Download

1 / 33

330 likes | 455 Vues

Generating Superior Returns From a Traditional Asset Class. The Growth of Serviced Offices as an Investment. Business Centre Capital Co. Ltd. Established 1999 Specialising in serviced office/business centres Adviser to a number of profile institutions and business centre operators

E N D

Generating Superior Returns From a Traditional Asset Class The Growth of Serviced Offices as an Investment Business Centre Capital Co. Ltd www.b3c.biz

Business Centre Capital Co. Ltd • Established 1999 • Specialising in serviced office/business centres • Adviser to a number of profile institutions and business centre operators • Established first ever publicly listed business centre fund • Set up a number of LPs • Combined asset value of circa £60 million Business Centre Capital Co. Ltd www.b3c.biz

Structure • Overview • Size • Players • Business Models Business Centre Capital Co. Ltd www.b3c.biz

Overview • A Definition • The provision of short term space supported by a range of business services actively managed by on-site staff Business Centre Capital Co. Ltd www.b3c.biz

Size Globally • > 10,000 business centres • + 1,000 operators • > 70 countries • < 1% of global office space Business Centre Capital Co. Ltd www.b3c.biz

Size in the UK • Currently represents nearly 2% of UK office space • Equivalent to nearly 1.5 million square metres • Represents around 5% of space in Central London • Around 350 operators of flexible business space in the UK in 1,100 centres • Workstation capacity has doubled in 5 years • Between 2000 and 2006 the number of workstations rose from around 120,000 to over 200,000 Business Centre Capital Co. Ltd www.b3c.biz

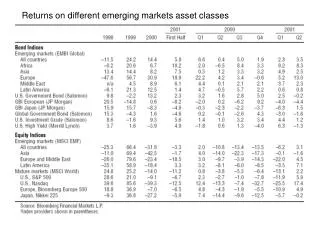

UK Demographics Source: DTZ Business Centre Capital Co. Ltd www.b3c.biz

UK Major Players Quality Fully Serviced Regus EOG Avanta BEG MWB SOG Citibase MLS Leased Owned Workspace Bizspace Lenta Semi Serviced Business Centre Capital Co. Ltd www.b3c.biz

Long Term Structural Growth • Drivers – “it’s what the client wants” • Costs – TOCC shows it is more expensive to take a traditional lease • Accounting rules – require leases on balance sheet • Technology – good infrastructure required • Infrastructure costs are shared amongst the occupiers • Flexibility – occupiers can expand/contract at will • Simplicity – costs are easy to understand and predictable • Convenience – allowing occupiers to concentrate on their business Business Centre Capital Co. Ltd www.b3c.biz

Investment Potential • High yield • Capital Growth • Scale • Brand Business Centre Capital Co. Ltd www.b3c.biz

High Yield • Serviced offices provide a higher yield • typical income yield can exceed 7% • typical capital growth can exceed 4% • Business Centre Properties plc • First ever publicly available fund in the sector • £40 million of serviced office properties • Average income yield 7.5% to investors after fund costs • Share price growth of 36% since launch ’04/04 Business Centre Capital Co. Ltd www.b3c.biz

Capital Growth • Conversions • Conversion of existing office stock to serviced offices • Real options in secondary locations with secondary properties • Good options in primary locations where little or no flexible space • Development • Creation of specific serviced office developments • Big meeting room/conferencing facilities • Clubs, restaurants • High tech wiring, easy demountable partitioning • Emerging markets Business Centre Capital Co. Ltd www.b3c.biz

Yield Shift • Serviced offices have followed yields down • BCP bought its first building at a cap rate of 11% • 2004, 11% • 2005, 9% • 2006, sub 8% • The risk margin has narrowed • In 2004 the margin was around 2-3% • Now it is 1-2% Business Centre Capital Co. Ltd www.b3c.biz

POWER (Property Opportunities With Enhanced Returns) Fund • Philosophy • Structure • Expertise • Timings Business Centre Capital Co. Ltd www.b3c.biz

Philosophy • “Global provision of flexible working for individuals and businesses in secure, comfortable office accommodation” Business Centre Capital Co. Ltd www.b3c.biz

