresinlinewiththeirrespectivemandateswhicharewelcomed. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |12 Globalgrowthremainsmodestanddownsiderisksarestillelevated,includingduetopossibledelaysinthecompleximplementationofrecentpolicyannouncementsinEurope,apotentialsharpfiscaltighteningin theUnitedStates,securingfundingforthisyear'sbudgetinJapan,weakergrowthinsomeemergingmarketsandadditionalsupplyshocksinsomecommoditymarkets. Thereductionofglobalimbalanceshasnotbeensufficient,andinmanycountriestheprocessofnecessarydeleveragingbytheprivateandpublicsectorsisongoingandunemploymentremainshigh. Completeandtimelyimplementationofallofourpolicycommitmentsiscriticalinordertocontinuetoreducerisksandsecureadurableandstrongrecovery. Wearecommittedtobuildonthepolicymeasurestakeninrecentmonths. CurrentreformmomentumintheEUonstructural,fiscalandfinancialfieldsneedstobecontinuedwiththeviewtoimprovingcompetitivenessandpromotingfinancialstability. Inthisrespect,wewelcometherecentdecisionbyEuropeanleaderstoagreeonalegislativeframeworkbyJanuary1st2013onasinglesupervisorymechanism. Welookforwardtotheoperationalimplementationofthesinglesupervisorymechanisminthecourseof2013andtothecompletionofthetechnicaldiscussionsonthefutureoftheESMdirectbankrecapitalizationinstrument,withinabroaderstrategyofcompletingthearchitectureoftheEMU. Wewillensureourpublicfinancesareonsustainablepaths,inlinewiththemedium-termTorontocommitmentsinthecaseofadvancedeconomies. Inlightoftheweakpaceofglobalgrowth,theywillensurethatthepaceoffiscalconsolidationisappropriatetosupporttherecovery. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |13 Countrieswhichhavefiscalspacewilllettheautomaticfiscalstabilizersoperateasappropriate. Thosewithsufficientspacestandreadytosupportdemandasneededin theshortrunshouldeconomicconditionsdeteriorate. TheUnitedStateswillcarefullycalibratethepaceoffiscaltighteningtoensurethatpublicfinancesareplacedonasustainablelong-runpathwhileavoidingasharpfiscalcontractionin2013. InJapanfurtherprogressinmedium-termfiscalconsolidationisneeded. BythenextSummit,advancedeconomiesagreetoidentifycredibleandambitiouscountry-specifictargetsforthedebt-to-GDPratiobeyond2016,wherethesedonotcurrentlyexist,accompaniedbyclearstrategiesandtimetablestoachievethem. 7.Theweakpaceofglobalgrowthalsoreflectslimitedprogresstowardssustainingandrebalancingglobaldemand. Wecommittoachievingexternalandinternaladjustmentinawaythatsupportsandsustainsgrowthandleadstoglobalrebalancing. Inthisregard,wereiterateourcommitmentstomovemorerapidlytowardmoremarket-determinedexchangeratesystemsandexchangerateflexibilitytoreflectunderlyingfundamentals,avoidpersistentexchangeratemisalignmentsandrefrainfromcompetitivedevaluationof currencies;toboostdomesticsourcesofgrowthinsurpluseconomies,andboostnationalsavingsindeficiteconomies. Wereiteratethatexcessvolatilityoffinancialflowsanddisorderlymovementsinexchangerateshaveadverseimplicationsforeconomicandfinancialstability. Wecommittotheimplementationofambitiousstructuralreformsaimedatpromotingoutputandemployment. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |14 WehavealsomadeprogressinstrengtheningourAccountabilityAssessmentframeworkbyagreeingonasetofmeasurestoinformour analysisofourfiscal,monetaryandexchangeratepolicies. Wewillconsiderarangeofindicatorsandapproachestoassessspillovereffects,progresstowardscommitmentsonstructuralreforms,andourcollectiveachievementofstrong,sustainableandbalancedgrowth. WewelcomethecontinuationoftheprocesstostrengthenIMFresourcestosafeguardglobalfinancialstabilityandenhancetheIMF'sroleincrisispreventionandresolution. SincetheLosCabosSummit,additionalpledgeshavebeenreceivedfrommoremembers,andtotalcommitmentsadduptoUS$461billion. Furthermore,wewelcometheformalizationofthefirstsetofbilateralborrowingagreementsundertheagreedmodalitiescomprisingUS$286bn,whichrepresentmorethanhalfoftheLosCabos'2012pledge. Wecallforthefinalizationoftheremainingbilateralagreements. WewelcomeIMF´sExecutiveBoarddecisionontheuseofUS$2.7bnofadditionalresourcesfromthewindfallgoldsalesprofitsfortheFund´sPovertyReductionandGrowthTrustandcallonthemembershiptoprovidetheassurancesneededforthistotakeplace. Thiseffortreinforcestheinternationalcommunity´swilltoreducepovertybyboostingfinancialassistancetolowincomecountrymembers. Weremaincommittedtothefullimplementationofthe2010QuotaandGovernanceReform. Althoughsignificantprogresshasbeenachieved,asofOctober2012theconditionsfortheentryintoforceofthe2010QuotaandGovernanceReformhavenotbeenfullymet. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |15 Wereaffirmtheurgencyofmakingtheseimportantreformseffectiveandcallonmemberswhohaveyettocompletetheprocesstodosoassoonaspossible. TheprocessofIMFreformwillenhanceitslegitimacy,relevanceandeffectiveness. Wearecommittedtocompletingthecomprehensivereviewofthequotaformula,toaddressdeficienciesandweaknessesinthecurrentquotaformula,byJanuary2013andtocompletethenextgeneralreviewofquotasbyJanuary2014. Weagreethattheformulashouldbesimpleandtransparent,consistentwiththemultiplerolesofquotas,resultincalculatedsharesthatarebroadlyacceptabletothemembership,andbefeasibletoimplementbasedonatimely,highqualityandwidelyavailabledata. Wereaffirmthatthedistributionofquotasbasedontheformulashould betterreflecttherelativeweightsofIMFmembersintheworldeconomy,whichhavechangedsubstantiallyintheviewofastrongGDPgrowthin dynamicemergingmarketsanddevelopingcountries. WereaffirmtheimportanceofcontinuingtoprotectthevoiceandrepresentationofthepoorestmembersoftheIMF. WecallontheIMFmembershiptodeveloptheconsensusneededtocompletethereviewbyJanuary2013. WewelcomethestrengtheningoftheIMF'ssurveillanceframeworkthroughtheadoptionofthenewIntegratedSurveillanceDecision,andwewelcometheintroductionofthePilotExternalSectorReporttostrengthenmultilateralanalysisandenhancethetransparencyofsurveillance. AtransparentandevenhandedframeworkofsurveillanceiskeytoachieveownershipandtractionofpolicyrecommendationsbytheIMF,thusmakingsurveillancemoreeffective. