Download

1 / 19

190 likes | 514 Vues

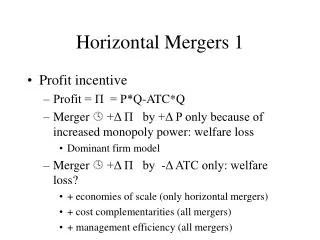

The Law and Economics of Horizontal Mergers. Incentives to Merge. Merger to attain monopoly Merger for Improved efficiency Takeovers. The Williamson Tradeoff. $/Q. P 2. B. AC 1. P 1. A. AC 2. D. Q 2. Q 1. Q. The Economic effects of Mergers. Theoretical Considerations

E N D

Incentives to Merge • Merger to attain monopoly • Merger for Improved efficiency • Takeovers

The Williamson Tradeoff $/Q P2 B AC1 P1 A AC2 D Q2 Q1 Q

The Economic effects of Mergers • Theoretical Considerations • Dominant Firm-Competitive Fringe • Cournot • Bertrand • Empirical Analyses • Event analyses (Eckbo; Prager) • Merger Specific Analyses (Northwest-Republic)

Implications of DF-CF Model for Mergers • If a dominant firm mergers with a competitive fringe firm, market power and price will rise (ceteris paribus) • The magnitude of market power increases depend on standard DF-CF Market power factors (concentration; fringe SS elasticity, market DD elasticity) • Without barriers to entry, no MP increase • Efficiency gains may offset market power effects

Northwest/Republic Merger Markup Relative to industry average prices (%) 40 NW or Rep NW + REP 30 20 NW or Republic + Other 10 NW +Rep + Other 1987 1985 1986

Merger Policy in Practice • Legal foundation of merger policy • Clayton Act, Section 7 • Hart Scott Rodino • Antitrust enforcement • Judicial Treatment of mergers

The Clayton Act, Section 7 That no corporation engaged in commerce shall acquire, directly or indirectly, the whole or any part…of another corporation also engaged in commerce, where in any line of commerce in any section of the country, the effect of such acquisition may be substantially to lessen competition or to tend to create a monopoly. Language matters…. * in any line of commerce in any section of the country *the effect…may be to lessen competition or tend to create

Hart Scott Rodino • Requires pre-notification of intent to merger be filed with both the Federal Trade Commission and the Department of Justice, Antitrust Division • The relevant antitrust agency has 30 days to green light or issue a “second request” • Second requests typical involve large detailed filing • Once complete DOJ/FTC has 20 days

2010 Merger Guidelines • “The unifying theme of the Guidelines is that mergers should not be permitted to create, enhance or entrench market power or to facilitate its exercise.”

The DOJ/FTC Merger Guidelines • Market Definition • Market concentration • Entry Conditions • Other Competitive Indicators • Merger-induced efficiencies

Market Definition • Begin with a small geographic and product definition. • Could a hypothetical monopolist raise prices by a small but significant and non-transitory amount? • Yes • No • (dd-side product, dd-side geographic, ss-side product, ss-side geographic substitutability)

Market Concentration • Herfindahl-Hirschmann Index • HHI = Σ S2i • 0<HHI<10,000 • (Post merger) HHI < 1500 - unconcentrated • 1500 <HHI< 2500 -- moderately concentrated • if ΔHHI <100 • if ΔHHI >100 • 2500 <HHI -- highly concentrated • If 100< ΔHHI <200 “potentially raise significant competitive concerns” • if ΔHHI >200 “presumed to be likely to enhance market power”

Entry conditions • Prior taxonomy: • Uncommited Entry • Committed entry • Entry requiring significant sunk costs • “The Agencies will consider the actual history of entry into the relevant market and give substantial weight to this evidence.” • Timely (“former language” w/i two years; now “rapid enough…”) • Likely (profitable at pre-merger prices), and • Sufficient (enough to discipline prices)

Other Competitive Indicators • Would merger facilitate collusion? • Facilitate monitoring of cheating • Promote ability to punish cheaters • Factors: e.g., product homogeneity; are transactions prices “visible”; are demand and cost changing rapidly; maverick firm

Merger-Induced Efficiencies • Consistent with Williamson Trade-off • Only considered if merger is only means of achieving efficiencies • Consider the case of efficiencies to gain economies of scale...

Brown Shoe Company v. U.S. • Merger of Brown and Kinney shoes (retail) • market: • product markets: mens, womens, childrens’ • geographic : any city over 10,000 • “We cannot avoid the mandate of Congress that tendencies toward concentration in industry are to be curbed in their incipiency”

FTC v. Coca-Cola • Coca-Cola - Dr. Pepper, Pepsi - 7-Up announce merger plans • FTC issues preliminary injunction • Coca-Cola-Dr. Pepper challenge in court • Critical issue: Market definition • FTC - carbonated soft drinks (pricing decisions of executives) • Coca-Cola - all potable liquids sold in North America (Lake Erie defense)

FTC v. Coca-Cola (cont.) • Barriers to entry • sunk costs of entry (brand name awareness) • requirements for distribution network • limited buttons on “Coke Machines” • Anticipated anticompetitive effects • Third party bottler problem • Court’s finding “the acquisition totally lacks any apparent redeeming feature.”