Download

1 / 47

500 likes | 966 Vues

Lesson 7 Merchandise Inventories and Cost of Sales. Task Team of FUNDAMENTAL ACCOUNTING School of Business, Sun Yat-sen University. Outline. Flow of inventory cost Items and costs of merchandising inventory Assigning costs to inventory Lower of cost or market

E N D

Lesson 7 Merchandise Inventories and Cost of Sales Task Team of FUNDAMENTAL ACCOUNTING School of Business, Sun Yat-sen University

Outline • Flow of inventory cost • Items and costs of merchandising inventory • Assigning costs to inventory • Lower of cost or market • Errors in measuring inventory • Inventory estimating method

Introduction • While sales and purchases are the focus of operations, inventory is no less important. Inventory costing and evaluation methods can substantially influence the bottom line. Since China’s listed companies were permitted to write down inventories in 1998, inventory has long been criticized as the “income adjustor”. Besides, inventory costing policies and the scope of inventory can also significant change the current and future years income numbers.

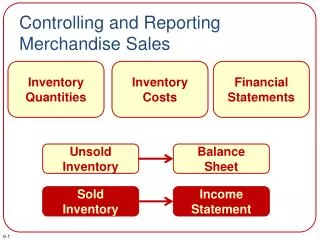

Purchasesfor the Period BeginningInventory + Goods Availablefor Sale Ending Inventory(Balance Sheet) Cost of Goods Sold(Income Statement) + Beginning inventory + Purchases – Ending inventory = Cost of goods sold Nature of Inventory and Cost of Goods Sold

Merchandiser MerchandisePurchases Cost ofGoods Sold MerchandiseInventory Manufacturer RawMaterials Raw MaterialsInventory Work in ProcessInventory Finished GoodsInventory DirectLabour Cost ofGoods Sold FactoryOverhead Flow of Inventory Costs

Accounting for Inventory • Accounting for inventory requires several decisions which include: • Items to include in cost. • Inventory System. • Perpetual or Periodic • Costing Method. • FIFO, LIFO, Weighted Average, Specific ID • Use of estimates. • Gross profit method, Retail inventory method

Items in Merchandise Inventory • Inventory includes all goods owned by a company and held for sale. • Items requiring special attention: • Goods in Transit • Goods on consignment • Obsolete or damaged goods

Costs of Merchandise Inventory • All expenditures necessary to bring an item to a saleable condition and location. • This includes: • Invoice price less discounts • Import duties • Transportation-in • Storage • Insurance

Assigning Costs to Inventory • Management must decide on method of determining unit cost. • This will affect both the incomestatement and the balance sheet. • Methods: • Specific Identification • FIFO • LIFO • Average Cost

Specific Identification • This method is used when items: • Are unique. • Can be directly identified with a specific purchase and its invoice. Examples: Automobiles, custom furniture, art.

The opening inventory consists of 10 units @ $90/unit. Specific Identification-Example

This results in two layers of inventory. Additional units re purchased @ $100/unit. Specific Identification-Example

On August 14, 20 units are sold. Eight of these units came from the opening inventory and the remaining 12 units came from the August 3 purchase. Specific Identification-Example

This leaves 2 units remaining from the original inventory and 3 units remaining from the August 3 purchase. Specific Identification-Example

First-In, First-Out (FIFO) • Based on the assumption that the items are sold in the order acquired. • When a sale occurs: • The earliest units purchased are charged to Cost of Goods Sold. • The cost of the most recent purchases remain in inventory

Under FIFO, units are assumed to be sold in the order acquired. Therefore, of the 20 units sold on August 14, the first 10 units come from beginning inventory. Therefore, those 10 units are removed from the inventory record based on the cost of those units of $90. FIFO-Example

The remaining 10 units sold on August 14th come from the next purchase, made on August 3rd. Therefore, these units are removed from the inventory record based on their cost of $100. FIFO-Example

Ending inventory approximates current replacement cost. The ending inventory consists of the 5 remaining units from the August 3 purchase. FIFO-Example

Last-In, First-Out (LIFO) • Based on the assumption that the most recently purchased items are sold first. • When a sale occurs: • The latest units purchased are charged to Cost of Goods Sold. • The cost of the earliest purchases remain in inventory.

