Download

1 / 29

290 likes | 380 Vues

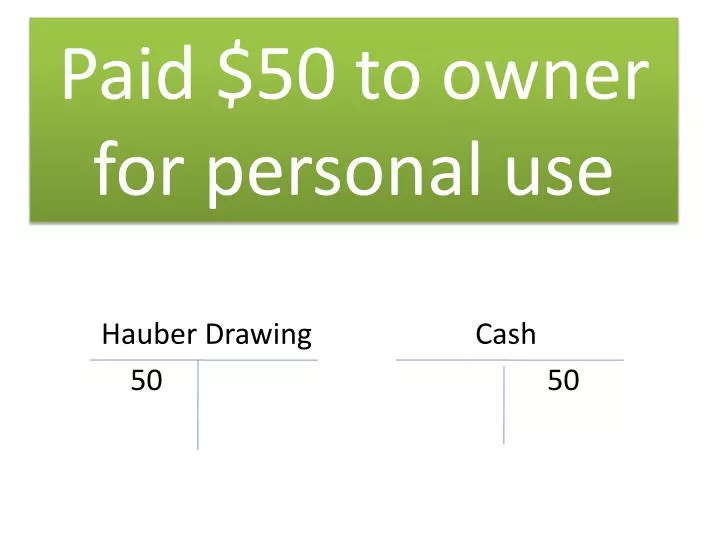

Paid $50 to owner for personal use. Hauber Drawing Cash 50 50. Paid $75 for supplies. Supplies 75. Cash 75. Bought $40 of supplies on account. Supplies 40. Accounts Payable 40. Established $200 petty cash fund. Petty Cash 200.

E N D

Paid $50 to owner for personal use Hauber Drawing Cash 50 50

Paid $75 for supplies Supplies 75 Cash 75

Bought $40 of supplies on account Supplies 40 Accounts Payable 40

Established $200 petty cash fund Petty Cash 200 Cash 200

Adjust supplies by $30 Supplies Expense 30 Supplies 30

Close sales with $2000 balance Sales 2000 Income Summary 2000

Close rent expense with $700 balance Income Summary 700 Rent Expense 700

Close income summary with a net income of $5000 Hauber Capital 5000 Income Summary 5000

Close Hauber drawing with $300 balance • Hauber Capital 300 • Hauber Drawing 300

Unit 2 Purchased $600 worth of merchandise on account Purchases 600 Accounts Payable/Vendor Name 600

Paid cash $650 for merchandise Purchases 650 Cash 650

Returned $400 worth of merchandise on account Accounts Payable 400 • Purchases Returns and Allowance 400

Paid on account ($400) with a discount ($40) AP/Vendor Cash Purchases Discount 360 40 400

Sold merchandise ($1000) on account with tax ($70) AR/Customer Sales Sales Tax Payable 1070 1000 70

Recorded cash and credit card sales ($2000) with tax ($140) Cash Sales Sales Tax Payable 2140 2000 140

Paid cash to replenish petty cash fund: supplies $20 and advertising $25 Supplies Advertising Expense Cash 20 25 45

Granted credit to our customer for merchandise ($300) returned plus tax ($21) Sales Returns and allowance Sales Tax Payable AR/Customer 300 21 321

Received cash on account ($520) with a discount ($20) Cash Sales Discount AR/Customer 500 20 520

Declared a $5000 dividend Dividends 5000 Dividends Payable 5000

Paid previous dividend declared Dividends Payable 5000 Cash 5000

Adjust merchandise inventory that went down by $10,000 Income Summary 10,000 Merchandise Inventory 10,000

Adjust uncollectible accounts by $1200 Uncollectible Accounts Expense 1200 Allowance for Uncollectible 1200

Close purchases discount with a $140 balance Purchases Discount 140 Income Summary 140

Close Sales returns and allowance with $200 balance Income Summary 200 Sales Returns and Allowance 200

Close income summary with a net income ($25,000) Income Summary 25,000 Retained Earnings 25,000

Close Dividends with $5000 balance Retained Earnings 5000 Dividends 5000

Paid the Payroll ($2000) less deductions: Social Security Tax($100) Medicare Tax($100) Employee Income Tax($100) Salary Expense SSTP MTP • 100 100 EITP Cash 100 1700

Record the employer’s income taxes: Social Security Tax($100) Medicare Tax($100) Federal Unemployment Tax($25) State Unemployment Tax($75) Payroll Tax Expense SSTP MTP • 100 100 FUT SUT 25 75

Paid the Federal Social Security Tax $1300 Social Security Tax Payable 1300 Cash 1300