Download

1 / 10

100 likes | 296 Vues

Product and Service Costing. Managerial Accounting and Cost Management Product costs are used for planning, control, directing, and management decision making. Financial Accounting Product costs are used to value inventory and to compute cost of goods sold. Manufacturing overhead (OH)

E N D

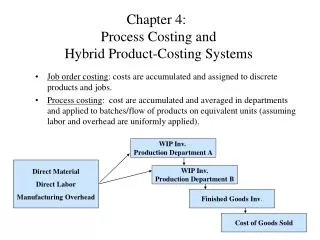

Product and Service Costing Managerial Accounting and Cost Management Product costs are used for planning, control, directing, and management decision making. Financial Accounting Product costs are used to value inventory and to compute cost ofgoods sold.

Manufacturingoverhead (OH) Applied to eachjob using apredeterminedrate Accumulating Costs in aJob-Order Costing System Directmaterials Traced directly to each job THE JOB Traced directly to each job Direct labor

Budgeted manufacturing overhead cost POHR = Budgeted amount of cost driver (or activity base) Manufacturing Overhead Costs Overhead is applied to jobs using a predetermined overhead rate (POHR) based on estimates made at the beginning of the accounting period. Overhead applied = POHR × Actual activity Based on estimates, anddetermined before the period begins Actual amount of the allocation base, such as direct labor hours, incurred during the period

Job Cost Sheets Job Cost Sheets Job Cost Sheets Job-Cost Records Manufacturing Overhead Account Job-Order CostingDocument Flow Summary The materials requisition indicates the cost of direct materialto charge tojobsand the cost of indirect materialto charge to overhead. Direct materials Materials Ledger Cards Materials Ledger Cards Materials Ledger Cards MaterialsRequisition Indirect materials

Job Cost Sheets Job Cost Sheets Job Cost Sheets Job-Cost Records Manufacturing Overhead Account Job-Order CostingDocument Flow Summary Direct Labor Employee time tickets indicate the cost of direct laborto charge tojobsand the costofindirect laborto charge to overhead. Employee Time Ticket Employee Time Ticket Employee Time Ticket Employee Time Ticket Indirect Labor

Job-Order CostingDocument Flow Summary IndirectLabor EmployeeTime Ticket Overhead AppliedwithPOHR OtherActual OHCharges Manufacturing Overhead Account Job-Cost Records MaterialsRequisition IndirectMaterial

The Concept of Activity-Based Costing (ABC) Activity-Based Costing Departmental Overhead Rates Level of Complexity Plantwide Overhead Rate Overhead Allocation

Activity-Based Costing In the ABC method, we recognize that many activities within a department drive overhead costs.

Assigning Costs to Activity Centers Assign costs to the activity centers where they are accumulated while waiting to be applied to products.

Assign costs from the activity center to the product using appropriate cost drivers. When selecting a cost driver consider: The ease of obtaining data. The degree to which the cost driver measures actual consumption by products. Selecting Cost Drivers