Download

1 / 18

190 likes | 301 Vues

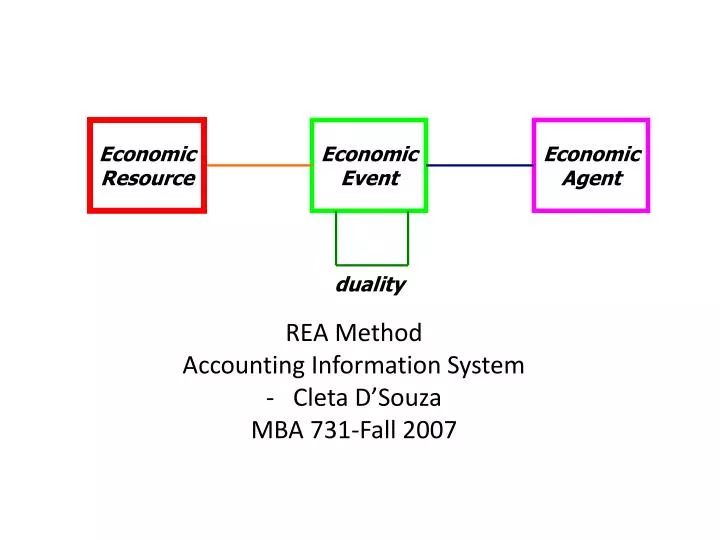

REA Method Accounting Information System Cleta D’Souza MBA 731-Fall 2007. Economic Resource. Economic Event. Economic Agent. duality. AIS- Accounting Information System.

E N D

REA Method Accounting Information System CletaD’Souza MBA 731-Fall 2007 Economic Resource Economic Event Economic Agent duality

AIS- Accounting Information System “An accounting information system is one that captures, stores, manipulates, and presents data about an organization’s value-adding activities to aid decision makers in planning, monitoring, and controlling the organization”

REA • Resources, Events, Agents (REA) is a model of how an accounting system can be reengineered for the computer age. • REA stands for, R- Resource E- Event A- Agent • REA accounting model is developed using data modeling techniques • Its structure consists of sets representing economic resources, economic events and economic agents and the relationships that exists between them • REA was originally proposed in 1982 by William E. McCarthy as a generalized accounting model, and contained the concepts of resources, events and agents.

TABLE 1 Categorization of Accounting Frameworks

Features of REA • An extension of the conventional accounting models to include management information needs of managerial decision models and non financial measures of effectiveness. • Rea Model provides shared data access to accountant and non accountants • A generalized E-R representation of an accounting phenomena. • REA helps represent traditional accounting debit-credit phenomena.

REA explores the issues of database design and E-R accounting methodology, to include the concept of generalization. • REA replaces bookkeeping schemes with an accounting framework whose structure is derived with semantic modeling and whose elements correspond to the accounting principles.

Steps • Database design process where needs of both accountants and non accountants are serviced through shared access to centrally stored data. - Conceptual schema, defines entities, their properties and relationships. • E-R representation of the accounting phenomena. (REA Accounting Model)

Database Design Process • Database design - Requirements analysis - View modeling - View integration

REA Data Model- Elements • Economic Resources Includes objects that are scarce and have utility under control of an enterprise (includes Assets except Accounts receivables) • Economic Events a class of phenomena which reflects changes in scarce means resulting from production, exchange, consumption and distribution • Economic Agent Includes persons and agencies who participate in the economic events or who are responsible for the subordinates participation. - Economic Units A subset of economic agent, are inside the economic agents- work for the economic agent or are part of the enterprise. • Control Relationship/Participant A three way relation between an event, an insider agent (unit) and a outsider (agent).

Generalizing of Data • When all the generalized elements are combined the E-R framework as shown below results.

REA Template Economic Resource Inside Agent Economic Event Outflow Participant Outside Agent Give Duality Take Outside Agent Economic Event Inflow Participant Inside Agent Economic Resource

Revenue Process using REA Model Inventory Sales Person Sale Outflow Participant Give Customer Duality Take Cash Receipt Inflow Participant Cashier Cash

The relationship between customer and sales is a 1:N relationship. We make the primary key for the entity that occurs only once (customer) serve as a foreign key in the entity that can occur many times (sale). Customer Sale Inventory Employee Customer Cash Receive Cash

Table Name Primary Key Foreign Key Other Attributes Sale Sale No. Customer No., Employee No. Date of Sale, Time of Sale, Total Amount of Sale Receive Cash Cash Rect. No. Employee No., Customer No., Receipt Date, Receipt Time, Account No. Total Amount of Receipt Sale No., Inventory Item No. Description, List Price Cash Account No. Bank, Type of Account Customer Customer No. Customer Name, Customer Address, Customer Phone Employee Employee No. Employee Name, Employee Address, Employee Phone, Job Title Sales-Inventory Sale No.-Item Quantity Sold, Actual Price No. EXAMPLE

Where can REA be applicable? Labeled as an accounting system. Can be used for various other business functions. • Supply chain collaboration • inventory control (assigning goods to resources, transfers to events, and owners to agents.) • for payroll by assigning lengths of time to resources (assigning time cards to events, and employees to agents.)

Different perspectives on REA modeling needed for enterprise modeling (value chains) and collaboration space (supply chains) • Enterprise modeling (as evidenced in normal ERP systems) is done from the perspective of one company or entrepreneur. Business processes are viewed as components of a single value chain. A single exchange (like the sale of a product for money) would be modeled twice, once in the enterprise system of each trading partner. • Collaboration space modeling (as evidenced in ebXML or ISO Open-edi) is done from a perspective independent of each trading partner. A single exchange is modeled once in independent terms that can be then mapped into internal enterprise system components. Supply chains are networks of business processes that alternate internal transformations and external exchanges (definition due to Bob Haugen). • REA modeling works in both cases and the independent to trading partner mapping is absolutely straightforward and completely defined.

References • Dunn, Cheryl L, and William McCurthy. "The REA Accounting Model: Intellectual Heritage and Prospects for Progress." Michigan State Uniiversity. http://www.msu.edu/user/mccarth4/DUNN&MC.htm (accessed November 4, 2007). http://www.msu.edu/user/mccarth4. • McCarthy, William. "An Entity-Relationship View of Accounting Models." The Accounting Review, 1979. • McCarthy, William. "The REA Accounting Model: A Generalized Framework for Accounting Systems in a Share Data Environment." The Accounting Review, 1982. • Romney, and Steinbart. "Implementing an REA Model in a Relational Database." In Accounting Information Systems, by Romney and Steinbart. Prentice Hall Publishing, 2006. • Wikipedia. http://en.wikipedia.org/wiki/Resources,_Events,_Agents (accessed November 3, 2007).