Download

1 / 10

E N D

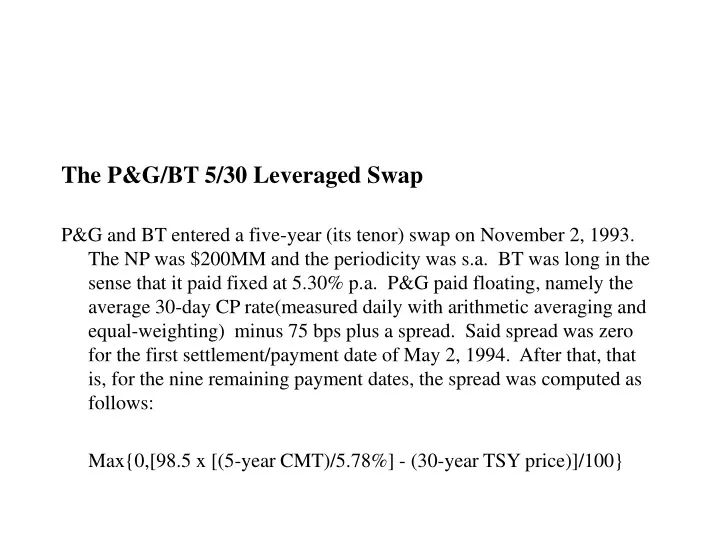

The P&G/BT 5/30 Leveraged Swap P&G and BT entered a five-year (its tenor) swap on November 2, 1993. The NP was $200MM and the periodicity was s.a. BT was long in the sense that it paid fixed at 5.30% p.a. P&G paid floating, namely the average 30-day CP rate(measured daily with arithmetic averaging and equal-weighting) minus 75 bps plus a spread. Said spread was zero for the first settlement/payment date of May 2, 1994. After that, that is, for the nine remaining payment dates, the spread was computed as follows: Max{0,[98.5 x [(5-year CMT)/5.78%] - (30-year TSY price)]/100}

Where 5-year CMT is the 5-year constant-maturity Treasury, and 30-year TSY price is the midpoint of the bid and offer cash bond prices for the 6.25% Treasury bond maturing on August 2023. P&G hoped that the spread would be zero, thus permitting it to earn 5.30% on a payment of CP less 75 bps. But rates moved against P&G and it got crushed. A similar deal was done between BT and Gibson Greetings. P&G sued BT for sell-side abuse and was partly successful. BT was fined and disciplined by the SEC. BT’s image was harmed. The court case and SEC action together established modern standards for sell-side conduct.

Notice that P&G could have achieved the same gamble (get it?) through trading an interest rate spread option. But embedding (read “hiding”) the option in a swap made the position off-balance sheet and therefore not obvious to analysts and the like. FAS133makes swaps - like other derivatives - on-balance sheet, to curb this sort of thing. Note: Paine-Webber MMMF “breaking the buck” case.

A Generic Swap Application: “Sophistication Arbitrage” Suppose that you invent an interest rate swap where the floating amount paid on the payment date is determined by the rate observed on the payment date itself - rather than say twelve-months ago (assuming an annual swap and ignoring the typical Actual/360 day count convention). Define the reset dates in the swap as t(i) for i = 0, 1, 2, ..., n, with T(i) = t(i+1) - t(i). Define R(i) as the LIBOR rate for the period between t(i) and t(i+1), F(i) as the forward value of R(i), and vol(i) is the volatility of this rate, that is, the standard deviation of its natural logarithm. Vol(i) would come from a caplet or LIBOR option price.

In your swap, the floating payment at time t(i) is based on R(i), rather than the traditional R(i-1). It can be proven that the valuation of this swap should be based on the assumption that the forward rate is not F(i), but instead is F(i) + {[F(i)^2(vol(i)^2)(T(i)t(i))]/[1 + F(i)T(i)]}. The term in { } represents a type of convexity adjustment.

For example, let the NP be $100MM, let the fixed swap rate be 2%, payments are annual, the tenor is 2 years, the LIBOR curve is flat at 2% per annum (with annual compounding), and the vol curve is flat at 20% per annum. Ignore day count conventions. Here, a typical swap would have a zero value. But the floating payments in your swap would be estimated at a convexity-adjusted rate of .02 + {(.02^2)(.20^2)(t(i))/(1.02)} = .02 + .0000156t(i). So the floating payments at the end of years 1 and 2 should be based on rates of 2.00156% and 2.00312%. The value of the long swap is positive $4,528.

You are successful at marketing this swap, and you load up on long positions and engage in offsets by shorting plain-vanilla swaps. Is this sell-side abuse? Do you think you would be caught? If so, by the time you get your bonus and retire to Paris by way of say Morrocco?

Credit Derivatives Lecture Outline • NP = $180B in 1997 and $5100B in 2004 • CDS about 75% of market • Banks about 50% of end-users (regulatory capital relief and diversification of loan portfolios) • Underlying credits 44% North America, 40% Europe, 11% Asia

Hull (Chapter 27, 5th ed.) provides coverage of: • CDS valuation • Implying default probabilities of reference credit assets from CDS’s • Variations of CDs’s including binary and basket CDS’s • Total Return Swaps • Credit Spread Options • CDO’s

We focus on applications • Synthetic CDO’s • Diversification of concentrated credit risk Note: See “Credit Derivatives” file. But first a simple one: In the beginning of 2001 Enron was rated Baa1/BBB+ and swap rates on 5-year CDS’s were running around 115/135 bid/offer. So one could have insured $100MM for $1.35MM per year. Of course, Enron was in default by the end of 2001.