Download

1 / 4

40 likes | 116 Vues

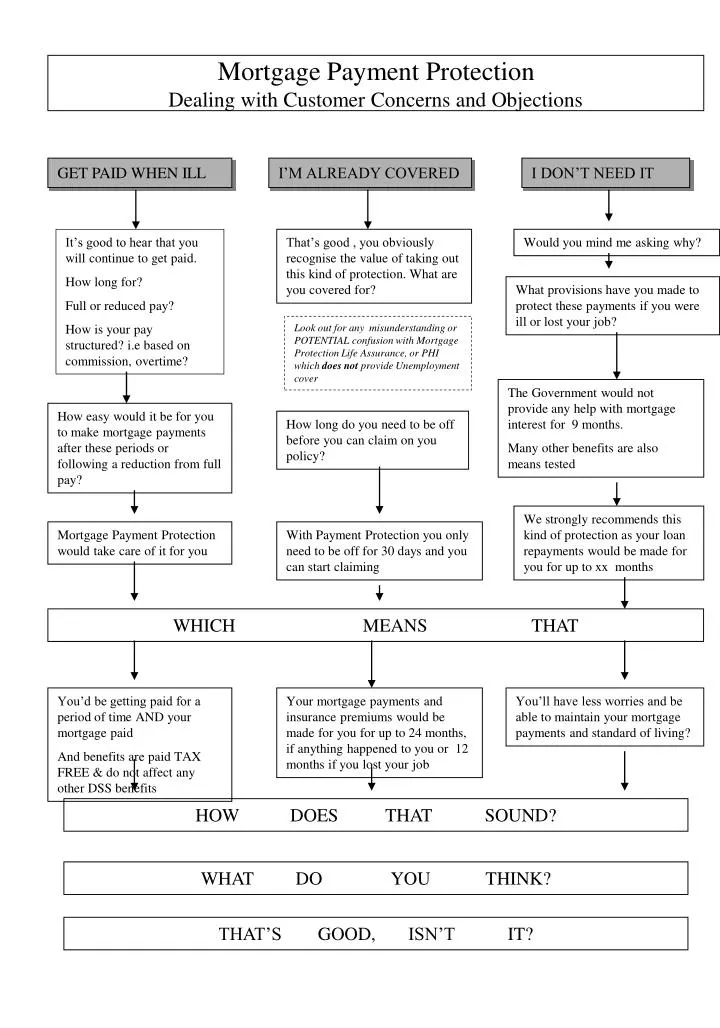

Mortgage Payment Protection Dealing with Customer Concerns and Objections. GET PAID WHEN ILL. I’M ALREADY COVERED. I DON’T NEED IT. It’s good to hear that you will continue to get paid. How long for? Full or reduced pay? How is your pay structured? i.e based on commission, overtime?.

E N D

Mortgage Payment ProtectionDealing with Customer Concerns and Objections GET PAID WHEN ILL I’M ALREADY COVERED I DON’T NEED IT It’s good to hear that you will continue to get paid. How long for? Full or reduced pay? How is your pay structured? i.e based on commission, overtime? That’s good , you obviously recognise the value of taking out this kind of protection. What are you covered for? Would you mind me asking why? What provisions have you made to protect these payments if you were ill or lost your job? Look out for any misunderstanding or POTENTIAL confusion with Mortgage Protection Life Assurance, or PHI which does not provide Unemployment cover The Government would not provide any help with mortgage interest for 9 months. Many other benefits are also means tested How easy would it be for you to make mortgage payments after these periods or following a reduction from full pay? How long do you need to be off before you can claim on you policy? We strongly recommends this kind of protection as your loan repayments would be made for you for up to xx months Mortgage Payment Protection would take care of it for you With Payment Protection you only need to be off for 30 days and you can start claiming WHICH MEANS THAT You’d be getting paid for a period of time AND your mortgage paid And benefits are paid TAX FREE & do not affect any other DSS benefits Your mortgage payments and insurance premiums would be made for you for up to 24 months, if anything happened to you or 12 months if you lost your job You’ll have less worries and be able to maintain your mortgage payments and standard of living? HOW DOES THAT SOUND? WHAT DO YOU THINK? THAT’S GOOD, ISN’T IT?

Mortgage Payment ProtectionDealing with Customer Concerns and Objections WANT LOWEST REPAYMENTS I’LL USE MY SAVINGS IT’S TOO EXPENSIVE May I ask what you are comparing the cost against? I understand, however how would you manage your payments of £x over the months should anything unforeseen happen, e.g redundancy, illness, accident etc? Yes, you could use your savings How easily accessible are they? How much interest would you lose? For less than x pence per day you can fully protect your mortgage and insurance payments for up to 12 months. What else could you buy for that?, newspapers, beer, cigarettes, chocolate Mortgage Payment Protection is a way of guaranteeing that your mortgage commitment would be maintained for up to 12 months Why not let us protect your mortgage payments, so you can use your savings for other important things This guarantees your payments are made for you. WHICH MEANS THAT We’d pay your mortgage payments for up to 12 months. You wouldn’t have to worry about your account falling into arrears, so you would protect your credit rating Our Payment protection policy will relieve you from the worry of keeping up your payments, should the unexpected happen AND your saving remain intact You and your family are free from worry about keeping up with mortgage payments for the time your are off work HOW DOES THAT SOUND? WHAT DO YOU THINK? THAT’S GOOD, ISN’T IT?

Payment ProtectionDealing with Customer Concerns and Objections I HAVE A SECURE JOB DIDN’T TAKE IT LAST TIME SPOUSE WOULD PAY That’s good to hear, but who can be 100% sure these days. Look what has happened to jobs in Banking, Insurance, the Forces May I ask how easy would it be for him/her to pay the mortgage and all the other bills on one wage. As you have taken a joint mortgage, you rely on 2 wages to make ends meet When /Why did you feel you didn’t NEED it last time Since Oct 1995 the Government have changed the waiting period for any help with interest payments to 9 months. What would happen is you were off sick for a lengthy period, or had an accident May I explain how Payment Protection would work for you You would be able to claim £x per month And your partners income will not affect the claim How would you make the repayments , and for how long How would you be able to cope with mortgage payments should the unexpected happen now Mortgage Payment Protection would act as a safety net for you Payment Protection is a low cost method of ensuring your mortgage payments are accounted for WHICH MEANS THAT Your mortgage repayments and insurance premiums would be secured for the time you were off, for up to 12 months any one claim These payments meet your monthly payments, leaving any other income you have free for other household bills Your mortgage commitment to your lender and your partner are guaranteed and you have peace of mind knowing your monthly bills would be paid HOW DOES THAT SOUND? WHAT DO YOU THINK? THAT’S GOOD, ISN’T IT?

Payment ProtectionDealing with Customer Concerns and Objections I HAD A BAD CLAIMS EXPERIENCE I’m extremely sorry to hear that May I ask what happened? Who was the cover with? When did you make the claim? May I explain how our plan would work? ( match to circumstances) You would be able to claim after 30 days of disability or loss of job We do cover self employed…. We do treat contract workers as permanent employees if….. Our plan complies with and exceeds the new Government & C.M.L Minimum cover wording standards WHICH MEANS THAT You can be sure Mortgage Payment Protection would meet your needs should the worst happen and you were to lose your job or become disabled from illness or accident HOW DOES THAT SOUND? WHAT DO YOU THINK? THAT’S GOOD, ISN’T IT?