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |16 WenotetheWorldBankandotherInternationalOrganizations'(IOs)progressreportonimplementationoftheG20actionplantosupportthedevelopmentoflocalcurrencybondmarkets. Welookforwardtofullimplementationoftheactionplanin2013toensureabroadownershipofthediagnostictoolamongpotentialusers,andfurtherreportingonprogressbytheWorldBank. Wewelcomeongoingregionalinitiativestopromotelocalcurrencybondmarkets. WewilldeepenworkontheseissuesunderRussia´sPresidency. Weacknowledgetheimportanceoflongtermfinancing,particularlyforinfrastructureinvestment,recognizingthatworkonthissubjectwillfosteranenvironmentmoreconducivetolong-terminvestment,effectivelyhelpingtoboostjobsandgrowth. WeaskthattheWorldBank,IMF,OECD,FSB,UNandrelevantIOsundertakefurtherdiagnosticworktoassessfactorsaffectinglong-terminvestmentfinancingincludingitsavailability. Welookforwardtoreceivingthisworkinearly2013toprovideasoundbasisforanyfutureG20work. Weremaincommittedtothefull,timelyandconsistentimplementationofthefinancialregulationagenda,anddiscussedthelatestFSBreportsontheprogressinimplementationofagreedreforms. WeendorsetheconclusionsandrecommendationsofthefourthprogressreportontheimplementationoftheG20commitmentstoOTCderivativesreformsandtheBCBSreportonimplementationofBaselIII. WeagreetoputinplacethelegislationandregulationforOTCderivativesreformspromptlyandactbyend-2012toidentifyandaddressconflicts,inconsistenciesandgapsinourrespectivenationalframeworks,includinginthecross-borderapplicationofrules. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |17 Weagreetotakethemeasuresneededtoensurefull,timelyandeffectiveimplementationofBaselII,2.5andIIIanditsconsistencywiththeinternationallyagreedstandards. WelookforwardtoreceivingforourAprilmeetingtheBCBSreportontheconsistencyofmeasurementofrisk-weightedassets. WeendorsetheCharterfortheRegulatoryOversightCommitteewhichwillactasthegovernancebodyfortheglobalLegalEntityIdentifiersystemtobelaunchedinMarch2013. Weacknowledgeprogressmadeinthedesignandimplementationofpolicymeasurestostrengthentheresilienceofthefinancialsystemandreducesystemicrisks. Inparticular,wewelcomethepublicationbytheFSBofanupdatedlistofglobalsystemicallyimportantbanks,theBCBSframeworkfordealingwithdomesticsystemicallyimportantbanks,andtheInternationalAssociationofInsuranceSupervisors(IAIS)consultationpaperonpolicymeasuresforglobalsystemicallyimportantinsurancecompanies. WecommittomakethenecessarychangestoresolutionregimestoenableauthoritiestoresolveSIFIs. Wewelcometheinitialintegratedsetofpolicyrecommendationstostrengthentheoversightandregulationofshadowbankingtogetherwithexpandeddatamonitoring. WecallforfinalizedpolicymeasuresbytheSt.PetersburgSummitforoversightandregulationforshadowbankingthatcanbepeer-reviewed. WealsowelcometherecommendationstoincreasetheintensityandeffectivenessofSIFIsupervision,andtheFSB'sroadmaptoaccelerateimplementationoftheFSBPrinciplesforReducingRelianceonCreditRatingAgencyRatings. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |18 Weencouragefurtherworktoenhancetransparencyofandcompetition amongcreditratingagenciesandaskIOSCOtoprovideareportonongoingworkatourmeetinginApril. WesupportmeasurestostrengthenthetransparencyoffinancialinstitutionsandrecognizethecontributionoftheEnhancedDisclosureTaskForce. Recognizingtheneedforadequatestatisticalresources,weendorsetheprogressreportoftheFSBandtheIMFonclosinginformationgaps,andinparticularlookforwardtotheimplementationofthedatareportingtemplatesforglobalsystemicallyimportantfinancialinstitutions. Weareconcernedabouttheslowprogressachievedtowardasinglesetofhighqualityaccountingstandards. WeencouragetheInternationalAccountingStandardsBoard(IASB)andFinancialAccountingStandardsBoard(FASB)tocompletework promptly,andreporttoournextmeeting. InrelationtoLIBOR,EURIBORandotherfinancialbenchmarks,wewelcomeactionstakenandongoingreviewstoidentifymeasurestoaddressweaknessesandrestoreconfidenceinbenchmarkandindexsettingpracticesandwelcomethecoordinatorroleoftheFSBasagreed. WeaskIOSCOtoprovidebyourAprilmeetingareportonthenextstepsonthefunctioningofcreditdefaultswapsmarkets. WeexpecttheFSBtocontinuemonitoring,analyzingandreportingontheunintendedconsequencesofregulatoryreformsonEMDEs. 18.WewelcometheFSB'sprogressinimplementingthemeasuresendorsedatLosCabostostrengthenitscapacity,resourcesandgovernance. Welookforwardtoitsestablishmentasalegalentitybyournextmeeting anditsfullimplementationbySeptember2013. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |19 WecallontheFSBtoreportbackonhowitintendstokeepunderreviewthestructureofitsrepresentation. Wewelcometheobservedincreaseinjurisdictions'adherencetointernationalregulatoryandsupervisorycooperationandinformationexchangestandards,asstatedintheFSBstatusreport,andcallforfurtherprogress. WeremaincommittedandencouragetheFATFtocontinuetopursueallitsobjectives,andnotablytocontinuetoidentifyandmonitor high-riskjurisdictionswithstrategicAnti-MoneyLaundering /Counter-TerroristFinancing(AML/CFT)deficiencies. Welookforwardtothecompletionin2013oftherevisionoftheFATFassessmentprocess. WeencourageallcountriestoadapttheirlegalframeworkwithaviewtocomplyingwiththerevisedFATF'sRecommendations,inparticularthenecessitytoidentifythebeneficialownerofcorporatevehicles,andwelookforwardtotheassessmentoftheeffectivenessofthemeasurescountriestakeandtheircompliancewiththeglobalstandardsinthenextroundofMutualEvaluations. WecommendthesigningsoftheMultilateralConventioninCapeTownandfurtherprogressmadetowardstransparencyasreportedbytheGlobalForumwhosemembershiphasincreased. WelookforwardtoaprogressreportbytheGlobalForumontheeffectivenessofinformationexchangepracticesbyApril2013. WewelcomeandendorsetheimprovedOECDstandardwithrespecttoinformationrequestsonagroupoftaxpayersandencourageallcountriestoadoptitwhenappropriate. WewillcontinuetoimplementpracticesofautomaticexchangeofinformationandcallontheOECDtoanalyzethesafeguards,mechanismsandmilestonesnecessarytoincreaseitsuseandefficientimplementationinamultilateralcontext. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |20 WealsowelcometheworkthattheOECDisundertakingintotheproblemofbaseerosionandprofitshiftingandlookforwardtoareportaboutprogressoftheworkatournextmeeting. Wewelcometheworkstatedinthefinal2012GlobalPartnershipforFinancialInclusion(GPFI)progressreportonimplementingthefiverecommendationssetoutin2011andtheprogressonimplementingtheG20PrinciplesforInnovativeFinancialInclusion,includingthroughconcreteactionsbydevelopingandemergingcountriestomeettheir commitmentstotheMayaDeclaration. WecommendtheadditionalcommitmentstotheMayaDeclarationmadeinCapeTownin2012,andencouragecountriestomeasureprogressthroughnationaldatacollectionefforts. WewelcomethedecisiontoestablishtheAllianceforFinancialInclusion(AFI)asapermanentnetworkforknowledgecreation,exchangeandpolicydialogue. WewelcomethefirstGPFIConferenceonStandard-SettingBodiesandFinancialInclusionasasubstantialdemonstrationofgrowingcommitmentamongStandardSettingBodies(SSBs)toprovideguidanceandtoengagewiththeGPFItoexplorethelinkagesamongfinancialinclusion,financialstability,financialintegrityandfinancialconsumerprotection. WealsocommendtheworkdonetocontinueimprovingSMEsfinancing andtheirenvironment. Togetherwiththeimplementingpartners,welookforwardtoupdatesontheG20FinancialInclusionPeerLearningProgramandencouragethecommitmenttootherinitiativesthatpromoteFinancialInclusion. Foradvancingthefinancialconsumerprotectionagenda,weacknowledgetheworkdonebytheInternationalFinancialConsumerProtectionNetwork(FinCoNet)tosupporttheexchangeofbestpracticesandlookforwardforaprogressreportbytheG20SummitinSt.Petersburgin2013. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |21 WealsowelcometheimplementationoftheactionplanbytheG20OECDTaskForceonFinancialConsumerProtectionandprogressachievedinCartagena,includinginthefieldofnationalstrategiesand financialeducationforwomen,bytheOECDInternationalNetworkonFinancialEducation(INFE). Wewelcomethenumberofproposalsreceivedinresponsetothe2012MexicoFinancialInclusionChallenge:InnovativeSolutionsforUnlockingAccess. Wecongratulatethefinalistsandthewinner. InLosCabos,Leadersrecognizedthatexcessivecommoditypricevolatilityhassignificantimplicationsforcountries,increasinguncertaintyintheeconomy,andendorsedtheconclusionsofareportonthemacroeconomicimpactsofexcessivecommoditypricevolatilityongrowth. Aheadofthe2013Summit,wewillreportprogressontheG20'scontributiontofacilitatebetterfunctioningofcommoditymarkets,consideringpossibleareasforfurtherworkoutlinedinthereport. Wereaffirmourcommitmenttoimprovetransparencyand functioningofcommoditymarkets. WewelcometheprogressmadeintheimplementationoftheAgriculturalMarketInformationSystem(AMIS)whichwillprovidemoretransparencyonphysicalmarketsforagriculturalcommodities. WewelcometheIEF'srecommendationstoimprovethereliabilityoftheJODI-Oildatabase. WewelcomethereportpreparedbytheIEA,theIEFandtheOPEConincreasingtransparencyininternationalgasandcoalmarketsandasktheseorganizationstoproposepracticalstepsbymid-2013thatG20countriescouldtaketoimplementthem. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |22 WewelcomeprogressontheJODI-Gasdatabaseandlookforwardtoworkingwithitin2013. Wewelcomethereportonrecommendationstoimprovethefunctioning andoversightofoilPriceReportingAgencies,andaskIOSCOtoliaisewiththeIEA,IEFandOPECtoassesstheimpactoftheprincipleson physicalmarketsandreportback. WealsoaskIOSCOtoreportprogressontheimplementationoftheprinciplesin2013. Wereaffirmourcommitmenttoenhancetransparencyandappropriateregulationinfinancialcommoditymarkets,andthuswewelcomeIOSCO'sreportontheimplementationofitsPrinciplesfortheRegulationandSupervisionofCommoditiesDerivativesMarkets. InLosCabos,Leadershighlightedthatgreengrowthandsustainabledevelopmentpolicieshavestrongpotentialtostimulatelongterm prosperity. Wewillvoluntarilyself-reportagainin2013onoureffortstoincorporategreengrowthandsustainabledevelopmentpoliciesintostructuralreformagendas,takingintoaccounttheoutcomeoftheUNConferenceonSustainableDevelopment(Rio+20). Wewillreportbacktoourleadersontheprogressmadetorationalizeand phase-outoverthemedium-terminefficientfossilfuelsubsidiesthatencouragewastefulconsumption,whileprovidingtargetedsupportforthepoorest. WewilldevelopavoluntarypeerreviewprocessonsuchfossilfuelsubsidiesandpresentareportontheoutcomestoourLeadersin2013. WewelcometheOECDreportonpensionfundsfinancinggreeninitiatives. RecognizingthattheUNFCCCistheforumforclimatechangenegotiationsanddecisionmakingattheinternationallevel,we InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |23 acknowledgethatclimatefinanceisarelevantissuetobediscussedamongstG20FinanceMinistersandCentralBankGovernors. WewelcometheprogressreportbytheG20ClimateFinanceStudyGrouponwaystoeffectivelymobilizeresourcesforclimatefinance. WewillcontinueworkingtowardsbuildingabetterunderstandingoftheunderlyingissuesamongG20memberstakingintoaccounttheobjectives,provisionsandprinciplesoftheUNFCCC,andreportbacktoourLeadersin2013. WerecognizethatdisasterriskfinancingpoliciesarenecessaryforanoverallDisasterRiskManagement(DRM)strategy. WeappreciateandwelcomethecombinedeffortsmadebytheWorldBankandtheOECD,withthesupportoftheUnitedNations,tobroadentheparticipationinthediscussiononDRMbyhighlightingthecentral rolethatfinancialpolicymakersplaytosupportotherareasofGovernmentandcivilsocietyindealingwithdisasters. WewelcometheG20/OECDvoluntaryframeworkfordisasterriskassessmentandriskfinancingwhichprovidesadetailedguidelinethataimstofacilitatetheimplementationofmoreeffectiveDRMstrategies. WeencouragefurthereffortsbytheWorldBankandOECDincooperationwithotherrelevantinternationalorganizationstoleveragethevoluntaryframeworkinordertoaddressremainingchallenges. WecommendMexicoforchairingtheG20in2012andlookforwardtoRussia'spresidencyin2013. TheFinanceTrack TheFinanceTrackintheG20focusesonfinancialandeconomicissues;theseincludeprovidingsolutionstothecurrenteconomicproblems,economicstabilizationandstructuralreforms,increasinginternationalcoordinationforcrisisprevention,correctionofexternal,fiscaland InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |24 • financialimbalances,providingresourcestoincreasegloballiquidity,andstrengtheningtheinternationalfinancialsystem. • TheFinanceTrackiscomposedofallG20FinanceMinistersandCentralbankGovernorswhomeetregularlyduringtheyeartodiscussthecurrenteconomicglobalproblemsandtakecoordinatedactionstowardstheirsolutions;thesemeetingsareattendedalsobyInternationalOrganizationssuchastheIMF,WorldBank,OECDortheFinancialStabilityBoard. • Organizationally,thetrackoperateswithworkinggroupsformallyestablishedwithintheG20butalsothroughclosecooperationwithinternationalfinancialentities. • CurrentlytheFinanceTrackoftheG20isorganizedinthefollowingmajorareas: • FrameworkforStrong,SustainableandBalancedGrowthWorkingGroup(Co-chairedbyCanadaandIndia) • FinancialRegulation • FinancialInclusion,FinancialEducationandConsumerProtection • InternationalFinancialArchitectureWorkingGroup(Co-chairedbyAustraliaandTurkey) • EnergyandCommoditiesMarketsWorkingGroup(Co-chairedbyIndonesiaandUnitedKingdom) • CommoditiesMarketsSubgroup(Co-chairedbyBrazilandUnitedKingdom) • EnergyandGrowthSubgroup(Co-chairedbyKoreaandUnitedStates) • DisasterRiskManagement • ClimateFinanceStudyGroup(Co-chairedbyFranceandSouthAfrica) • TheG20hasbeenaveryeffectiveforumofinternationalcoordinationandcooperationforcrisismitigationandtofostereconomicgrowthandstrengthenfinancialregulation. • Ithasalsoincreaseditsscopetootherrelevanteconomicissuessuchasfinancialinclusionandeducation,disasterriskmanagement,greengrowthorclimatefinance. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |25 UndertheMexicanpresidency,theFinancetracklaunchedthe2012G20AgendaonDecember13-14th2011withaseminarinMexicoCity. InpreparationtotheLeadersSummitinLosCabosinJune,FinanceMinistersandCentralBankGovernorshavemetonFebruaryandApriltodiscusscurrentrelevanteconomicproblemsandhavetakencoordinated actionsfortheirsolution. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |26 Ontime,stocksandflows:Understandingtheglobal macroeconomicchallenges ClaudioBorio BankforInternationalSettlements Introduction Itwasn’tmeanttobelikethis. Thefinancialcrisisthatbeganin2007 shatteredtheillusionofuninterruptedprosperitythathadprevailedinmuchoftheWesternworld. Itwasnotthefirsttimethatthishadhappened. Doubtless,itwillnotbethelast. Fiveyearson,muchoftheadvancedcountryworldisstillstrugglingtoreturntorobust,sustainablegrowth. Andthecrisishaskeptmorphingbeforeoureyes;ithasnowengulfedsovereignstoo. Theeuroareaisthenewepicentre. Butwillthetremorsstopthere? Inwhatfollows,Iwillseektoprovideabroadframeworkforthinkingtheseissuesthrough. Howdidwegethere?Why?Wheremightwegofromhere?Howmightweextricateourselvesfromourpredicament? InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |27 Thesearehardquestions. Noonereallyknowstheanswers. Butallofushaveaperspectiveandanarrativethatgoeswithit. Thisisjustanotherone–onethatdrawsheavilyonworkdoneattheBIS.Iwilltrytolookbelowthebusyandattimeschaoticsurfaceoftheworld economy. Theideaistoidentifywhatonemightcalltheshiftsinits“tectonic plates”–thosedeepforcesthat,slowlybutcumulatively,can fundamentallyreshapewhatweseeonthesurfaceandthateconomistscall“economicregimes”. Iwillhighlightthreesuchforces:financialliberalisation,theestablishmentofcredibleanti-inflationmonetaryframeworks,andtheglobalisationoftherealsideoftheworldeconomy. Eachofthem,takeninisolation,isundoubtedlyagoodthing.Allofthemtogetherareworthhavingandfightingfor. YetIwillarguethatafailureofpolicytoadjusttothemhasplayedanimportantroleinthecrisisanditsaftermath. Ithasgivenrisetothere-emergenceofpowerfulfinancialcycles,whoseboomsandbustshavecausedhavocintheeconomyandhaveleftuswherewearetoday. Butwhatisthelinkbetweenallthisandthetitleofmyremarks?Infact,thetitlehighlightstwokeyaspectsofthestory. First,time. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |28 Asthethreedeepforcesgainedfullstrengthfromthemid-1980s,theyshapedanenvironmentwhere,inBurnsandMitchell’sterminology,economictimehassloweddownrelativetocalendartime. Thatis,themacroeconomicdevelopmentsthatmattertakemuchlongertounfold. Thelengthofthefinancialcycleismuchlongerthatofthetraditionalbusinesscycle,oftheorderof16to20yearsormorecomparedwithuptoeightyears. Yettheplanninghorizonsofmarketparticipantsandpolicymakershavenotadjustedaccordingly–indeed,ifanything,theyhaveshrunk. Thisisacriticalreasonwhythecurrentproblemshavearisenandwhyithasprovedsohardtosolvethem. Andithasmajorimplicationsforthesustainabilityofgrowth,forfinancialregulation,forfiscalpolicyandformonetarypolicy. Wethencometostocksandflows. Inthenewenvironment,stockshavecometodominateeconomicdynamics,inparticularthelargestocksofassetsand,aboveall,debt. Stocksbuildupabovetrendduringfinancialbooms,ascreditandassetpricesgrowbeyondsustainablelevels,andgeneratestubbornoverhangsoncetheboomturnstobust.Stocksraiseseriouspolicychallenges. Inthepresenceofpolicyresponsesthatreacttoolittletoboomsandtoomuchtobusts–injargon,thatareasymmetric–stocksgrowoverconsecutivebusinesscycles. Ittakeslongertodealwiththem. Anddoingsoisalsopoliticallymoredifficult,becauseoftheseriousimpactonincomeandwealthdistribution,bothwithinandacrossgenerations. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |29 Thisistrueofbothprivateandpublicdebt. Failuretodealwithstockseffectivelycouldentrenchinstabilityinthesystem. Ifthisdiagnosisisright,theremedyisnothardtofind,althoughitmaybeextraordinarilydifficulttoimplement. Inanutshell,itistolengthenpolicyhorizons,toputinplacemoresymmetricalpolicies,andtotacklethedebtproblemshead-on. Muchofmydiscussionwillseektomaketheseguidelinesmoreconcrete. Theultimateriskofafailuretoadjustisthatofyetanother epoch-definingshiftinthetectonicplates–theriskofareversalthatwilltakeusbacktoaneraoffinancialandtradeprotectionismaswellasinflation. Thestructureofmyremarksisasfollows. Thefirstsectionlaysoutthebroadcanvas. Itconsidersthechangingcharacterofeconomicfluctuations,highlightingtheroleofthefinancialcycleanditslinktostructuralinstitutionalarrangements,policydecisionsandhorizons. Thesecondsectionturnstothepolicychallenges. Itbeginswithabriefsummaryofthecurrentsituation,seenthroughthelensofthefinancialcycle. Itthenexplores,inturn,theimmediateormoreconjuncturalchallengeofhowtoreturntoself-sustainingandsustainablegrowthandthenthelonger-termormorestructuralchallengeofhowtoadjustpolicyframeworkstoaddressthefinancialcycle–nottobeinterpretedsequentially,though. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |30 Thediscussioncoversfinancial(specificallyprudential)regulationandsupervision,fiscalandmonetarypolicies. Whilemyfocusisontheglobaleconomy,IwillalsonotethespecificitiesoftheEuropeansituation. I.Thebroadcanvas Stylisedfacts:aneconomichistorian’sperspective Imagineafutureeconomichistorianlookingbackatthebigmacroeconomictrendsfromthefirstoilshockoftheearly1970stoourpresentday. Whatwouldheseeashecasthisgazeoveralongerhistoricaltimespan?Consider,inturn,themostsalientoutcomes,theintellectualbackdrop, thefeaturesofbankingcrises,andinstitutionalsetups. Intermsofoutcomes,hewouldnodoubtbestruckbythemajorshiftinthebehaviourofinflation:fromhighandvariabletolowandstable,withtheinflexionpointaroundtheearly1980s. Atthesametime,hewouldalsonoteamajorincreaseinfinancialcrises,especiallybankingcrises,withseriousmacroeconomicconsequences,inbothadvancedandemergingmarketeconomies. Readingthecontemporaryeconomictextstounderstandtheintellectualbackdrop,hewouldsurelyfinditironicthattheviewprevailingatthetimehadregardedpricestabilityasaguaranteeofmacroeconomicstability. Andthat,inmuchoftheWestduringtheearly2000s,therehadevenbeentalkofaso-calledGreatModeration:agoldenageofstableoutputandlowinflation. Thisconvictionhadhardlybeendentedbythebankingcrisesthathadhitemergingmarketeconomiesandevensomeadvancedonesduringthe1980sand1990s,notleasttheNordiccountriesandJapan. