Download

1 / 31

310 likes | 358 Vues

Dealmakers’ Workshop: Health Care Services Investing. February 26, 2013. Sponsored by. @ACGPhilly with #ACGPHL. The fiscal problems in the U.S. Barbara Shander Partner, Morgan Lewis and Program Chair, ACG Philadelphia. Welcome & Introductions. 2. #ACGPHL.

E N D

Dealmakers’ Workshop:Health Care Services Investing February 26, 2013 Sponsored by @ACGPhilly with #ACGPHL

The fiscal problems in the U.S. Barbara ShanderPartner, Morgan Lewis and Program Chair, ACG Philadelphia Welcome & Introductions 2 #ACGPHL

The fiscal problems in the U.S. Glenn BarenbaumSenior Manager- Transaction Advisory ServicesErnst & Young 3 #ACGPHL

DealMaker Panelists Tim Johnson, England & Company Russell Pederson, Sellers DorseyDan Shoenholz, Ernst & Young TomSchneider, Gemino Healthcare FinanceMike Gaffney, EDG Partners Moderator: Steve Economou, Curtis Financial #ACGPHL

The fiscal problems in the U.S. Steve EconomouManager DirectorCurtis Financial Group, LLC 5 #ACGPHL

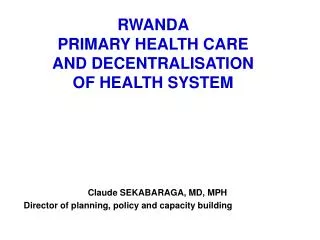

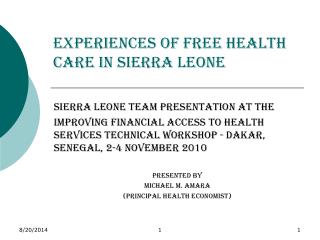

Health Care Services Mergers & AcquisitionsTotal Announced Transactions By Year

The fiscal problems in the U.S. Tim JohnsonManager DirectorEngland & Company 7 #ACGPHL

England & Company • England & Company – middle market focused investment bank • Offices in New York and Washington DC • Our principals apply vast transactional experience and deep industry knowledge to deliver exceptional results for our clients • Our investment bankers have been involved as agent, principal or advisor in: • Dozens of M&A transactions worth more than $5 billion in total consideration • More than 100 private placements aggregating over $10 billion in capital raised • We primarily focus our resources on the following industries: • Healthcare Services & IT (Laboratory services a key focus area) • Software & Information Technology • Energy & Infrastructure Technology

England & Company – Recent Healthcare Transactions has acquired has acquired has acquired has been acquired by has completed a recapitalization led by has led the buyout of has completed a recapitalization and management buyout led by has been acquired by has been acquired by

Why Invest in Healthcare? • Large and Rapidly Growing Market • Favorable demographic trends (aging population) • ACA (“Obamacare”) projected to cover additional ~30 million • Highly fragmented sub-sectors with natural acquirers • Advances in IT can level the playing field for smaller companies • High-level Trends / Issues: • Emphasis on prevention • Continued reimbursement pressures • Shift towards outcomes based-payments • Pushing care to the lowest cost provider

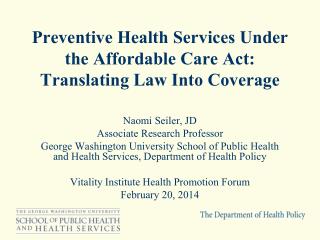

US Healthcare Spending National Health Expenditure 2005 – 2021 ($Billions) • $ 2.8 trillion market (17%+ of the US economy) • Healthcare spending projected to grow ~6% per year over the next decade Source: CMS

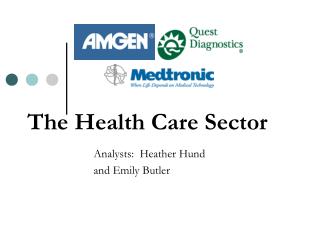

Aging US Population US Population Over 65 Source: US Census Bureau

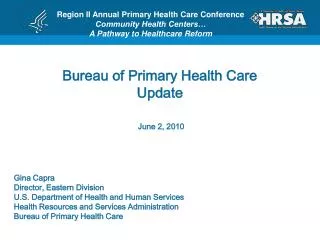

US Healthcare Spending by Sector US Health Care Spending by Sector (2011) Source: CMS

The fiscal problems in the U.S. Russell PedersonManaging PrincipalSellers Dorsey 14 #ACGPHL

