Download

1 / 15

150 likes | 154 Vues

This discussion explores the reasons why private equity funds continue to hold onto public equity after initial public offerings (IPOs), highlighting conflicts of interest and potential economic benefits.

E N D

Discussion: Long goodbyes: Why do privateequity funds hold onto public equityafter IPOs? By T. Jenkinson, H. Jones, C. Rauch and R. Stuecke Discussion by Jens Martin, University of Amsterdam

Basic Question • How does Private Equity exit? • Traditional argument: • Sale to strategic buyer • Sale to financial buyer • IPO • Very interesting question • Exhibits another facet of moral hazard in the PE sector

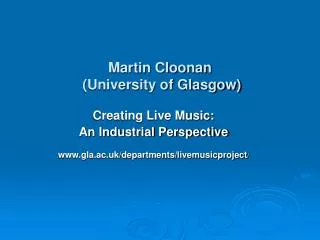

Exit choices of PE for a portfolio company IPO Private Firm Direct acquisition

Exit choices of PE for a portfolio company Acquisition IPO Selling shares of the public company Private Firm Delisting Direct acquisition

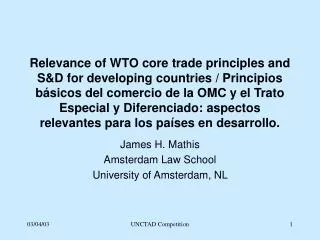

Conflict of interest: Timeline of private equity funds commitments by investors cash flows back to investors 1 year 2 years 10 years marketing investment exit extension GP earns management fee on committed capital GP earns management fee on invested capital follow-on fund GP starts marketing of a new fund

Other conflict of interests: • Where in the fund life do we see which behavior? • Grandstanding to market new funds? IPO valuation of particular importance at this stage? • Pressure to sell at the end of the fund lifecycle? • Give the long time to exit, are you more likely to IPO early on in the fund lifecycle?

Other conflict of interests: • When are other investors leaving the company? Did they leave partly before? Do all partners, i.e. in a club deal, leave at the same time? What happens to co-investments? • Do some fund actually increase their holding? • What’s the value of reputation as it may be a bad signal for future investors as returns are below expectations? • Is it a way to lock in-IRR? I.e. sell a stake at the IPO to lock in IRR, then selling later will not affect it greatly • Calculate difference in carry if they would have sold at IPO versus at the actual selling point to illustrate the economic benefit. What is the economic benefit compared to the funds total fees?

General comments • What type of companies / industries? Ritter (2012) assumes that small companies have less incentive to do a IPO? • Time trends? We see a decline in IPOs over the long run. • Do we see short term patterns? So a month prior to see do we see an increase? So a quasi-market timing in the short run? • Returns: different for the M&A sample? • What are the other deals a fund has?

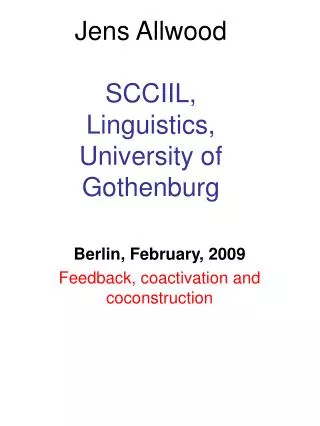

At the IPO • Do we see differences in lockup structures? You report that 13% do actually sell in the lockup period • Narrative of Behavioral Issues: what would be a comparable sell be worth in the market: thus, is the market open, is it at the IPO more lucrative to do an IPO? Look closer at market conditions (as Cao 2011) IPO Private Firm Direct acquisition

Returns • The returns you show during the holding period seem to be very low • Other literature, reported a much higher return for IPO exit. That means that returns have to be impressively high prior to exit. So most of the return seem sto be locked in at the IPO. Can you observe this? Do you see a pattern? Source: Degeorge et al, 2016, On Secondary Buyouts

Methodology: which model do you use? • As stocks are listed, you could use more advance asset pricing models: DGTW adjusted returns, etc.

Methodology, cont. • %-Days Stock Price>IPO Price (IPO to Exit)=>Potentially problematic, better take a Cox Proportional Hazard model to measure the likelihood in a given time (see Genesove, D., and C. Mayer. "Loss aversion and seller behavior: Evidence from the housing market." The quarterly journal of economics 116.4 (2001): 1233-1260. • Do we see different selling patterns (number of sells etc.) in downtrends versus uptrends? Do they keep all the shares? Is duration the right variable? • What role is market liquidity playing? • “Both measured from IPO to final share sale”do we see a difference if we look at the largest sale? Do we see sometimes just a toke piece left?

Split funds along the carry for a more nuanced picture and to account for non-linearity Funds deep in the carry: Carry might not be affected, So they have am incentive for such behavior 2. Funds just above carry threshold: Funds might be reluctant to risk a market downturn and not being in the carry anymore 3. Funds just below the vary: Funds might try to gamble on a market uptrend and so getting above the threshold. 4. Funds way below the threshold: These fund get their money mostly through their 2% on assets invested. So they have an incentive to hold it longer

Very interesting paper with a very relevant research question!