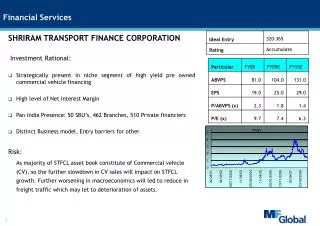

Download

1 / 24

260 likes | 414 Vues

Financial Services Seminar 3. 10 th July 2014. THE REGULATION OF SHARES OFFERINGS AND FINANCIAL PROMOTIONS. Tim Green. PURPOSE OF THE SEMINAR. This seminar is directed at commercial and regulatory lawyers working with the financial services industry who may need to advise clients on:

E N D

Financial Services Seminar 3 10th July 2014

THE REGULATION OF SHARES OFFERINGS AND FINANCIAL PROMOTIONS Tim Green

PURPOSE OF THE SEMINAR • This seminar is directed at commercial and regulatory lawyers working with the financial services industry who may need to advise clients on: • The scope of regulation when offering shares in a company for sale to the general public. • The scope of regulation when applied to promoting financial services. • The context for this talk is up turn in all sectors of economy taken up where banks remain reluctant to lend to SMEs and businesses may be looking to raise funds from private investors.

The general prohibition on offering shares for sale without an FCA approved prospectus • There is a general prohibition on the offer for sale of transferrable securities in the UK unless the prospectus making that offer satisfies the Prospectus Rules and is approved by the FCA (s85 (1) FSMA). • Section 85 (1) of FSMA provides that, “ 85 (1) It is unlawful for transferrable securities to which this subsection applies to be offered to the public in the United Kingdom unless an approved prospectus has been made available to the public before the offer is made.” • Section 85 (3) of FSMA makes it a criminal offence punishable with up to 2 years imprisonment to contravene section 85 (1). I. OFFERING SHARES FOR SALE TO THE GENERAL PUBLIC

What is a transferrable security for the purposes of the general prohibition on the sale of transferrable securities without an approved prospectus? • “Transferrable securities” are defined by the Prospectus Directives 2003 and 2010 and by reference to Directive 93/22/EEC. The Directive describes transferrable securities in this way: "Transferable securities" means those classes of securities which are negotiable on the capital market, such as government securities, shares in companies…” • This is a broad definition which includes most classes of share offering.

Would the sale of shares in a company that are not in fact to be listed on capital markets come within the general prohibition? Most types of company shares are transferrable. Even if it is not proposed that the shares in the company to be sold are to be offered to regulated markets like AIM or the London Stock Exchange, the shares in a company are still transferrable. Thus shares in a company belong to a class of security are negotiable on the capital market, namely equities (even if the proposal is that the share in question is not offered in fact offered on the capital markets). A share offering that relates to transferrable securities that may be negotiated on a capital market needs an FCA approved prospectus to be lawfully promoted and sold.

Are there exceptions to the general prohibition on offering securities to the public without an FCA approved prospectus that relate to certain types of securities? • Section 85 (5) FSMA provides that, “85 (5) Subsection (1) applies to all transferrable securities [THE GENERAL PROHIBITION ON THE OFFERNING OF SECURITIES WITHOUT AN FCA PROSPECTUS APPROVED] other than- • those listed in Schedule 11 A; • such other transferrable securities as may be specified in the prospectus rules. • Schedule 11 A generally relates to investments that would appeal to institutional investors of one type or another. • As a rule of thumb: share offerings to the public require an FCA approved Prospectus to be lawful.

When is an offer of transferrable securities made to the public? • There is no definition of “the public” in the Prospectus Directive. However the Directive does provide at Article 2 (d) that: "offer of securities to the public" means a communication to persons in any form and by any means, presenting sufficient information on the terms of the offer and the securities to be offered, so as to enable an investor to decide to purchase or subscribe to these securities. This definition shall also be applicable to the placing of securities through financial intermediaries”. • The purpose of both Directives is to protect investors and to allow the smooth running of markets. • The offering of shares to sophisticated retail investors would include “the public” for the purpose of section 85 (1) FSMA.

If there are few exceptions to the type of share that needs an approved prospectus, are there exceptions to the type of investors who need to see an approved prospectus? • There are exceptions to the prohibition in section 85 (1) and (3) FSMA contained in section 86 FSMA. Those exceptions are as follows: • The offer is made to or directed at qualified investors only [qualified in the sense of being professional investors] OR, • The offer is made to or directed at fewer than 150 persons other than qualified investor per EEA state OR, • The minimum consideration which may be paid by any person for transferrable securities acquired by him pursuant to the offer is at least 100,000 Euros [Note; this has increased from 50,000 Euros by the Prospectus Directive 2010] OR, • The transferrable securities being offered are denominated in amount of at least 50, 000 Euros; OR • The total consideration for the transferrable securities being offered cannot exceed 100,000 Euros (or equivalent amount).

Who are qualified investors? The persons who may be offered these shares can include private individuals providing the minimum investment to be made by them is 100,000 Euros. Otherwise, the share offering must be directed at qualified investors only. A “qualified investor” has a specific meaning under FSMA and the Prospectus Rules but is generally speaking a person authorised by the FCA to deal in transferrable securities by way of business. A qualified person need not be a government body. Note: the Prospectus Rules prohibit the offer of shares to the public unless the Prospectus has FCA approval or the share offering is aimed a specific class of professional investor.