Role of Government in Healthcare • Government is the principal driver of the healthcare industry – As purchaser of health plans, payor of providers, financer of coverage, and regulator • Public sector is largest payor of: • Health insurance premiums • Hospital care • Drugs, biologics, diagnostics, devices, and supplies • Physician, clinics, and other ambulatory care • Nursing facilities, home health, and other long-term services and supports • In many sub-segments – biologics, diagnostics, long-term care – the public sector is a monopsony • The government’s market influence goes far beyond reimbursement. Federal and state policy drive virtually every aspect of the industry: • Pricing, coverage and benefit design, business arrangements, sales and marketing, operations, clinical care, innovation, and technology • Affects every player – providers, manufacturers, and insurers • Medicare and Medicaid policies – coverage decisions, reimbursement methods, performance reporting, and care delivery expectations – drive the marketplace. Private payors typically follow the government’s lead. • State and local government spend more on health care than private employers

Opportunities • Over $1.8 trillion in new federal and state-funded premium revenue in first 10 years (2014-2023). • Health Insurance Exchanges: • New, complex, highly regulated marketplace • Will replace 80%+ of current individual insurance market • Could replace over 50% of small business market • Significant interaction with Medicaid market • Medicaid expansion: • ACA Medicaid expansion, streamlined eligibility, woodwork effect, and crowd out will increase Medicaid enrollment by 20 million+ • In revenue, Medicaid health plan market will exceed size of Medicare Advantage market • Medicare-Medicaid integration for dual eligibles: • $350 billion market – only 15% of now under risk • Huge opportunity for health plans. • Additional opportunities for companies in care management / IT spaces. • Information Technology / Information Services: • States primed for IT transformation • Traditional service providers struggling to adapt • Managed long-term care • Acquisition non-profit players (health plans and health systems) and conversion to for-profit status

Risks • Medicare and Medicaid are fiscally unsustainable: • Further budget cuts are inevitable • High risk of technical, budget driven changes with major implications for specific sectors • Significant price competition in Exchange market • Premium sticker shock under adjusted community rating • Complexity and uncertainty of ACA changes: • ACA is unprecedented in size, scope, and complexity. • No precedents, many scenarios • “Cognitive risk” where decision makers freeze and miss opportunities • Requires nimble, policy-savvy strategy • Providers are slow to adapt their business model and operations. Under significant pressure. Lack capabilities, expertise, alignment, data, and capital • Lack of expertise navigating federal and state government and public programs: • Most healthcare businesses remain dangerously unsophisticated • Push back on need to understand complexity, politics • Boards lack experts in public programs • Due diligence more complex, specialized • Most analysts are mile wide and inch deep • Health insurers risk becoming regulated utilities. Low but predictable margins • Compliance risks will increase for all players

Trends • Healthcare cost containment will become top priority. This includes: • Eliminating unnecessary spending, especially preventable events • Accelerated payment reform. New incentives for providers and consumers to reduce costs, reward efficiency. • Fraud and abuse reduction – Continued, expanded • Pricing based on acquisition cost • Strong, intense focus on data and evidence throughout marketplace: • Value of products and services • Decision making • Coverage and reimbursement • Transparency of clinical and economic performance • New framework for reimbursement: • Continued, faster efforts to replace fee-for-service with performance-based reimbursement • Move from volume metric (volume and unit price) to value (outcomes, quality, net costs) • Fundamental change to financial paradigm for providers. Significant impact on manufacturers • Political gridlock between White House and Congress • Major federal legislative changes will be difficult and rare • Power will shift to federal agencies (CMS, OMB) and States • Policies affecting industry will be made through budgets, rulemaking, waivers, and sub-regulatory guidance

The fiscal problems in the U.S. Dan ShoenholzPartner/PrincipalErnst & Young Commercial Advisory & Healthcare Practice Commercial Due DiligenceHealthcare Considerations 19 #ACGPHL

Introduction • E&Y: Transaction Advisory Services business • Focused Healthcare and Life Sciences professionals • Dedicated Commercial Advisory Services Team – diligence/strategy • Experience working on hundreds of healthcare/life sciences deals

Healthcare: Commercial Diligence Themes • Fragmented/local markets • Multiple stakeholders with evolving decision-making dynamics • Regulation and regulatory change • Funding and reimbursement pressures • Consolidation/integration of business models • Revenue/operational benefits to scale