Of the 20 units sold, these units are assumed to be sold first. LIFO-Example

Once the latest units purchased are sold, units are sold from the previous purchase. LIFO-Example

This leaves 5 units remaining from the first purchase. Better matches current costs in cost of goods sold with revenues. LIFO-Example

Average cost per unit Cost of goods available for sale Number of units available for sale = Moving Weighted Average Method • Under this method, the cost of all units are averaged together.

Additional units are purchased @ $100/unit. This results in an average cost of $100/unit. (10 x $90) + (15 x $100) 25 units Moving Weighted Average-Example

These 20 units are sold at the average cost of $96/unit. Moving Weighted Average-Example

This leaves 5 units remaining at an average cost of $96/unit. Smoothes out purchase price changes. Moving Weighted Average-Example

Financial Reporting • Because prices change, the choice of an inventory method influences both income statement and the balance sheet.

Lower of Cost or Market • Inventory must be reported at market value when market is lower than cost (conservatism principle). • Market may be defined as: • Net realizable value • Current replacement cost • May be applied in one of three ways: • Separately to each item. • To major categories of items. • To the inventory as a whole.

Lower of Cost or Market A motor retailer has the following items in inventory:

Lower of Cost or Market Compute lower of cost or market for individual inventory items.

Lower of Cost or Market Compute lower of cost or market for the two groups of inventory items.

Lower of Cost or Market Compute lower of cost or market for the entire inventory.

Retail Inventory Method • Occasionally used for interim period reporting. • Needed information includes: • Beginning inventory at cost and retail. • Net purchases at cost and retail. • Net sales.

Goods available for sale at retail Net sales at retail Ending inventory at retail – Step 1 = Goods available for sale at cost Goods available for sale at retail Cost to retail ratio Step 2 = ÷ Ending inventory at retail Cost to retail ratio Estimated ending inventory at cost Step 3 = × Retail Inventory Method

Gross Profit Method • Estimate ending inventory by applying the gross profit ratio to net sales at retail. • Useful when inventories have been destroyed, lost or stolen.

Net sales at retail 1.0 minus the gross profit ratio Estimated cost of goods sold × Step 1 = Goods available for sale at cost Estimated cost of goods sold Estimated ending inventory at cost – Step 2 = Gross Profit Method

Gross Profit Method • In March of 2002, CheTec Company’s inventory was destroyed by fire. CheTec’s normal gross profit ratio is 40% of net sales. At the time of the fire, CheTec showed the following balances:

Gross Profit Method Step 1

Gross Profit Method Step 2

Summary • Inventory includes all goods owned by a company and held for sale. • Costs of merchandise inventory include all expenditures necessary to bring an item to a saleable condition and location. • There are four method to assigning costs to inventory: specific identification, FIFO, LIFO and average cost. The average cost method smoothes out purchase price changes. Ending inventory under FIFO approximates current replacement cost. LIFO better matches current cost in cost of goods sold with revenue. • Inventory must be reported at market value when market is lower than cost. • Retail inventory method and gross profit method can be used to estimate ending inventory.

Discussion Case Northeast Pharmaceutical • When preparing financial statement of 2012, Northeast Pharmaceutical recorded RMB 21,280,000 expenses as inventory cost, which carries to next year’s beginning inventory. As a result, the bottom line is RMB 19,950,000 profits, instead of a big loss. This was discovered and was fined by CSRC as securities fraud.

Discussion Case • Required: • What’s the difference between expenses and inventory costs? • What are the impacts of inventory errors on financial statements? • Why Northeast Pharmaceutical chose to report false income numbers? • How to prevent the occurrence of such kind of cases.