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |31 ToparaphraseReinhartandRogoff,whatseemedtobeatworkwasnotjustthe“this-time-is-different”syndromebutthenolessinsidious “we-are-different”syndrome. IthadtakentheGreatFinancialCrisis,ascontemporarieshadquicklycalledit,whichhaderuptedin2007toshakethiscomplacency. Thehistorianwouldalsonotethattheexperienceofthoseyearshadbeen bynomeansunique. Similareconomicfluctuations,wherelowinflationhadcoexistedwithoccasionalbankingcrises,hadbeenquitecommonintheGoldStandard days,whencountrieshadpeggedtheircurrenciestogold. Indeed,alongeconomicboomwithlowandstableinflationhadusheredinthatotherdefiningmomentineconomichistory–theGreatDepressionintheUnitedStatesintheearly1930s. Then,justaslateron,therehadbeentalkofpermanentprosperity,ofan endtothetyrannyofthebusinesscycle. Ourhistorianwouldthengooneleveldeeper. Hewouldask:“Arebankingcrises,likeTolstoy’sfamousunhappyfamilies,alldifferent?Oraretheymorelikehishappyones,whichareallalike?” Itisalltooeasy,hewouldnote,tospottheidiosyncraticfeaturesofacrisis. Structuredproducts,forinstance,hadnotexistedintheearly1930s. Or,totakejustanotherexample,thecrisesinJapanandNordiccountrieshadcausedhavocinbank-basedfinancialsystems;bycontrast,thesubsequentGreatFinancialCrisishadoriginatedintheUnitedStates,withitssecuritisation-intensive,capitalmarkets-basedfinancialsystem. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |32 Or,again,thecrisisinFinlandhadfollowedthecollapseofitsmain tradingpartner,theSovietUnion;butnoobviousexternalshockhadbeenatworkin2007. Andhecouldgoon. Yet,hewouldquicklyrealisethatfocusingonidiosyncrasieswouldmeanfallingvictimtothe“we-are-different”syndromeinanotherguise. Afullerunderstandingofcrisesrequiresafocusonwhattheyhaveincommon,notonhowtheydiffer. Onlythencanonefindreliableremedies. Afterall,hadnottheJapanesebank-basedfinancialsystembeenhailedassuperioraheadofthecountry’sbankingcrisis? AndhadnotmuchthesamebeensaidoftheUSmarket-basedfinancialsystemaheadofitsownmeltdown? Ourhistorianwouldthenlookforcommonpatterns. Soonenough,anobviousonewouldleapoutathim:crisestendtobeprecededbymajorfinancialboomsandfollowedbyprotractedbuststhatleavedeepscarsintheeconomictissue. Inotherwords,theyarecloselyassociatedwithpeaksinthefinancialcycle. Thejointbehaviourofcreditandassetprices,inparticularpropertyprices,capturethesecyclesremarkablywell. Andsincebankingcrisesarerareeventsinanygivencountry,itisnaturalforthesecyclestobeverylong. Theirorderofmagnitudeisbetween15and20years. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |33 Ashereadfurther,ourhistorianwouldrealisethatthecloseassociationbetweencrisesandfinancialboomsandbustshad,infact,beenrecognisedearlyonintheeconomicsprofession,asfarbackasthe19thcentury. Duringthepost-warperiod,economistssuchasKindlebergerandMinskyhadkepttheconceptaliveatthemarginsofthefield. Theirworkhadinspiredpolicy-orientedresearchaheadoftheGreatFinancialCrisis. Butithadgonelargelyunheeded,drownedinthecontagiousenthusiasm fortheGreatModeration. Memoriesareshort;hubrislong. Butourhistorian’sintellectualcuriositycouldnotstopthere.Hehasestablishedthatfinancialcyclesfomentbankingcrises,withdamaging macroeconomicconsequences. Hehasalsonotedthatfinancialcycleswereacommonfeaturebothofthegoldstandarderaandoftheperiodrunningfromthemid-1980stoourpresentday. Couldthetwoperiodshaveyetmoreincommon?“Yes”,wouldbeourhistorian’sanswer. Andthisconclusionwouldrefertothetectonicplatesoftheglobaleconomy–totheinstitutionsthatembodyits“economicregimes”. Thetwoerashadseenthecoexistenceofmonetarypolicyframeworksthatdeliveredreasonablepricestabilitywithliberalisedfinancialmarketsandhighlyintegratedmarketsforgoods,capitalandlabour. Infact,theyhadcometobeknownasthefirstandsecondwavesofglobalisation. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |34 Thesuccessfulfightagainstinflationdatedbacktotheearly1980s,and hadgraduallyspreadacrosstheworldthereafter. Bythemid-1980spolicymakershadlargelyliberaliseddomesticfinancialmarkets,andbytheendofthatdecade,inthewordsofPadoa-SchioppaandSaccomanni,theglobalfinancialsystemhadturnedfromgovernment-ledtomarket-led. Theintegrationofgoodsandfactormarketshadstartedmuchearlierinthepost-warperiod,butithadtakenaquantumleapinthe1990s,whentheformercommunistcountrieshadenteredthecapitalistproductionsystem. AsThomasFriedmanhadputit,theworldhadbecomeflat–onceagain,heshouldhaveadded. Stylisedfacts:aninterpretation Isthissimilaritybetweendeepstructuresandeconomicoutcomesjustacoincidence? Iwouldsuggestnot. Butnowitisbesttopartcompanywithoureconomichistorian,aswemovefurtherawayfromtherealmofstylisedfactstothatof(wehope)informedconjecturesandtheirpolicyimplications. Itstandstoreasonthatthethreepowerfulforceshaveinteractedsoastodeeplyshapeeconomicfluctuations. Theirconjunctionhasmadeeconomiesmorevulnerabletolargeandprolongedfinancialboomsandbusts–financialcycles–thatcaninflictseveredamageontheeconomy. Duringtheboom“financialimbalances”develop:(privatesector)balancesheetsbecomeoverextendedonthebackofaggressiverisk-taking. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |35 Theimbalancessowtheseedsoftheirowndestruction,andhenceofeconomicweakness,unwelcomedisinflationandfinancialstrainsdowntheroad. Theboomcanturntobusteitherbecauseincipientinflationeventuallydoesemerge,forcingthecentralbanktotightenor,moreoften,becausetheimbalancescollapseundertheirownweight. Onemaycallthispropertyoftheeconomy“excesselasticity”. Theanalogyiswithanelasticband,whichonecanstretchfurtherand furtheruntilatsomepointitsnaps. Thesefinancialboomsandbustsnecessarilytakealongtimetounfold. Astheyemerge,theyslowdowneconomictimerelativetocalendartime. Howmightthetectonicforcesinteracttoproducethisoutcome? First,financialliberalisationmakesitmorelikelyforfinancialfactorsingeneral,andboomsandbustsincreditandassetpricesinparticular,todriveeconomicfluctuations. Ratherthanbeingtightlyboundbycashflowconstraints,theeconomyispropelledbylooselyanchoredperceptionsofassetvaluesandrisks,criticallysupportedbyeasiercreditavailability. Indeed,thelinkbetweenfinancialliberalisationsandsubsequentcreditandassetpriceboomsiswelldocumented. Second,theestablishmentofregimesyieldinglowandstableinflation,underpinnedbycentralbankcredibility,canmakeitlesslikelyforsignsofunsustainableeconomicexpansiontoshowupfirstinrisinginflationandmorelikelyforthemtoemergefirstasunsustainableincreasesincreditandassetprices(the“paradoxofcredibility”). InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |36 Afterall,stableexpectationsmakepricesandwageslesssensitivetoeconomicslack:thisispreciselywhatpolicymakersandeconomistshaveexpectedallalong. Finally,theglobalisationoftherealeconomyhasgivenamajorboosttoglobalpotentialgrowth–whateconomistswouldcallasequenceofpervasivepositive“supplyshocks”oranoutwardshiftintheglobaleconomy’sproductionpossibilityfrontier. ThinkofthehugeboosttoproductioncapacityasChinaandotherformercommunistcountriesjoinedtheworldtradingsystem. Bythesametoken,however,ithassurelyhelpedtokeepinflationdownandprovidedfertilegroundforcreditandassetpricebooms. Policyandhorizons:pre-crisisrole