Industry Backdrop/Key Unique CDD Issues: Providers Driver Unique Commercial Diligence Issues • Risk shifts to providers • Industry consolidation • IT and Services outsourcing • Labor availability • Demographics • Target’s payer mix • Pricing/reimbursement trends • Validation of efficiency potential • Payer concentration in local markets • Threats/opportunities from provider consolidation/”ACOs” • Roll-up opportunities • Current/future propensity to outsource services • Pricing/spending environment • Customer ability to/interest in in-sourcing • Labor pools for qualified professionals • Accreditation requirements • Wage trends • Population trends • Disease incidence/prevalence

Industry Backdrop/Key Unique CDD Issues: Providers Driver Unique Commercial Diligence Issues • Changes in buying power (docs/administrators) • Same store sales/facility-level analysis • Procedure mix/trend • Local market dynamics (competition/physician) • Regulatory changes (federal/state) • Decision-making process within provider networks • Relative significance of key stakeholders • Unit-level performance and trends • Environmental drivers of performance • Pricing and setting sustainability across modality/acuity of treatment • Local market share • Competitive positioning/differentiation • Physician availability and affiliation • New entrants • Medicaid/Medicare pricing and coverage • CON/site approvals

Industry Backdrop/Key Unique CDD Issues: Payers Driver Unique Commercial Diligence Issues • Regulatory changes • HCIT • Consolidation • Local market dynamics (competition/physician) • Business efficiency • Impact of regulations on patient population and reimbursement • Opportunities for new models (ACOs, Health Exchanges) • Opportunities for business models focused around data/ analytics • Competitive differentiation through HCIT • Provider landscape • Opportunities/threats from payer-provider consolidation • Local market share • Effectiveness of provider network • New entrants • MLR/ALR trending and peer comparisons

Health Care CDD Best Practices • Physician and administrator perspective on buying process: understand relative influence, identify key physician influencers • Local (MSA)-level perspective: granular analysis of patient/provider demographics, competition, payer mix, regulations • Location-level analysis: define winning formula and assess ability to replicate • Regulatory perspective (Federal and sometimes state): can determine attractiveness of local market/overall business model • Benefits to scale and ability to achieve it: efficiencies, available targets Begin to assess critical issues pre-LOI, and front-load them in the post-LOI process, to get an early view on valuation in front of deal-killer issues!

The fiscal problems in the U.S. Mike Gaffney Co-Founder & Managing DirectorEDG Partners 26 #ACGPHL

EDG Partners Singular Focus on Healthcare By committing ourselves exclusively to healthcare, EDG offers a well-defined view of the industry, its future, and how companies can excel. In addition, EDG offers relationships built over 65 years of healthcare experience. Operating Experience Having founded and run public and private healthcare companies, EDG appreciates what it means to “make payroll” and navigate the operational challenges of growth. Strategic Partners Because we view an investment as a partnership, EDG offers ourselves as a source of strategic insight. Leveraging EDG’s investment and operating experience, we seek to be thoughtful partners helping as needed but making sure we are not an obstruction to the creativity and leadership occurring within portfolio company’s. 27

Successful Dealmaking in Healthcare Back the Jockey – with an eye on the quality of the Horse Keen eye on big market participants – especially the government – most businesses are price takers Biggest investment risk – significant volatility; tourists Our expectation for the future: Change – Obamacare; Retail Health Insurance; Demographics… Uncertainty – 2000 pages of legislation; 20% of regulations written; significant state level variability… Opportunity – for businesses that create value 28

The fiscal problems in the U.S. Tom SchneiderChief Operating and Credit OfficerGemino Healthcare Finance Lending to Healthcare Service Companies 29 #ACGPHL

Impact of Reimbursement Trends and Healthcare Reform on Provider Financing Needs • Due Diligence Considerations • Management Experience • Regulatory Issues • AR Valuation/Monitoring Changes in Reimbursement • Overpayment Liabilities • QOE Analysis and Clinical Due Diligence • Structuring/Financial Covenants

Upcoming Events Mark Your Calendar acg.org/philadelphiaMarch 21, 2013 March Breakfast: Private Equity & Human Capital April 4, 2013 Young DealMakers’ Happy Hour April 11, 2013 Corporate Executives’ Dinner - Human Capital Integration April 18, 2013 The Role of the Family Office in M&A April 22 - 25, 2013 InterGrowth - Orlando, Fl May 16, 2013 May Breakfast: Annual Lenders’ Panel Discussion #ACGPHL