Download

1 / 35

350 likes | 358 Vues

Role/Importance in External Financial Reporting September 29 , 2004. Mike Willis Founding Chairman, XBRL International Partner, PricewaterhouseCoopers Mike.willis@us.pwc.com. Willis lives here. Frances. Willis lives here. Jeanne. Corporate Reporting Processes.

E N D

Role/Importance in External Financial ReportingSeptember 29, 2004 Mike Willis Founding Chairman, XBRL International Partner, PricewaterhouseCoopers Mike.willis@us.pwc.com

Willis lives here Frances

Willis lives here Jeanne

Corporate Reporting Processes

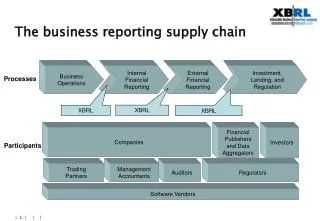

The corporate reporting supply chain Companies Financial Publishers and Data Aggregators Investors Central Banks Participants Trading Partners Auditors Regulators Management Accountants Software Vendors Business Operations Internal Financial Reporting External Financial Reporting Investment, Lending, Regulation Economic Policymaking Processes

External Reporting XBRL Ledger XBRL External Reporting Business Operations Internal Financial Reporting External Financial Reporting Investment, Lending, Regulation Economic Policymaking Processes

Consolidated Profit and Loss Account for the year ended June 30, 2004

Democratizing Access to Financial InformationPercentage of Companies Receiving Coverage Includes all common stock on NASDAQ National Market and NYSE. Source: Thomson Financial. December 2002.

What is XBRL • An international market driven corporate reporting information format standard • A platform for corporate reporting standards already adopted by the IASB for IFRS • A market reality with broad and accelerating regulatory adoption around the world • A standard that can enhance the quality and efficiency of business reporting of all types • A way to enhance the analysis of information contained within business reports both internal and external to the enterprise

XBRL (eXtensible Business Reporting Language) is: • Available on a royalty free basis • The convergence of: • Technology = XML-based specification (information format) • Language / dictionary = (information) • Terms by jurisdiction (US, Germany,Ireland, Spain, Japan,….), • Terms by regulation / industry (Basel 2, IFRS, GL, Accountants, Analysts,….) • Collaboration by over 250 market participants

What is the Opportunity? • Manual supply chain orientation • Need for greater accuracy and efficiency • External reuse is largely ignored • Cost of consuming information is high • Accuracy and timeliness are victimized • Analysis adversely impacted • Transparency is all about content • Opacity thrives • Uninformed decisions are the status quo

Information Cost and Value equation • Value = Reduction of uncertainty times $$$ at risk • Cost = Produce + Structure + Distribute + Consume XBRL provides a powerful ROI as it puts information in the hands of consumers at lower costs (both production and consumption)

Benefits of XBRL for Preparers • Lower cost of producing information • More timely, accurate, data for decisions • Enhanced analytical capabilities • Better control environment • Tell your own story (precise & clear) • Accelerate adoption of reporting models • Enhanced functionality • Ease of use

Benefits of XBRL for Consumers • Lower cost of consuming information • Faster access to information • More timely, accurate, data for decisions • Enhanced analytical capabilities • Enhanced functionality • More useful access to information • Ease of access to definitions enhance comparability • Facilitates language translations

