Download

1 / 37

370 likes | 520 Vues

Impact of TRIA Expiration. • Nathan Bacchus, RIMS Sr. Government Affairs Manager • Elizabeth Guimaraes, Director, Risk Management, Nova Southeastern University, Inc. What to Expect. Gain an understanding of why the TRIA program was created and how it works.

E N D

• Nathan Bacchus, RIMS Sr. Government Affairs Manager • • Elizabeth Guimaraes, Director, Risk Management, Nova Southeastern University, Inc.

What to Expect • Gain an understanding of why the TRIA program was created and how it works. • Appreciate the program's importance to risk professionals, the industry and the economy as a whole. • Determine ways you can get involved in advocating for a long-term extension of the program.

Agenda • RIMS Position • History of TRIA • Why TRIA is Important • Arguments For/Against TRIA • How You Can Get Involved

RIMS Position • Strongly support permanent/long-term extension • Public/private partnership • Orderly & efficient response to acts of terror • Address Nuclear, Biological, Chemical and Radiological (NBCR) Coverage • Clarity

History and Evolution of TRIA • Before September 11, 2001 losses from terrorism events were included in GL policies. • Fears from late 2001 and into 2002 that lack of coverage posed a serious threat to many industry sectors and entire U.S. economy

History and Evolution of TRIA • A 2002 survey found that “$15.5 billion of real estate projects in 17 states were stalled or cancelled because of a continuing scarcity of terrorism insurance.

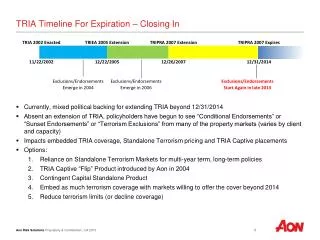

History and Evolution of TRIA • November 26, 2002 - The Terrorism Risk Insurance Act was signed into federal law • Government and private insurers share in losses from terrorism inside the U.S.

History and Evolution of TRIA • Minimum threshold of $5 million & 3 year duration • insurer deductible of 7% of earned premium increasing to 15% by the end of 2005 • Requirement that every insurer make terrorism coverage available

History and Evolution of TRIA • 2005 Extension • Established triggers: aggregate industry losses $50 million in 2006 and $100 million for 2007

History and Evolution of TRIA • Increased insurer deductible to 17.5% in 2005 and 20% in 2007; reduced the federal share of losses from 90% to 85% in 2007

History and Evolution of TRIA • 2007 Extension • Removed requirement that a covered act of terrorism be committed on behalf of a foreign person or interest

How TRIA Works • Certain criteria must be met before the federal government is required to step in • An individual act of terrorism must result in losses in excess of $5 million in the United States or to U.S. air carriers or sea vessels.

How TRIA Works 2. This act must then be certified as an act of terror by the U.S. Secretary of the Treasury, Secretary of State, and Attorney General. 3. Aggregate insurance industry losses from certified acts of terrorism must exceed $100 million.

Defining “Act of Terrorism” • Violent or dangerous act toward human life, property, or infrastructure • Results in damage within the United States • Committed by individual(s) acting as part of an effort to coerce the civilian population or to influence the policy or affect the conduct of the U.S. Government by coercion

NBCR Coverage • Not explicitly included/excluded under TRIA • Language offered in 2007, but not adopted • 2008 GAO study • Coverage generally unavailable • Insurers generally exclude coverage from property coverage • Coverage generally offered in WC, Group Life, and Health coverage b/c of states

Why TRIA is Important • TRIA allows insureds to obtain adequate coverage at affordable prices - Without actuarial data, it is not possible to project sound rates for insurance coverage - Workers’ Compensation insurance requires coverage for workers in the event of injury or illness due to a terroristic act

Why TRIA is Important • Workers’ Compensation insurance requires coverage for workers in the event of injury or illness due to a terroristic act

Why TRIA is Important • Without coverage many businesses will be forced to self-insure - Most businesses cannot afford to absorb the costs of terrorism related losses, even with aid from state and federal agencies

Why TRIA is Important • Terrorism Risk Insurance is required to procure lending - Most financial institutions have required terrorism coverage since the 9/11

Why TRIA is Important • - A sample agreement reads as follows: • "insurance with respect to the Improvements and the Personal Property insuring against any peril now or hereafter included within the classification “All Risk” or “Special Perils” (including, without limitation, fire, lightning, windstorm, hail, terrorism and similar acts of sabotage, explosion, riot, riot attending a strike, civil commotion, vandalism, aircraft, vehicles and smoke), in each case (A) in an amount equal to 100% of the “Full Replacement Cost,”…"

Why TRIA is Important • Other coverage lines may also be affected - We have already seen the impact on workers’ compensation coverage

Marketplace Uncertainty • Increases of up to 10% for companies w/urban concentrations • 53% of companies expected to see increased rates • Standalone policies being offered • Sunset provisions, non-renewals, etc.

Opposing Views • Only helps major metropolitan areas • Can terrorism be modeled as other lines? • High government cost/Bailout of insurance companies • TRIA=NFIP • Reinsurance available

Modeling Terrorism Coverage • Not accidental • Unpredictable/Random • Events rare but losses from one single event could be catastrophic • Confidential information

Differences from Bailouts & NFIP • Not primary insurer or major creditor under TRIA • TRIA is reinsurance • Only cost government money in the event of catastrophic attack • Recoupment mechanism in place • Government has responsibility

Reinsurance Capacity? • Reinsurance industry does have available capacity generally • Same issues with modeling terrorism • 2014 PWG report found industry “does not have capacity to provide reinsurance” • Estimates $6 to $8 billion reinsurance available for terrorism

Congressional Outlook • Series of House & Senate hearings • New leadership of HFS and Senate Banking • Huge turnover since last extension • 28 members of HFS new

Congressional Outlook • SB 2244, Introduced April 10, 2014 • Bipartisan Senate Banking agreement • Increases copay from 15%-20% • Recoupment from $27.5 B to $37.5 B

Congressional Outlook • House Financial Services • Transition to NBCR • Far less government responsibility • Far more taxpayer protection • Certification Process • Extension length

What Can You Do? • Contact member(s) of Congress • Particularly in districts of HFS members • Legislative Alerts • Attend RIMS Legislative Summit

Questions, Final Comments and Contact Information • Nathan Bacchus • nbacchus@rims.org • Elizabeth Guimaraes • guimarae@nova.edu