Download

1 / 39

430 likes | 1.09k Vues

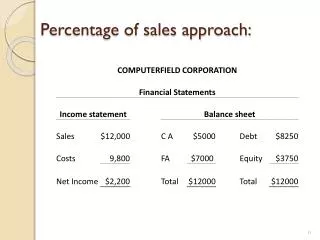

Percentage of Completion Example. Paterno Construction receives a contract for $1.5 million Renovation to Beaver Stadium Through 1997, 1998, and 1999.

E N D

Percentage of Completion Example Paterno Construction receives a contract for $1.5 million Renovation to Beaver Stadium Through 1997, 1998, and 1999

When materials are purchased and costs are incurred, we transfer the balance to a work-in-process inventory account called Construction-in-Progress Basic Journal Entries for Transactions 1997 Costs Incurred: $350,000

Constr In Progr Inv. 350,000 Transferring costs to CIP account. Basic Journal Entries for Transactions 1997 Costs Incurred: $350,000 The Journal Entry to do this transfer might look like:

Basic Journal Entries for Transactions 1997 Costs Incurred: $350,000 The Journal Entry to do this transfer might look like: Constr In Progr Inv. 350,000 Materials Inv. 200,000 Wages Payable 80,000 Cash 70,000 Actual costs incurred in the year.

T-Account Summary CIP Inv 350,000

Basic Journal Entries for Transactions When the company bills for work in progress, it records an accounts receivable for the amount of the billing and a corresponding contra-asset account called Billings on Construction. Billings on Construction is a contra-asset account because it reduces the amount of Construction-in-Progress inventory that the firm can claim is theirs. In other words, it is as if the firm is transferring the rights to ownership of a portion of Construction-in-Progress inventory in exchange for an increase in accounts receivable.

Basic Journal Entries for Transactions Example: On Nov. 30, the company mails a bill for $300,000 . 11/30 Accounts Rec. 300,000 Billings on Constr 300,000

Billings on Constr 300,000 T-Account Summary CIP Inv 350,000 1997 Balance Sheet Representation: Assets: Constr in Prog Inv 350,000 Less: Billings on Construct (300,000) Net CIP Inventory 50,000

Basic Journal Entries for Transactions When the company actually receives payment on the recent billing, it simply records the cash in exchange for the accounts receivable. Example: On Dec. 10, the company receives cash for the bill: 12/10 Cash 300,000 Accounts Rec. 300,000

Computing Revenue under Percentage of Completion Start with 1997 data for costs incurred and estimated total completion costs.

Computing Revenue under Percentage of Completion 1997 Costs Incurred to-date: $350,000 Estimated Total Costs: $1,350,000 Percent Complete = 350,000/1,350,000 = 25.926% Revenue = Percent Complete x Total Revenue for Project - Prior Revenue Recognized Revenue1997 = (0.25926 x $1,500,000) - $0 = $388,890

Computing Revenue under Percentage of Completion Now, compute for 1998. Assume expected completion costs increase to $1,360,000 due to budget overruns.

Note that this is cumulative (this includes the $350,000 costs incurred in 1997 and an additional $550,000 incurred in 1998). Computing Revenue under Percentage of Completion 1998 Costs Incurred to-date: $900,000 Estimated Total Costs: $1,360,000 Percent Complete = 900,000/1,360,000 = 66.176% Revenue = Percent Complete x Total Revenue for Project - Prior Revenue Recognized Revenue1998 = (0.66176 x $1,500,000) - $388,890 = $603,750

Computing Revenue under Percentage of Completion Now, compute for 1999. Assume actual completion costs increase to $1,365,000 due to budget overruns.