The general prohibition of promoting many financial services Section 21 FSMA provides is that in the course of business, unauthorised persons must not communicate an invitation or inducement to engage in investment activity unless the content of the communication is approved by an authorised person or is exempt. II. RESTRICTIONS ON FINANCIAL PROMOTIONS

Invitation or inducement? • FSMA does not contain any definition of the expressions “invitation” or inducement” leaving them to their natural meaning. The ordinary dictionary entries for “invitation” and “inducement” offer several possible meanings for the expressions. An “invitation” is capable of meanings from merely asking graciously or making a request to encouraging or soliciting. • The word “inducement” is given meanings ranging from bringing about to prevailing upon or persuading. In guidance issued pursuant to the section 139 A FSMA, the FCA has indicated it will look closely at the context of words and behaviour to see if they come within these definitions (PERG 8.4.1 G).

The FCA guidance on what is meant by invitation or inducement… continued. Invitation- The FCA guidance provides states as follows: • “PERG 8.4.5 G An invitation is something which directly invites a person to take a step which will result in his engaging in investment activity. Examples include: • Direct offer financial promotions. • A prospectus with application forms. • Internet promotions”

The FCA guidance on what is meant by invitation or inducement • PERG 8.4.6 G “Merely asking a person if they wish to enter into an agreement with no element of persuasion or incitement will not, in the FCA’s view, be an invitation under section 21. For example, the FCA does not consider an invitation to have been made where: • A trustee or nominee receives an offer document of some kind and asks the beneficial owner whether he wishes it to be accepted or declined; • A person such as a professional adviser enquires whether or not his client would be willing to sign an agreement; or • A person is asked to sign an agreement on terms which he has already accepted or to give effect to something which he has already agreed to do.”

Inducment – • PERG 8.4.7 G describes an inducement as, “A significant step in persuading or inciting or seeking to persuade or incite a recipient to engage in investment activity”

Are there exceptions to the prohibition on inviting or inducing persons to invest in regulated activities? • There are two exemptions to the rules against financial promotions by unauthorised persons. They relate to: • Certified high net worth individuals (see Art 48 Financial Promotions Order); • Certified sophisticated investors (see Art 50 Financial Promotions Order).

The exemption from authorisation for high net worth individuals This exemption disapplied the restriction in section 21 to financial promotions which are made to a person who the communicator believes on reasonable grounds to be a certified high net worth individual and which relate to certain investments. These investments may shares in or debentures or alternative debentures of an unlisted company. A certified high net worth individual is an individual who has signed a statement in the form prescribed in Part I (Statement for certified high net worth individuals) of Schedule 5 to the Financial Promotion Order. This requires the individual to certify that he has earned at least £100,000 or have held net assets to the value of more than £250,000 throughout the financial year before the date of the certificate. For the exemption to apply, the certificate must have been signed within twelve months of the date on which the communication is made. The validity of the statement is not affected by a defect in its wording or form provided the defect does not alter its meaning or involve failure to place certain paragraphs in bold.

FCA guidance on certified high net wealth individuals • FCA guidance at PERG 8.14.24 G to the effect that a person seeking to make a financial promotion to another person may wish to make enquiries of that person to establish whether he is certified • In the FCA’s view, a communication which is merely an enquiry seeking to establish that a person holds a current certificate will not itself be an inducement or invitation. Once it has been established that the person qualifies as a certified high net worth individual financial promotions about the controlled investments.

The exemption of invitation and inducements made to sophisticated investors • The other exemption to section 21 FSMA which may be relevant to TAL is the exemption which allows financial promotions to sophisticated investors. • Again, the terms of the exemption are detailed. In fact Article 50 relates to two different types of sophisticated investors: • those certified by an authorised person, and • those that are self-certified.

Article 50 (Sophisticated investors)) applies to persons who are certified by an authorised person and to a broad range of specified investments. Article 50A (Self-certified sophisticated investors)) is similar to the exemption for certified high net worth individuals and applies where the investor has self-certified himself and to a narrower range of specified investments.

This exemption also requires that certain warnings are given to the potential investor regarding risks. In this respect, article 50(3) (d) provides that the financial promotion must state that there is a significant risk of losing all monies invested or of incurring additional liability. This is a mandatory requirement.

Share offerings made to the public for investments in companies will generally need an FCA approved prospectus to be lawful. Invitations or inducements to invest in unauthorised investment activities will probably be unlawful. Exceptions to both rules exist for invitations to sophisticated investors and high net wealth individuals. III. CONCLUDING REMARKS

TIM GREEN Seconded to a “Technical Specialist” role at the Legal Department, Enforcement Division, FCA 2012 “A highly skilled barrister who is incredibly good in front of jury” “clients praised his commercial awareness” “one of the few counsel recommended for proceeds of crime work outside of London” Chambers and Partners 2014

Contact us: enquiries@st-philips.comSt Philips Chambers55 Temple RowBirmingham, B2 5LS 41 Park Square Leeds, LS1 2NP9 Gower StreetLondon, WC1E 6HBwww.st-philips.com Birmingham Tel: 0121 246 7000 Leeds Tel: 0113 244 6691 London Tel: 0207 467 9444