Structure Luxembourg Domicile UK Sub Fund Europe Sub funds North America Sub funds ROW Sub funds Local operator ABCN centres centres centres (Replicated across each sub fund) Business Centre Capital Co. Ltd www.b3c.biz

Scale • Economies of scale • Spread of infrastructure costs • Best economies from running assets in hubs • HQ costs spread • Portfolio effect • Spread of risk through geography • Through client base • Big means • Saleable >£300m • Brandable • Listable Business Centre Capital Co. Ltd www.b3c.biz

Brand value • A brand has strategic value • Regus today has a £1.5 billion stock market capitalisation • That is 20x earnings! Business Centre Capital Co. Ltd www.b3c.biz

Alliance Business Centres Network (ABCN) • ABCN is: • “a distributed network of senior industry professionals” • Only global business centres network • 650 locations in 37 countries • Broad range of services to members • Market intelligence • Marketing and referrals • Alliance Access • Franchising • Purchasing Business Centre Capital Co. Ltd www.b3c.biz

Timings • Fund life expected to be 10 years • Seed investment £100 million equity • Investment period – 3 years in the UK • Expected ROW expansion year 2 onwards • Target IRR 25%+ at 5 year point Business Centre Capital Co. Ltd www.b3c.biz

Expertise • Jonathan Price (CEO EMA) – 8 years in sector • Barrister at law and former investment banker • President of UK Chapter of FIABCI • NED to international serviced office operator • Frank Cottle (CEO US & ROW) – 22 years in sector • Chairman of Alliance Business Centres Network • Former investment banker specialising in real estate • Board member OBCAI • Former owner operator of serviced offices • Chris Brierley (COO)– 5 years in the sector • Former investment banker • NED on a number of property related funds • Former director of a research company • Former FD of fund manager (CFO) – 14 years • Former Property director of serviced office operator – 10 years Business Centre Capital Co. Ltd www.b3c.biz

Exit • Trade sale • To a new entrant • To an existing operator • Securitisation • >£300m • REIT • Workspace has become a REIT Business Centre Capital Co. Ltd www.b3c.biz

Business Centre Capital Co. Ltd www.b3c.biz

Lease v. Ownership • Leasehold Operator • Long term liability to short term income profile • Can be mitigated where a turnover lease or management contract is in place – landlord shares risk • Low capital commitment allows rapid expansion Business Centre Capital Co. Ltd www.b3c.biz

Lease v. Ownership • Owner Operator • Freehold/long leasehold • Avoids mismatch of assets and liabilities • High capital commitment • Double whammy of rents falling and property value declining in poor market conditions • But more flexibility in getting and retaining clients Business Centre Capital Co. Ltd www.b3c.biz

Valuation • Issues • Serviced offices are hybrid: renting space and offering services • Property valuation and company valuation approach diverge • RICS approach to going concern valuation is based on “strictly limited use” and serviced offices typically operate from traditional office premises • Red Book needs to be revised • Multiples are beginning to emerge • Businesses operating out of leased premises on EBITDA multiples of 4-6 times • Businesses that own the operating asset 13-16 times EBITDA Business Centre Capital Co. Ltd www.b3c.biz

Listed Company Valuations Business Centre Capital Co. Ltd www.b3c.biz

RGU Share Price Business Centre Capital Co. Ltd www.b3c.biz

SVO Share Price Business Centre Capital Co. Ltd www.b3c.biz

MBE Share Price Business Centre Capital Co. Ltd www.b3c.biz

Alternative Asset Valuations • Valuations of student accommodation • Unite • 12/06 - EBITDA £103 million, EV £1.070 billion = 10 x • Valuations of self storage • Big Yellow • 09/06 – EBITDA £70 million, EV £900 million = 13 x Business Centre Capital Co. Ltd www.b3c.biz

BYG Share Price Business Centre Capital Co. Ltd www.b3c.biz

Metrics • MWBX - £67.1m (^23%), PTP £7.8m (£2.7m) • 60 locations • Regus - £680m (^47%), PTP £77.5m (£38.7m) • 950 centres Business Centre Capital Co. Ltd www.b3c.biz