Computing Revenue under Percentage of Completion 1999 Costs Incurred to-date: $1,365,000 Estimated Total Costs: $1,365,000 Percent Complete = 1,365,000/1,365,000 = 100% Revenue = Percent Complete x Total Revenue for Project - Prior Revenue Recognized Revenue1999 = (1 x $1,500,000) - $388,890 - $603,750 = $507,360

Annual Journal Entries to Record Revenue and Gross Profit 1997 End-of-Year Journal Entry: Construction Expense 350,000 Construction Revenue 388,890

Gross profit goes to CIP Inventory Account Annual Journal Entries to Record Revenue and Gross Profit 1997 End-of-Year Journal Entry: Construction Expense 350,000 Constr In Prog Inv 38,890 Construction Revenue 388,890

1997 T-Account Summary CIP Inv Billings on Constr 350,000 38,890 300,000 Actual Costs Gross Profit

1997 T-Account Summary CIP Inv Billings on Constr 350,000 38,890 300,000 300,000 1997 Balance 388,890

Annual Journal Entries to Record Revenue and Gross Profit 1998 End-of-Year Journal Entry: Construction Expense 550,000 Construction Revenue 603,750

Annual Journal Entries to Record Revenue and Gross Profit 1998 End-of-Year Journal Entry: Construction Expense 550,000 Constr In Prog Inv 53,750 Construction Revenue 603,750

Annual Journal Entries to Record Revenue and Gross Profit 1999 End-of-Year Journal Entry: Construction Expense 465,000 Constr In Prog Inv 42,360 Construction Revenue 507,360

End of Project T-Account Summary CIP Inv Billings on Constr $1,500,000 $1,500,000

This includes all costs incurred through the project plus all gross profit on the project. This is the amount we will have billed the client through the project life. End of Project T-Account Summary CIP Inv Billings on Constr $1,500,000 $1,500,000

End of Project T-Account Summary CIP Inv Billings on Constr $1,500,000 $1,500,000 Closing Journal Entry (to zero out accounts): Billings on Constr 1,500,000 CIP Inv 1,500,000

Losses on Long-Term Contracts • There are two situations for losses: • Loss only in current period • When current year’s expenses > current year’s revenues. But the total project will still be profitable. • Unprofitable total contract • When new estimates of total contract costs > expected total revenues.

Losses on Long-Term Contracts Loss only in current period Example: 1998 expected total costs increase to $1,450,000 (Note that the total contract is still profitable since we will collect $1,500,000)

900,000 / 1,450,000 = 62% 0.62 x 1,500,000 = $931,035 – 388,890 = $542,145 Losses on Long-Term Contracts Loss only in current period Example: 1998 expected total costs increase to $1,450,000

Losses on Long-Term Contracts Loss only in current period Example: 1998 expected total costs increase to $1,450,000 Notice costs incurred > Current period revenue 550,000 542,145

Losses on Long-Term Contracts Loss only in current period Notice costs incurred > Current period revenue 550,000 542,145 Journal entry: Construction Expenses 550,000 CIP Inventory (Loss) 7,855 Construction Revenue 542,145

Losses on Long-Term Contracts Unprofitable Total Contract Example: 1998 expected total costs increase to $1,600,000 Note that the total contract is no longer profitable since we will collect only $1,500,000. So, we anticipate a $100,000 loss. We must recognize this anticipated loss on the entire project in the year we first discover the expected loss (in this case, 1998). To do this, we do the following: 1. Compute the revenue for the year using same method as before. 2. Reverse any prior recorded profits and record the anticipated loss.

900,000 / 1,600,000 = 56.25% 0.5625 x 1,500,000 = $843,750 – 388,890 = $454,860 Note also that we recorded $388,890 - $350,000 = $38,890 Gross Profit in 1997. Losses on Long-Term Contracts Unprofitable Total Contract Example: 1998 expected total costs increase to $1,600,000 Compute Revenue for the Year

Record the $100,000 loss + reverse the 1997 Gross Profit Record the revenue for the year Losses on Long-Term Contracts Unprofitable Total Contract Example: 1998 expected total costs increase to $1,600,000 1998 Journal entry: Construction Exps 593,750 CIP Inventory (loss) 138,890 Construction Revenue 454,860