Somuchforthebigpicture–thetectonicplates,sotospeak.Butwhatabouttheroleofdecisionsmadebythepolicymakerswhowere confrontedwiththeseforces? Withhindsightatleast,ithasbecomeclearthatpolicymakersinadvertentlyaddedfueltothefireaheadoftheGreatFinancialCrisis. Theyputtoomuchfaithinmarkets’abilitytoself-correct. Theyfailedtofullyunderstandthatthechanginglandscapecalledforadjustmentsinpolicyframeworks. And,evenwhentheydidunderstand,theyfoundittoohardtochangecourse:toomuchreputationalcapitalwasatstakeand,anyway,whyfixwhatain’tbroken? Consider,inturn,prudential,monetaryandfiscalauthorities. Prudentialauthoritiesconvergedonframeworksthatconcentratedtoomuchonthesafetyandsoundnessofindividualinstitutionsandtoolittle InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |37 onthatofthesystemasawhole–frameworksinwhichthemacroeconomyandthefinancialcyclehardlyfigured. Theyfocusedtoomuchonindividualtreesandtoolittleonthewood. Incurrentjargon,theyhadtoomuchofa“microprudential”focus,asopposedtoa“macroprudential”one. Monetaryauthorities,stillburntbytheGreatInflationexperience,focusednarrowlyonstabilisingnear-terminflation. Theycouldnotjustifyraisinginterestratesifinflationwaslowandstable,letalonefalling,eveniffinancialimbalanceswerebuildingup. Asaresult,theimbalancesproceededtogrowunchecked. Andfiscalauthoritiesfailedtorealisethatfinancialboomswerehugelyflatteringthefiscalaccountsandthatthebustswouldatsomepointpresentthemwithahugebill–aburdenoverandabovethebetterknown,butjustasintractable,oneresultingfromageingpopulations. Underlyingthesefailingswasanaturaltendencytooverestimatesustainableoutputandgrowth. Thenotionthatinflationwasthesoleharbingerofunsustainabilitywasespeciallyinsidious. Financialfactors,again,didnotfigureinthispicture. Thatwastherelentlessmessageoftheprevailingintellectual macroeconomicparadigm,bothareflectionoftheZeitgeistanda contributortoit. Shortpolicyhorizonsplayedakeyroleinallthis. Muchofmacroeconomicpolicycentresonthenotionofthebusinesscycle. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |38 Asconceivedandmeasured,thebusinesscyclehasadurationofeightyearsatmost. Andyetwehaveseenthatthefinancialcyclelastsatleasttwiceaslong. Sincethefinancialcycle’sboomsandbustshavemajorconsequencesforeconomicactivity,nottakingthemintoaccountcancreateseriousbiasesinpolicymaking. Itisasif,ontheopensea,sailorssuccessfullyrodeoutthesmallerwavesbutremainedblissfullyunawareofthetsunamirollingbeneaththem–awavethatwouldsurgeandcrashonlyonceitreachedtheshore. Toillustratethis,considertheexperienceofseveraladvancedeconomiesinthemid-1980stoearly1990sandintheperiod2001–07. Inbothepisodes,policymakersreactedstronglytocollapsesinequityprices–theglobalstockmarketcrashesof1987and2001thatusheredineconomicslowdownsoractualrecessions. Theycutpolicyratesand,toavaryingandsmallerdegree,loosenedthefiscalreins. Inbothepisodes,however,creditandpropertyprices–themostrelevant indicatorsofthefinancialcycle–continuedtoincrease,asifgettingtheirsecondwind. Financialimbalancesbuiltupfurther. Andafewyearslater,thecreditandpropertypriceboomscollapsed,in turn,causingseriousfinancialdamageanddraggingdowntheeconomywiththem. ThisiswhathappenedtoJapaninthefirstepisodeandtotheUnitedStatesandUnitedKingdominboth. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |39 Fromamedium-termperspective,consistentwiththelengthofthefinancialcycle,theslowdownsorcontractionsin1987and2001canthusberegardedas“unfinishedrecessions”. Theinitial“over-reaction”toshort-termmacro-economicdevelopments,followedbyanunder-reactiontothefurtherbuild-upoffinancialimbalances,causedmoreseriousproblemsdowntheroad. Butshorthorizonsarenotjustanissueforpolicymakers.Theyareanevenbiggeronefortheprivatesector,especiallyforfinancialmarketparticipants. Here,traders’horizonsmaybeasshortasaday,orminutesorevenmicroseconds.Moregenerally,horizonsrarelyextendbeyondoneyear, constrainedbytherhythmoffinancialreportingconventions. Moreover,theyhave,ifanything,beenshrinking:technologyhasbeensurgingahead;thespreadoffairvalueaccountinghastelescopedtheindefinitefutureintotheephemeralpresent;tightermonitoringhascometomeanmorefrequentmonitoring. Theseshorthorizonsareembeddedinriskmeasurementtools,suchasvalue-at-risk,incommontradingstrategies,suchasmomentumtrading,andincredittechniques,suchassecuritisation. Forinstance,riskmodelsrelyonextraordinarilyshortdatahistories,hardlyeverextendingbeyondafewyears,andtheyprojectoutcomesover averyshortfuture,mostlydaysandattheverymostoneyear. ShorthorizonsareprobablybestcapturedbythefamouswordsofChuck Prince,thenCEOofCitigroup,totheeffectthat“aslongasthemusicisplaying,youhavetogetupanddance”. Thiswasjustbeforethecrisisbroke. Theendresultisthatmarketparticipants’expectations,onceembeddedinmarketprices,appearhighlyextrapolative:theyfollowthetrenduntilitistoolate. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |40 Hencewhatonemightcallthe“paradoxoffinancialinstability”:thefinancialsystemlooksstrongestpreciselywhenitismostvulnerable. Creditgrowthandassetpricesareunusuallystrong,leveragemeasuredatmarketpricesisartificiallylow,andriskpremiaandvolatilitiessagtorock-bottomlevelspreciselywhenriskisatitshighest. Whatlookslikelowriskis,infact,asignofaggressiverisk-taking. Therecentcrisishassimplyconfirmedthisalloveragain. Aviciouscyclehassetin. Theinteractionbetweenmarketparticipants’instincts,therelentless24/7mediarazzmatazzandtheresponseofpolicymakersbecomeseverstronger;asaresult,horizonsbecomeevershorter. So,thesearchfortheculpritsfortheGreatFinancialCrisisbringsverymuchtomindAgathaChristie’sfamousthriller,MurderontheOrientExpress. Whowasthemurdererthen?Asitturnsout,allthepassengersonthetrainwere. Whoistheculpritnow?Asitturnsout,weallare. II.Post-crisischallenges Thelegacyofthecrisis:abalancesheetrecession Theforegoinganalysiscastslightontherecessionthatfollowedthefinancialcrisis. Notallrecessionsarebornequal. Thetypicalpostwarrecessionwastriggeredbytightermonetarypolicyto stoprisinginflationorabalanceofpaymentscrunch. