Download

1 / 31

310 likes | 319 Vues

MODULE 34 Inflation and Unemployment: The Phillips Curve. What the Phillips curve is and the nature of the short-run trade-off between inflation and unemployment Why there is no long-run trade-off between inflation and unemployment

E N D

What the Phillips curve is and the nature of the short-run trade-off between inflation and unemployment • Why there is no long-run trade-off between inflation and unemployment • Why expansionary policies are limited due to the effects of expected inflation • Why even moderate levels of inflation can be hard to end • Why deflation is a problem for economic policy and leads policy makers to prefer a low but positive inflation rate

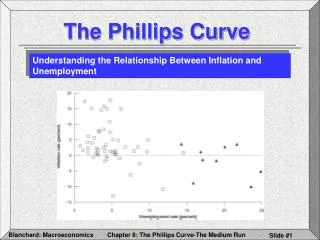

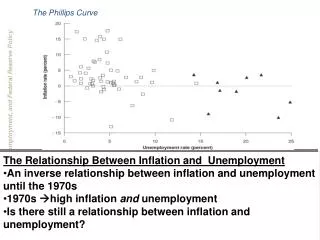

Short-run Phillips Curve • The short-run Phillips curve is the negative short-run relationship between the unemployment rate and the inflation rate. • The concept was introduced by a New Zealand-born economist Alban W. H. Phillips.

The Short-Run Phillips Curve Inflation rate When the unemployment rate is low, inflation is high. 0 When the unemployment rate is high, inflation is low. Unemployment rate

A negative supply shock shifts SRPC up. SRPC 1 A positive supply shock shifts SRPC down. SRPC 2 The Short-Run Phillips Curve and Supply Shocks Inflation rate 0 Unemployment rate SRPC 0

Inflation Expectations and the Short-Run Phillips Curve • The expected rate of inflation is the rate that employers and workers expect in the near future. • Expectations about future inflation directly affect the present inflation rate. • Higher expected inflation causes workers to desire higher wages, an increase in expected inflation shifts the short-run Phillips curve.

Expected Inflation and the Short-Run Phillips Curve Inflation rate 6% 5 SRPC shifts up by the amount of the increase in expected inflation. 4 3 2 1 SRPC 2 0 3 4 5 6 7 8% Unemployment rate –1 –2 SRPC 0 –3

The NAIRU and the Long-Run Phillips Curve Inflation rate 8% 7 C 6 5 B E 4 4 3 A E 2 SRPC 2 4 1 E SRPC 2 0 0 3 4 5 6 7 8% Unemployment rate –1 Nonaccelerating inflation rate of unemployment, NAIRU SRPC –2 0 –3

Inflation and Unemployment in the Long Run • The nonaccelerating inflation rate of unemployment, or NAIRU, is the unemployment rate at which inflation does not change over time. • NAIRU = Natural Unemployment Rate

Cost of Disinflation • Once inflation has become embedded in expectations, getting inflation back down can be difficult because disinflation can be very costly. • This requires high levels of unemployment and the sacrifice of large amounts of aggregate output.

Deflation • Irving Fisher analyzed great depression and claimed that the effects of deflation on borrowers and lenders can worsen an economic slump. • Deflation imposes a burden on borrower: lender wins and borrowers looses. • Investment by borrowers decreases more than the increases in investment by lenders. • So, deflation reduces aggregated demand deepening the slump. • This creates a vicious circle to further depress the economy.

Deflation Liquidity trap and Limitation of Monetary Policy: • There is a zero bound on the nominal interest rate: it cannot go below zero. • This zero bound can limit the effectiveness of monetary policy. • Monetary policy can’t be used because nominal interest rates cannot fall below the zero bound. • This liquidity trap can occur whenever there is a sharp reduction in demand for loanable funds. • A liquidity trap is when monetary policy is unable to stimulate an economy because nominal interest rates are up against the zero bound.

