Download

1 / 10

100 likes | 104 Vues

Current Individual Income Tax Rates 1. Current Individual Income Tax Rates 2. Income Tax Deductions and Credits. A tax deduction reduces your income. For example, if you make $80,000 and have $10,000 in deductions, your taxable income is $70,000.

E N D

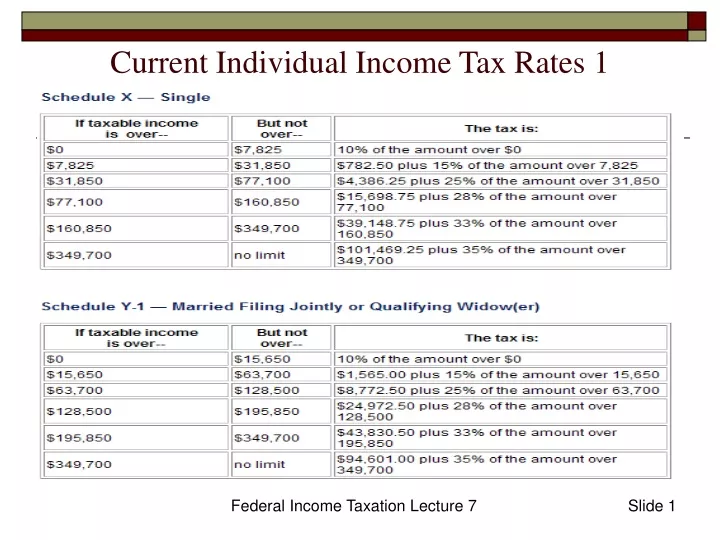

Current Individual Income Tax Rates 1 Federal Income Taxation Lecture 7

Current Individual Income Tax Rates 2 Federal Income Taxation Lecture 7

Income Tax Deductions and Credits • A tax deduction reduces your income. For example, if you make $80,000 and have $10,000 in deductions, your taxable income is $70,000. • A tax credit is a reduction in the amount of taxes you actually owe (much better than a credit). For example, if your tax computed on your income is $15,000 and you have a $3,000 tax credit, you owe only $12,000. • There are a wide variety of both deductions and credits that are available under the IRC, though deductions are more common. Federal Income Taxation Lecture 7

Standard Deduction vs. Itemized Deductions Taxpayers generally have a choice. They can: • A) Take a standard (i.e., minimum) deduction allowed under the IRC off his or her gross income. For 2007, that amount is $5,350 (double for married filing jointly). • B) Itemize Deductions for a variety of different expenses, such as mortgage interest, state taxes, etc. • Miscellaneous deductions (not listed in section 67 of the IRC) are subject to a limit of 2% of one’s gross income. Federal Income Taxation Lecture 7

Exemptions and Credits for Dependents • Each person living in one’s home (including oneself) entitles the taxpayer to an exemption (i.e., a deduction, but one that’s not counted as an itemized deduction, so it can be taken in addition to the standard deduction). This amount increases with inflation (currently $3,300). This is phased out for high income taxpayers. • Child tax credit: $1,000 credit for each qualifying child. Federal Income Taxation Lecture 7

Earned Income Tax credit • This is meant to help the “working poor” and allows benefits to workers who earn low incomes. • This allocates a substantial tax credit for the first few thousand dollars of income earned. The credit is increased for families with children and is phased out for people with higher incomes. • If the credit amount is more than the person’s tax liability, the excess is refunded! This means that some people actually get back more than they pay in federal income tax! Federal Income Taxation Lecture 7

Personal Casualty Losses • A taxpayer may deduct personal loss (e.g., house burned down, etc.) to the extent that the loss exceeds 10% of one’s income after deducting $100 per loss. But keep in mind: • It cannot be deducted to the extent that it’s covered by insurance. • Watch out for capital gains tax if the insurance pays more than the basis • For similar reason, the deductible loss cannot exceed the basis • Applies only to losses based on “sudden, unexpected and unusual” losses, such as fire, theft, shipwreck. Does NOT include damage by: • Household pets, termites, items lost in the house • Anything caused by the gross negligence of the taxpayer • Contrast: Business losses which are 100% deductible for any loss for any business related reason. Federal Income Taxation Lecture 7

Extraordinary Medical Expenses • Compare: • Medical benefits paid by an employer are deductible only to the extent that they exceed 7.5% of one’s adjusted gross income (AGI). • Medical Benefits paid by an employer are fully deductible as a business expense. Federal Income Taxation Lecture 7

What is a Medical Expense? • To qualify as a healthcare expense, the expense must be paid for the “diagnosis, cure, mitigation, treatment or prevention” of a disease. Other expenses to improve health (e.g., vacation to reduce stress) are not deductible. • The following have been allowed as medical expenses: • Weight loss treatments • Necessary home improvements (e.g., ramps, railings, lifts, etc.) but only over and above the value increase to the house • Cosmetic surgery, only if necessary to correct injury or disease • Medical insurance • Hospital stays, but only up to certain limits • Nursing home stays, in most cases Federal Income Taxation Lecture 7

Health Savings Accounts • These were created recently - in 2003. • The taxpayer must have high deductible health insurance ($1,000 for individuals, or $2,000 for families). • Contributions to the HSA are tax deductible, but only up to certain limits: the lesser of: • The amount of the deductible • A fixed sum; as of 2005: • $2,650 for individuals/$5,150 for families if the taxpayer is under 55 • $3,100 for individuals/$5,650 for families if the taxpayer is under 55 • Income earned by the HSA is not counted as taxpayer’s income • The money in the HSA can only be used for medical expenses. Federal Income Taxation Lecture 7