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |41 Bycontrast,apost-financialcrisisrecessionisabalancesheetrecession,linkedtoafinancialbustagainstthebackdropoflowandstableinflation. Thismeansthattheprecedingexpansionismuchlonger,thesubsequentdebtandsectoralcapitalstockoverhangsmuchlarger,andthedamagetothefinancialsectormuchgreater. Italsomeansthatthepolicyroomformanoeuvreisverylimited:unlesspolicyhasactivelyleanedagainstthefinancialboom,policybufferswillbedepleted. Thecapitalandliquiditycushionsoffinancialinstitutionswillrupture;gapingholeswillopenupinthefiscalaccounts;andpolicyinterestrateswillsagtonearzero. ThinkofJapaninthe1990s. Agrowingbodyofevidencesuggeststhatbalancesheetrecessionsareparticularlycostly. Theytendtobedeeper,togivewaytoweakerrecoveries,andtoresultin permanentoutputlosses:outputmayreturntoitspreviouslong-termgrowthratebutnottoitspreviousgrowthpath. Severalfactorsarenodoubtatworkhere:theoverestimationofboth potentialoutputandgrowthduringtheboom;themisallocationofresources,notablythecapitalstockbutalsolabour,duringthatphase;theoppressiveeffectofthedebtandcapitaloverhangsduringthebust;andthedisruptionstofinancialintermediationoncefinancialstrainsemerge. Afullfiveyearsafterthebeginningofthefinancialcrisis,thesymptomsofabalancesheetrecessionarealltooevident. BanksinEuropeand,toalesserextent,theUnitedStatesremainweak–althoughintheUnitedStatesitisGovernmentSponsoredEnterprises(GSEs)thataremoreexposedtothemortgagemarket. Tobesure,bankshavesignificantlybeefeduptheircapitalratios. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |42 Buttheircreditdefaultswaps,gaugesofperceivedcreditworthiness,havereturnedtolevelsthatarenotthatfarawayfromthosethatprevailedwhenLehmanBrotherscollapsed. Meanwhile,theirshareshavelostgroundagainsttherestofthestockmarket,andtheyhaveincurreddowngradesacrosstheboardinbothstandaloneandall-inratings. Privatesectordebt-to-GDPratios,ameasureofaggregateleverage,arestillveryhigh.Sovereigndebthasballoonedandsovereignshavebeendowngraded. Thepolicyratesofleadingeconomieslanguishattheireffectivezerolowerboundwhilethebalancesheetsoftheircentralbankshaveswelled enormously. Globally,though,therearesignificantdifferencesbetweencountries. Thosethathaveexperienceddomesticfinancialboomsandbustshavefacedseriousstrainsinbothnon-financialsectorandbankbalancesheets;tovaryingdegrees,theyareseeingdeleveraginginbothsectors. ClearexamplesaretheUnitedStates,theUnitedKingdom,SpainandIreland. Thosewhosefinancialinstitutionswereexposedtofinancialboomselsewherehavealsoseenseriousstrainsintheirbanks,buttheirnon-financialprivate-sectordebt-to-GDPratioshavetypicallyrisen furtheronthebackofcreditexpansion. NotableexamplesareGermany,FranceandSwitzerland. Indeed,inSwitzerlandastrongandpossiblyunsustainablehousingboomisunderway,despiteratherweakeconomicgrowth. Thosewhosebankswerenotdirectlyexposedtothefinancialbustsinmatureeconomies,afterabriefslowdown,haveprovedveryresilient; InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |43 manyofthemhavecontinuedtoseefinancialbooms,sometimeseerilyreminiscentofthepre-crisisonesinmatureeconomies. Theseincludeseveralemergingmarketeconomiesandsomecommodity-basedadvancedcountries,amongothers. Thesituationisparticularlyworryingintheeuroarea. Itistherethattheperversefeedbackloopbetweentheweaknessesinthebalancesheetsofbanksandsovereignshasbeenmostintense. Anobviouslyincompleteeconomicandmonetaryunionhasbroughtit intotheopenandexacerbatedit. Thatsaid,oneshouldnotconfusethesymptomswiththedisease.Marketscananddolullpolicymakersintoafalsesenseofsecurity. Theyarefartooslowtoreactand,whentheydo,theyreactviolently.Thereareothermajorcountrieswhoseunderlyingfiscalpositionsare hardlymoresustainablethanthoseintheeuroarea. Andyetbondmarketsseemtobeoblivious,atleastfornow. Theimmediatepolicychallenge:returningtoself-sustaining andsustainablegrowth Theimmediateglobalpolicychallengeistoreturntoself-sustainingandsustainablegrowth. Seenthroughthelensofthefinancialcycle,thisraisesdifferentissuesacrosscountries,dependingontheirspecificsituation. Atoneend,forthoselargelysparedbythecrisis,andthathavebeenseeingsignsofunsustainablefinancialbooms,thechallengeistocontaintheseexcessesandtoavoidoverestimatingthestrengthoffiscalpositions. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |44 Wherethecyclemighthaveturnedalready,itistocontainthedamage.Attheotherend,forthosethatwereattheepicentreofthecrisisandhave experiencedadomesticfinancialboomandbust,thechallengeistodealwithtwinweaknessesinthefinancialandnon-financialsectorbalancesheets. Somewhereinbetween,forthosewhosebankshavesufferedfromlossesonexposurestofinancialbustselsewhere,thechallengeistosolvethebanks’problems,evenasthenon-financialsectormaybeintheprocessofleveragingupfurther. Forall,thechallengeistoensurethatthesovereignremainscreditworthyorregainsitslostcreditworthiness. Inwhatfollows,Iwillleaveittothereadertodrawimplicationsforspecificcountries. Instead,Iwillfocusonthegeneralchallengesthatbalancesheetrecessionsraise,ieonhowtoaddressfinancialbusts. Iwillthendiscusshowtoaddressboomsinthefollowingsub-section,whichconsidersthelonger-termchallengeofhowtoadjustpolicyframeworks:howtoaddressboomsisbynowbetterunderstoodandrequireslesselaboration. Themainpolicychallengeinabalancesheetrecessionistopreventastockproblemfrommorphingintoalong-lastingflowproblem,weighingdownonincome,outputandexpenditures. Itisthereforecriticaltodistinguishtwophases,crisismanagementandcrisisresolution,whichdifferintermsoftheirpriorities. Incrisismanagement,thepriorityistopreventtheimplosionofthefinancialsystem,soastowardoffthethreatofaself-reinforcingdownwardspiralineconomicactivity. Restoringconfidenceisessential. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |45 Ifthereisscopetodoso,policiesshouldbedeployedaggressively. Thisisthephasehistoricallylinkedtocentralbanks’lender-of-lastresortfunction;togetherwithinterestratecuts,suchacourseofactioncanbeespeciallyhelpfulinboostingconfidence. Incrisisresolution,bycontrast,thepriorityisbalancesheetrepair,soastolaythebasisforaself-sustainingrecovery. Hereitisessentialtotacklethedebtoverhanghead-on.Andpoliciesneedtobeadjustedaccordingly. Consider,sequentially,therolesofprudential,fiscalandmonetarypolicyinthisphase. Thepriorityforregulationandsupervisionshouldbetoinducethethoroughrepairofbanks’balancesheetsandtosupportbanks’returntosustainableprofitability. Thismeans: Enforcingfullrecognitionoflosses(writedowns); Recapitalisinginstitutions(subjecttotoughtests),includingpossiblyviatemporarypublicownership; Sortinginstitutionsaccordingtotheirviability;Dealingwithbadassets(includingthroughdisposal); Reducingexcesscapacityinthefinancialsystem;andpromoting operationalefficiencies. ThisispreciselywhattheNordiccountriesdidwhentheyfacedtheirbankingcrisesintheearly1990s;anditiswhatJapanfailedtodoaroundthesametime. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |46 Thisdifferencewasnodoubtakeyfactorbehindtheirdivergenteconomicperformancesubsequently. Beforetherecentcrisis,theresponseoftheNordiccountriestotheircrisiswasuniversallyregardedastherightwaytogo. Suchapolicywouldhaveseveralbenefits. Itwouldrestoreconfidenceinthebankingsystem. Atpresent,forinstance,market-to-bookvaluesarewellbelow1andthereislittleuncollateralisedfundingonoffertobanks,especiallyforEuropeanones. Suchapolicywouldalsounblockinterbankmarketsandrelievepressureoncentralbanks–justthinkoftheEurosystem’sextraordinarylong-termunconditionalliquiditysupporttobanks. Anditwouldrestoreincentivesforallocatingcreditproperlyandavoidinginappropriaterisk-taking. Itishardlyacoincidencethatvolatiletradingprofitshavebeenthemainsourceofincomesincethecrisisandthatoneglobalbankhasrecentlymadesizeabletradinglossesonitscreditportfolio. Unlesslossesarefullyrecognised,viableinstitutionsarerecapitalisedand unviableonesinducedtoexit,theincentiveswillstayinplaceforbankstotakeonthewrongrisksattheexpenseofthegoodones,andtooverchargehealthyborrowerstothebenefitofunhealthyones. Whenthelevelofdebtinaneconomyistoohighandmustbecutbacktosetthesceneforaself-sustainingrecovery,theallocationofcreditismoreimportantthanitsoverallamount. Thepriorityforfiscalpolicyshouldbetocreatethescopeforusingthepublicsectorbalancesheettosupporttherepairofprivatesectorbalancesheets. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |47 Thisappliestothebalancesheetsoffinancialinstitutions,throughinjectionsofpublicsectormoney(capital)subjecttostrictconditionalityonlossrecognitionandpossiblythroughtemporarypublicownership. Butitappliesalsotothebalancesheetsofthenon-financialsectors,suchashouseholds,includingthroughvariousformsofdebtrelief. Suchaprescriptioncontrastssharplywithawidespreadviewamong macroeconomists,whowouldregardpump-priming(increasesinexpendituresortaxcuts)asmoreeffectiveduringslumps. Thatview,however,assumesthatpeoplewishtoborrowandcannot. Butiftheyhavealreadytakenontoomuchdebt,theyaremorelikelytowishtocutthatburden. Debtrepaymentwouldtakepriorityovermorespending. Ifso,eventheshort-termeffectofuntargetedfiscalexpansion(theso-called“fiscalmultiplier”)islikelytobesmall. Ratherthanjump-startingtheeconomy,itcouldendupbuildingbridgestonowhere,astheJapaneseexperiencesuggests. Bycontrast,thetargeteduseofthefiscalroomformanoeuvretosupportthebalancesheetrepairofthefinancialandnon-financialsectors,asneeded,couldremoveakeyobstacletoaself-sustainingrecovery. Moreover,asanownerorco-owner,thesovereigncouldactuallymakecapitalgainsinthelongerterm,aswasthecaseinsomeNordiccountries. Importantly,thisisnotapassivestrategy,butaveryactiveone.Itinevitablysubstitutespublicsectordebtforprivatesectordebt. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |48 Itrequiresaforcefulapproachtoaddressingtheconflictsofinterestsbetweenborrowersandlenders,betweenmanagers,shareholdersand debtholders,andsoon. Anditraisestrickydistributionalquestions. Itisnotpurefiscalpolicyinthetraditionalmacroeconomicsense:itcallsforabroadersetofmeasures,includinglegaladjustments,supportedbythepublicpurse. Butwhatifthecountryisalreadyfacingasovereigncrisis?Mysenseisthat,evenwhereimmediatefiscalconsolidationisnecessary,thisuseofpublicmoneyiscritical. TheNordiccountriesdidit,evenastheycutelsewhere. Onewayofalleviatingthetrade-offsistoobtaintargetedexternalsupport. Thereisaclearpotentialforthatoptionintheeuroarea,especiallyaspartofawellsequencedandcomprehensiveshifttowardsamorecompleteeconomicunion. Andevenasshort-termstepsaretaken,along-termhorizonisessential.Theevidenceindicatesthatanycontractionaryeffectsoffiscalpolicy dissipateovertime. Andrestoringthecreditworthinessofthesovereignisparamount. Thesovereignistheultimatebackstopforthefinancialsystemandtheeconomy. Therecannotbelastingfinancialandmacroeconomicstabilityifpublic financesremainonanunsustainablepath. Whataboutmonetarypolicy? InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |49 Thepriorityistorecogniseitslimitationsandtoavoidoverburdeningit.Monetarypolicyislikelytobelesseffectiveinabalancesheetrecession.Thisappliesasmuchtochangesinshort-terminterestratesandguidance aboutfuturerates(“interestratepolicy”)asitdoestoanaggressiveuseofthecentralbankbalancesheet,suchasthroughlarge-scaleasset purchasesandliquiditysupport(“balancesheetpolicy”). Overlyindebtedagentsunwillingtoborrowandabankingsystemunabletofunctionblunttheimpactofsuchpoliciesonexpenditure. Asaresult,aspolicymakerspressharderonthegaspedal,theenginerevsupwithouttraction. Andthisexacerbatesanysideeffectsthatpolicymayhaveinthecrisisresolutionstage. Severalpossiblesideeffectsmayarisefromalongperiodof extraordinarilyaccommodativemonetarypolicy. First,easingcanmaskunderlyingbalancesheetweaknesses. Itmakesiteasiertounderestimatetheprivateandpublicsector’sabilitytorepayinmorenormalconditionsanddelaystherecognitionoflosses(egevergreening). Second,itcanblurincentivestoreduceexcesscapacityinthefinancialsectorandevenencouragebettingforresurrection. Third,itcanunderminetheearningscapacityoffinancialintermediaries,bycompressingbanks’interestmarginsandsappingthestrengthofinsurancecompaniesandpensionfunds. This,inturn,weakensthebalancesheetsofnon-financialcorporations,householdsandthesovereign. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com

P age |50 ItisnocoincidencethatJapan’sinsurancecompaniescameunderseriousstrainafewyearsafteritsbanksdid. Fourth,itcanatrophymarketsandmaskmarketsignals,ascentralbankstakeoverfinancialintermediationfunctions. Interbankmarketstendtoshrinkandriskpremiabecomeunusuallycompressedaspolicymakersbecomelarge-scaleassetbuyers. Fifth,whileitcanhelprepairbalancesheetsbyweakeningthecurrency,thismaybeunwelcomeelsewhere,asitmaybeseenashavinga beggar-thy-neighbourcharacter–apointtowhichIwillreturnlater. Finally,overtimeitmaycompromisetheoperationalautonomyofthecentralbank,aspoliticaleconomyconsiderationsloomeverlarger. Thisisespeciallyimportantforcentralbanks’balancesheetpolicy,becauseofitsquasi-fiscalnature. Thekeyriskisthatcentralbanksbecomeoverburdenedandaviciouscircledevelops. Monetarypolicycangaintime,butitcanalsomakeiteasiertowastetime,becauseoftheincentivesitgenerates. Asthepolicyfailstoproducethedesiredeffectsandadjustmentisdelayed,centralbankscomeundergrowingpressuretodomore. An“expectationsgap”yawnsopen,betweenwhatcentralbanksareexpectedtodeliverandwhattheycandeliver. Allthismakestheeventualexitmoredifficultandmayultimatelythreatenthecentralbank’scredibility. OnemaywonderwhethersomeoftheseforceshavenotbeenatplayinJapan,acountrywherethecentralbankhasnotyetbeenabletoexit. InternationalAssociationofRiskandComplianceProfessionals(IARCP) www.risk-compliance-association.com