Regulator Regulator Regulator Company Regulator Regulator Regulator Company Company Regulator Regulator Regulator Regulator Company Company Company Regulator Regulator Regulator Regulator Company Company Company Regulator Regulator Regulator Regulator Company Company Company Regulator Regulator Regulator Regulator Company Problem = Exchange of data between regulated entity and regulator Company Regulator Regulator Regulator Regulator Regulator Regulator Regulator Regulator Company Regulator Regulator Regulator Regulator Company Company Company Regulator Regulator Regulator Regulator Company Regulator Company Company Regulator Regulator Regulator Regulator Company Regulator Company Company Regulator Regulator Regulator Regulator Company Regulator Company Company Regulator Regulator Company Regulator Regulator XML Schemas Company Regulator Regulator Regulator Regulator Proprietary solution for Regulator Looks good to the regulator Regulator Regulator Regulator Regulator Company Regulator XML Schema Company Company Regulator Regulator Regulator Company Regulator Company Company Company Regulator Regulator Company Regulator Regulator Company Company Company Regulator Regulator Company Regulator Regulator Company Company Company Regulator Regulator Company Regulator Company Company Company Regulator Regulator Company Regulator Company Regulator Regulator Proprietary solutions looks different to the companies and is a costly and complex model Regulator Company Company Regulator Regulator Regulator XML Schema Company Company Regulator Regulator Regulator Company Company Regulator Regulator solution = Use XML Schema to define terms for exchange. Regulator builds taxonomy using a (XML Schema) proprietary platform. Company Regulator Regulator Company Company Company Regulator Regulator Company Company Company Regulator Regulator Company Company Company Regulator Solution development – can be siloed

Regulations Stds (FASB, IFRS) Interpretative Guidance 3rd Party Interpretative Guidance Audit Guidance Instructions Internal Reporting Instructions Reporting Sources XBRL Solution development - Collaborationyields benefits to all participants Publicly available Company Regulator Validation

Taxonomy Development • More than just definitions (XML Schema + Link) • Structure for information • FRTA = Taxonomy Architecture (extensibility rules) • Components • Definition • Presentation • Classification • Calculation • Reference • Building Blocks

XBRL – More Than Just Definitions • XBRL adds to XML: • Multi dimensional financial data representations • Financial reporting vocabularies (taxonomies) • Aliases and other definition relationships • Mathematical relationships between concepts • Flexibility about how to present items to users • Structure for authoritative policies and guidance Reporting apps need these even when using XML Definitions cashCashEquivalentsAndShortTermInvestments References GAAP I.2.(a) Instructions Ad Hoc disclosures Presentation Receivables / Les créances/… XBRL Item “200” Label US $ FY2004 Budgeted FormulasCash ≥ 0 Calculations Cash = Currency + Deposits

Taxonomy as Dictionary Disclosure Income Expense Result inc exp inx Advertising Marketing Profit Net Interest exp.adv exp.mkt inx.prf inx.int

Disclosure Note aux comptes Revelación 開示 Produits Income Ingresos Charges Gasto Expense Résultat Result Resultado 所得 経費 結果 Publicidad Advertising Publicité Frais de commercialisation Marketing Marketing Gains Ganancia Profit Intérets nets Net Interest Interés neto 広告 マーケティング 利益 純利子 Taxonomy as Presentation (alternatives)

Taxonomy as Classification Disclosure Defined as Income Expense Result Defined as Defined as Advertising Marketing Profit Net Interest

Taxonomy as Calculation Disclosure Added into Income Expense Result Subtracted from Added into Added into Advertising Marketing Profit Net Interest Added into

Taxonomy as online reference Disclosure Income Expense Result Analyst Report Benchmarks Instructions Any content GAAP Advertising Marketing Profit Net Interest

Taxonomy as Reusable Building Block Disclosure Added into Income Expense Result Subtracted from Added into Added into Advertising Marketing Profit Net Interest Rebates Added into Website Expenses

Taxonomy as Collaborative Effort • Agree • Agree • Agree • Agree Disclosure Income Expense Result Advertising Marketing Profit Net Interest

XBRL “Building Blocks” Bank of New Orleans Terms Company/Industry Specific Terms GAAP Bank Terms Industry Terms GAAP FS Terms GAAP Primary Terms Foundational Terms GAAP Conceptual Framework Reporting Framework

Role/Importance in External Financial ReportingSeptember 29, 2004 Mike Willis Founding Chairman, XBRL International Partner, PricewaterhouseCoopers Mike.willis@us.pwc.com