Download

1 / 20

200 likes | 420 Vues

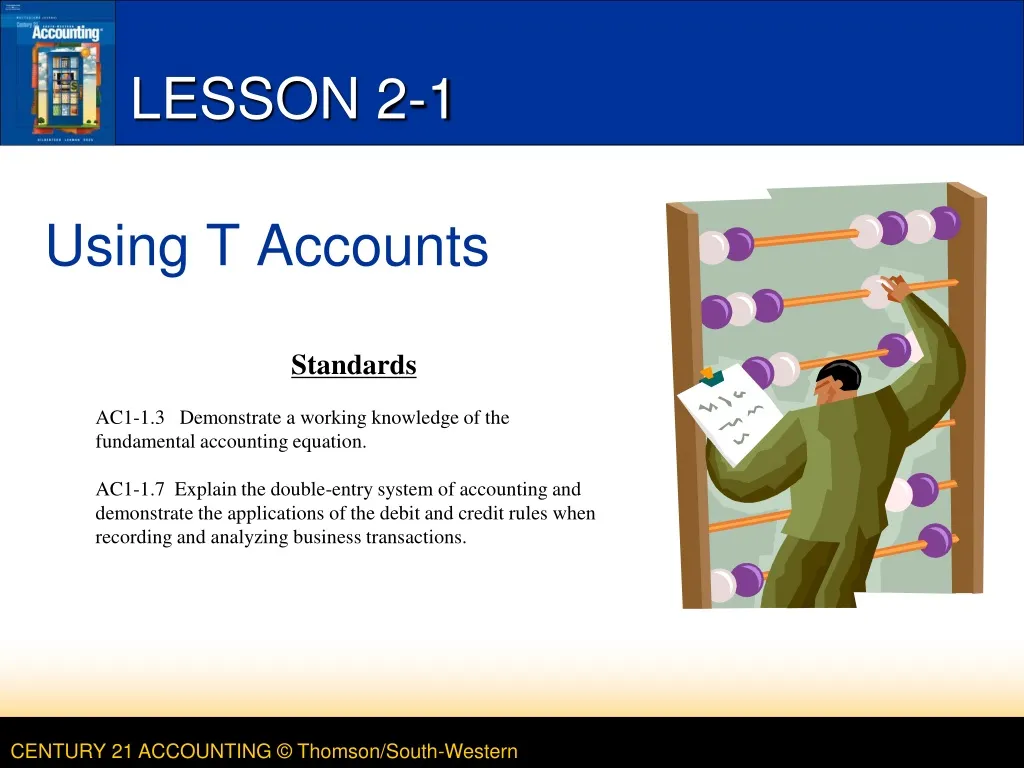

LESSON 2-1. Using T Accounts. Standards AC1-1.3 Demonstrate a working knowledge of the fundamental accounting equation. AC1-1.7 Explain the double-entry system of accounting and demonstrate the applications of the debit and credit rules when recording and analyzing business transactions.

E N D

LESSON 2-1 Using T Accounts Standards AC1-1.3 Demonstrate a working knowledge of the fundamental accounting equation. AC1-1.7 Explain the double-entry system of accounting and demonstrate the applications of the debit and credit rules when recording and analyzing business transactions.

ANALYZING THE ACCOUNTING EQUATION page 28 I can explain how to determine the debit and credit side of an account.

ACCOUNTS page 29 I can explain how to determine the debit and credit side of an account.

ACCOUNT BALANCES page 29 I can explain how to determine the normal balance of an account.

INCREASES AND DECREASES IN ACCOUNTS page 30 I can determine the increasing and decreasing side of an account.

TERMS REVIEW page 31 • T account • debit • credit • normal balance

LESSON 2-2 Analyzing How Transactions Affect Accounts

2 2 1 1 4 4 3 3 RECEIVED CASH FROM OWNER AS AN INVESTMENT page 32 August 1. Received cash from owner as an investment, $5,000.00. I can follow the process of determining debit and credit parts for a transaction. 1. Which accounts are affected? 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 1 1 4 4 3 3 PAID CASH FOR SUPPLIES page 33 August 3. Paid cash for supplies, $275.00. I can follow the process of determining debit and credit parts for a transaction. 1. Which accounts are affected? 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 1 1 4 4 3 3 PAID CASH FOR INSURANCE page 34 August 4. Paid cash for insurance, $1,200.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 2 1 1 4 4 3 3 BOUGHT SUPPLIES ON ACCOUNT page 35 August 7. Bought supplies on account from Supply Depot, $500.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 2 1 1 4 4 3 3 PAID CASH ON ACCOUNT page 36 August 11. Paid cash on account to Supply Depot, $300.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

TERM REVIEW page 37 • Chart of Accounts • Do: Work Together 2-2: • Do: OYO 2-2 • Do: Application problem 2-1

LESSON 2-3 Analyzing How Transactions Affect Owner’s Equity Accounts

2 2 1 1 4 4 3 3 RECEIVED CASH FROM SALES page 38 August 12. Received cash from sales, $295.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 2 1 1 4 4 3 3 SOLD SERVICES ON ACCOUNT page 39 August 12. Sold services on account to Oakdale School, $350.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

1 2 2 4 3 3 1 4 3 PAID CASH FOR AN EXPENSE page 40 August 12. Paid cash for rent, $300.00. 1. Which accounts are affected? 2. How is each account classified? I can follow the process of determining debit and credit parts for a transaction. 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 1 1 4 4 3 3 RECEIVED CASH ON ACCOUNT page 41 August 12. Received cash on account from Oakdale School, $200.00. 1. Which accounts are affected? I can follow the process of determining debit and credit parts for a transaction. 2. How is each account classified? 3. How is each classification changed? 4. How is each amount entered in the accounts?

2 1 4 3 3 1 2 4 3 PAID CASH TO OWNER FOR PERSONAL USE page 42 August 12. Paid cash to owner for personal use, $125.00. 1. Which accounts are affected? 2. How is each account classified? I can follow the process of determining debit and credit parts for a transaction. 3. How is each classification changed? 4. How is each amount entered in the accounts?

Chapter 2 Work Do: Work Together and On Your Own: 2-3 Application 2-4 Mastery Problem 2-5 Study Guide 2 Summative work for chapter 2: • Challenge Problem 2-6 • TEST: CHAPTER 2 Standards AC1-1.2 Explain the importance of following Generally Accepted Accounting Principles (GAAP) and interpret the standards correctly. AC1-1.3 Demonstrate a working knowledge of the fundamental accounting equation. AC1-1.7 Explain the double-entry system of accounting and demonstrate the applications of the debit and credit rules when recording and analyzing business transactions.