Download

1 / 52

520 likes | 766 Vues

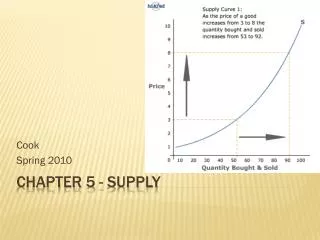

Chapter 5/6: Supply/Prices. Section 1: Understanding Supply. Supply is the counterpart to demand, together they shape markets. Supply. Supply is the amount of goods or services available. Law of Supply. Suppliers will offer more of a good at a higher price, and vice versa. Price. Supply.

E N D

Section 1: Understanding Supply • Supply is the counterpart to demand, together they shape markets.

Supply • Supply is the amount of goods or services available.

Law of Supply • Suppliers will offer more of a good at a higher price, and vice versa. Price Supply Supply Price

Supply Schedule • A supply schedule is a table that lists quantity supply levels at different prices.

Market Supply Schedule • A market supply schedule charts supply levels for an entire economy.

Supply Curve • Supply curves plot the data from demand schedules onto a graph.

Creating our own supply schedule How much would you sell an ipad for?

Elasticity of Supply • Elasticity measures the way supply responds to changes in price. • Elastic supply = supply changes greatly • Inelastic supply = supply doesn’t change much

Elastic Supply • An increase/decrease in price greatly impacts the level of supply. • Examples?

Inelastic Supply • An increase/decrease in price doesn’t greatly impact the level of supply. • Examples?

Section 3: Costs of Production • Supply is influenced not only by demand, but by the costs of production.

Costs • Costs can be divided into two categories… • Fixed cost: a cost that does not change, no matter how much is produced. • Variable cost: A cost that rises and falls depending on how much is produced.

Business Cost Exercise • With a partner, quickly create a business idea. • Come up with a list of all the different costs you will have in supplying your good/service.

Business Cost Exercise • With a partner, quickly create a business idea. • Come up with a list of all the different costs you will have in supplying your good/service. • Determine which are fixed costs and which are variable.

Examples of Fixed and Variable Costs • Fixed: • Rent/mortgage • Equipment purchase/repair • Property taxes • Salaries of workers • Variable: • Extra resources to produce more • Extra employees • Advertising/Marketing • Utilities: heat/electric

Total Cost • Fixed costs + variable costs = total cost

Managing Variable Costs • Businesses need to decide whether creating additional supply is worth the additional costs.

Section 3: Changes in Supply • Like demand curves, sometimes shifts occur along the curve, and sometimes the entire curve shifts.

Supply Shifts • Impacts on supply include… • Change of price for good/service • Production costs • Technology • Government influence on supply

Supply Curve • Supply Curves can shift right or left depending on increased or decreased supply levels at all costs.

Impacts on Supply: Technology • Improved technology often increases the potential supply for goods or services.

Impacts on Supply: Government • Subsidies: government payment to support a business or market. • Examples: agriculture, oil

Impacts on Supply: Taxes • Taxes impact supply levels • Excise tax: tax on the production or sale of a good (often to discourage their supply)

Impacts on Supply: Government • Regulation: government regulation can increase or decrease supply. • Example: environmental regulation

Future Expectations • Future expectations impact supply: will the demand go up or down for this product?

Chapter 6: Prices • Prices are always changing, based on availability (supply) and demand.

Section 1: Combining Supply & Demand • Together, supply and demand interact to determine prices.

Equilibrium Price • The point where demand and supply meet is the equilibrium point where prices are set.

Supply/Demand Curve • Equilibrium point is where the two lines intersect.

Disequilibrium • Disequilibrium occurs whenever the amount supplied is not equal to the amount demanded at a certain price.

Excess Demand • Excess demand occurs when there is more demand than supply.

Excess Demand • When the price is below equilibrium, excess demand occurs.

Excess Supply • Excess supply happens when there is more supply than demand.

Excess Supply • When the price is above equilibrium, excess supply occurs.

Government Intervention: Price Ceilings • Sometimes government intervenes to control prices. • Price ceiling: a maximum price that can be legally charged for something. • Example: rent control

Government Intervention:Price Floor • Price Floor: a minimum amount that can be charged for an item. • Example: Agriculture, minimum wage.

Section 2: Changes in Equilibrium • As supply and demand shift, equilibrium prices change.

Shifts in Supply • If demand remains the same… • An increase in supply will lower price. • A decrease in supply will raise the price. • Example: bacon shortage!

Increase in Supply Curve • A new supply curve changes the equilibrium price. P1 P2

Decrease in Supply Curve • A new supply curve changes the equilibrium price. P2 P1

Shifts in Demand • If supply remains the same… • An increase in demand will increase the equilibrium price. • A decrease in demand will lower equilibrium price. • Example: Ironic, hipster t-shirts

Increase in Demand Curve • A new demand curve changes the equilibrium price. P2 P1

Decrease in Demand Curve • A new demand curve changes the equilibrium price. P1 P2

What if both Demand and Supply Increase (or Decrease)? • Housing: • increased demand + increased supply = consistent prices

What if both Demand and Supply Increase (or Decrease)? P1 P2