Download

1 / 15

150 likes | 504 Vues

Weathering the Storm of Home Foreclosure Session II.12: Pre and Post-Investment Strategies for Homeownership: Foreclosure Prevention (Source: Number of foreclosure filings taken from statistics provided by North Carolina Administrative Office of the Courts) Threats to Homeownership:

E N D

Weathering the Storm of Home Foreclosure Session II.12: Pre and Post-Investment Strategies for Homeownership: Foreclosure Prevention

(Source: Number of foreclosure filings taken from statistics provided by North Carolina Administrative Office of the Courts)

Threats to Homeownership: • High Cost Mortgage • Too Much Home • Track Homes Offered by One Builder • High Maintenance Homes • Home Equity Theft • Un-educated Home Buyer • Job/Income Loss & Poor Health

High Cost Mortgage: • Adjustable/Variable Rates • Less Than 30 Years • High Interest Rates • Discount Points • Junk Fees • High Debt to Income Ratios • Pre-Payment Penalties • Insurance Packing • Unsigned Good Faith Statements Place Restrictions on the 1st Mortgage Product !

Affordable Monthly Payments Too Much Home Know Your Supply & Demand Soft-Second to Make Home More Affordable NOT to Buy More Expensive Home Burdensome Mortgage Payment

Problems with the Large Tract National and Regional Builders • The Builder Controls all the Players • Realtor • Lender • Attorney • Non-Sustainable Financing • Great Expectations • Bait & Switch • Early Homebuyers at Great Risk • Foreclosures Lead to Depressed Values • Renters Displace Homeowners • No or Weak Homeowners Association

LotsofHomes Inc. $6,000 closing cost paid Presents the Newest Mega Neighborhood “Large Tract Village” Chose your free Appliance Upgrade Today Homes Starting at $99,999 Interest Rates as Low as 2.5%* Be sure to visit our award winning Home Design Studio Prices, terms, and offer are subject to change without notice and valid on select home sites with financing by Lotsof$ Mortgage Company only. See on site sales consultant for details builder paid closing cost. Designer kitchen appliance upgrade available for a limited time only, subject to change without notice. Actual appliances may vary from photos. * Must use LotsofLaw real estate Attorneys, must qualify for lowest rate and the 2.5% rate is for the 1st year, the second year it is 4.5% and caps at 6.5% the third year. The APR is 7.75% Must also use LotsofRealty Real Estate Company. No outside Realtors welcome.

Prices, terms, and offer are subject to change without notice and valid on select home sites with financing by Lotsof$ Mortgage Company only. See on site sales consultant for details builder paid closing cost. Designer kitchen appliance upgrade available for a limited time only, subject to change without notice. Actual appliances may vary from photos. * Must use LotsofLaw real estate Attorneys, must qualify for lowest rate and the 2.5% rate is for the 1st year, the second year it is 4.5% and caps at 6.5% the third year. The APR is 7.75% Must also use LotsofRealty Real Estate Company. No outside Realtors welcome.

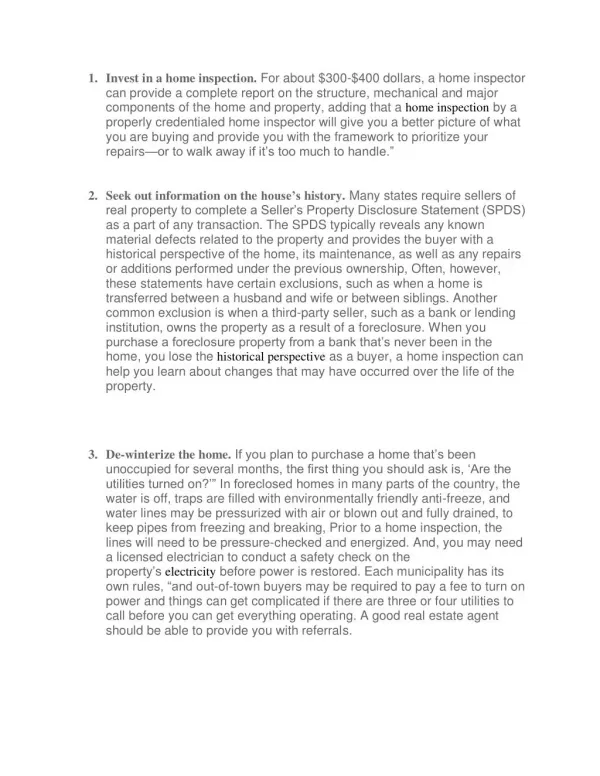

Beware of the Fixer Upper Avoid High Maintenance Homes • Professional Home Inspections • Lead Awareness (Pre 1978) • Beyond Minimum Standards • Home Warranties • Mold/Radon/Asbestos • New vs. Existing • Energy Efficient

The Home Equity Thief Protection Through Long Term Soft Second Mortgages Grants Provide No Protection Loans Requires Loan Subordination Or Loan Payoff

The Role of Realtors & Lenders Seriousness of Offers to Purchase What I Qualify For, I Cannot Afford Why they call it a “Good Faith Estimate” Understanding the Closing Documents How to operate items in the home The Basics of Home Maintenance Who to call when You can’t make the Monthly Payment Pre Homeownership Training Post Homeownership Training Educating the Homebuyer

Post HomeownershipEscrow Incentive Program • $300 Escrow Account at Closing from Buyer • Meet with Counselor 6-12 Months after Purchase • Pull and Review Credit Report • Inspect Home for Maintenance Issues • If Homeowner participates in one on one session with Counselor and Home Maintenance is Acceptable the Homeowner receives $250 of $300 back. The balance of $50 is retained by Center for Home Ownership. • Homeowner has up to 18 months to come into compliance • If compliance is not met within 18 month period the entire $300 is kept by the Center for Homeownership

Obstacles to Helping Homebuyers: • Psychological Factors: • Denial • Fear • Shame • Re-Active as Opposed to Pro-Active • Scam Mortgage/We Buy Homes/Companies • No Early Warning System

Loss Mitigation • NCHFA Pilot Home Foreclosure Protection Program • NCHFA Mortgage Assistance Program under MRB Program • FHA Programs