At a given point in time, there is a downward-sloping relationship between unemployment and inflation known as the short-run Phillips curve. This curve is shifted by changes in the expected rate of inflation. • The long-run Phillips curve, which shows the relationship between unemployment and inflation once expectations have had time to adjust, is vertical. It defines the non-accelerating inflation rate of unemployment, or NAIRU, which is equal to the natural rate of unemployment. • Once inflation has become embedded in expectations, getting inflation back down can be difficult since disinflation can be very costly.

Deflation can lead to debt deflation, in which a rising real burden of outstanding debt intensifies an economic downturn. • Interest rates are more likely to run up against the zero bound in an economy experiencing deflation. When this happens, the economy enters a liquidity trap, rendering conventional monetary policy ineffective.

Why classical macroeconomics wasn’t adequate for the problems posed by the Great Depression • How Keynes and the experience of the Great Depression legitimized macroeconomic policy activism • What monetarism is and its views about the limits of discretionary monetary policy • How challenges led to a revision of Keynesian ideas and the emergence of new classical macroeconomics

Classical Macroeconomics • Classical macroeconomics asserted that monetary policy affected only the aggregate price level, not aggregate output. • Classical macroeconomics asserted that the short run was unimportant. • According to the classical model, prices are flexible, making the aggregate supply curve vertical even in the short run.

Classical Macroeconomics • + M equal, proportional +P, with no effect on aggregate output/GDP. • Increases in the money supply lead to inflation, and that’s all. • No need for fiscal and monetary policy

The Great Depression and the Keynesian Revolution • In 1936, Keynes presented his analysis of the Great Depression—his explanation of what was wrong with the economy’s alternator—in a book titled The General Theory of Employment, Interest, and Money. • The school of thought that emerged out of the works of John Maynard Keynes is known as Keynesian economics. • According to Keynesian economics: • Changes in aggregate demand changes GDP. • Government intervention (i.e., fiscal and monetary policy) is needed.

Challenges to Keynesian Economics • Mainly put forth by Milton Friedman and his co-author Anna Schwartz. • Monetarism asserted that GDP will grow steadily if the money supply grows steadily. • Monetarism was influential for a time, but was eventually rejected by many macroeconomists.

Fiscal Policy with a Fixed Money Supply Figure Caption: Figure 35.2: Fiscal Policy with a Fixed Money Supply In panel (a) an expansionary fiscal policy shifts the AD curve rightward, driving up both the aggregate price level and aggregate output. However, this leads to an increase in the demand for money. If the money supply is held fixed, as in panel (b), the increase in money demand drives up the interest rate, reducing investment spending and offsetting part of the fiscal expansion. So the shift of the AD curve is less than it would otherwise be: fiscal policy becomes less effective when the money supply is held fixed.

Monetarism • Friedman didn’t favor activist monetary policy due to the problem of time lags. • He argues the central bank should follow a rule, called monetary policy rule. • A monetary policy rule is a formula that determines the central bank’s actions. • The velocity of money is the ratio of nominal GDP to the money supply. • The velocity equation: M × V = P × Y • https://www.youtube.com/watch?v=q59tZKP0HME

Monetarism • Monetarists believed that V was stable, so they believed that if the Federal Reserve kept M on a steady growth path, nominal GDP would also grow steadily.

Classical macroeconomics asserted that monetary policy affected only the aggregate price level, not aggregate output, and that the short run was unimportant. • Keynesian economics attributed the business cycle to shifts of the aggregate demand curve, often the result of changes in business confidence. Keynesian economics also offered a rationale for macroeconomic policy activism. • Monetarism is a doctrine that called for a monetary policy rule as opposed to discretionary monetary policy, and which argued that GDP would grow steadily if the money supply grew steadily.

The natural rate hypothesis says that the unemployment rate must be high enough to keep expected inflation and actual inflation equal. • Fears of a political business cycle led to a consensus that monetary policy should be insulated from politics. • Rational expectations suggests that even in the short run there might not be a trade-off between inflation and unemployment because expected inflation would change immediately in the face of expected changes in policy.

Real business cycle theory claims that changes in the rate of growth of total factor productivity are the main cause of business cycles. • New Keynesian economics argues that market imperfections can lead to price stickiness, so that changes in aggregate demand have effects on aggregate output after all.