Download

1 / 34

350 likes | 636 Vues

The Roth IRA. What is it and how does it work Roth IRA vs. Traditional IRA Contributing to a Roth IRA Conversion from Traditional IRA Types of distributions Is the Roth IRA right for you?.

E N D

The Roth IRA What is it and how does it work Roth IRA vs. Traditional IRA Contributing to a Roth IRA Conversion from Traditional IRA Types of distributions Is the Roth IRA right for you?

This material is intended to provide general information and is not intended to provide legal or tax advice. Because individual situations vary, each situation should be examined carefully to determine appropriate planning strategies. It is recommended that decisions be made after consultation with competent financial, tax and legal professionals.

The Roth IRA • The Roth IRA is a retirement savings vehicle similar to the Traditional IRA. With a Traditional IRA you may get tax benefits when you put the money in. With a Roth IRA you may be able to take money out completely income-tax-free. 4

The Roth IRA • What the Roth IRA is and how it works • In the simplest terms, with a Roth IRA you put away currently-taxed income to be withdrawn income-tax-free during retirement.1 5 • 1 Assumes funds meet Roth IRA minimum holding requirements, if applicable. Retirement funds withdrawn from a Roth IRA before age 591/2 may be subject to income and/or penalty taxes, depending on the purpose of the withdrawal.

The Roth IRA • Differences between the Roth IRA and the Traditional IRA Traditional IRA Roth IRA • Tax-deductible contribution • Maximum contribution2 • Income-tax-deferred growth • Income-tax-free withdrawals • Minimum holding period • No • $3,000 • Yes • Yes • 5-year holding period may apply to withdrawals • Maybe1 • $3,000 • Yes • No3 • None • 1 Deductibility of Traditional IRA contributions are based on adjusted gross income and participation in an employer-sponsored retirement plan. • 2 For 2003-2004 contributions cannot exceed the lesser of $3,000 or your taxable compensation. Spousal contributions are based on total household income, allowing couples to make a maximum contribution of up to $6,000. If you are 50 years of age or older, the limit is $3,500. • 3 Withdrawals of non-deductible contribution amounts are tax-free.

The Roth IRA Traditional IRA Roth IRA Roth IRA 701/2 701/2 Varies depending on the type and purpose of the withdrawals Withdrawals are taxed at present rate1 • None • No required distributions for the original owner • Varies depending on the type and purpose of the withdrawals • Withdrawals are income-tax-free if the account is held for more than five years • Maximum contribution age • Required minimum distributions begin • Tax penalty for earlywithdrawals • Withdrawals for retirement 7 • 1 Withdrawals of non-deductible contribution amounts are income-tax-free.

The Roth IRA Traditional IRA Roth IRA • Withdrawals for first-time homebuyers ($10,000 lifetime maximum) before age 591/2 • Withdrawals for higher education before age 591/2 • Yes – income tax owed on amounts exceeding contributions if withdrawn within the first five years • Yes – income taxes owed on amounts exceeding contributions if withdrawn within the first five years • Yes – withdrawals taxed at present rate • Yes – withdrawals taxed at present rate 7 7

The Roth IRA • Roth IRA vs. Traditional IRA • Compare the difference between making a $3,000 contribution to a Roth IRA for 20 years and making a $3,000 contribution to a nondeductible Traditional IRA for 20 years. 8

The Roth IRA • Roth IRA vs. Traditional IRA1 Traditional IRA Roth IRA • Amount contributed • Value in 20 years $148,269 $148,269 • Taxes owed on lump-sum withdrawal • Total amount available to withdraw $60,000 $60,000 0 $23,833 $148,269 $124,436 1 This hypothetical example is not indicative of any particular investment and does not consider the tax deductibility of the Traditional IRA, which may be important for some investors. The example assumes all contributions are after-tax dollars. Investment return is assumed to be 8 percent, and the assumed federal income tax bracket is 27 percent. 6

The Roth IRA • Roth IRA vs. Traditional IRA • If the funds are withdrawn over a period of 20 years, how much would you be able to spend at the end of each year?1 Roth IRA: Traditional IRA: $15,102 $11,024 8 1 Withdrawals may be subject to income and/or penalty taxes. This hypothetical example is not indicative of any particular investment. Investment return is assumed to be 8 percent, and the assumed federal income-tax bracket is 27 percent both before and during retirement.

Putting money into the Roth IRA • You have two options for putting money into a Roth IRA: • Contribute new money to a Roth IRA each year. • Convert an existing Traditional IRA to a Roth IRA. 10

Putting money into the Roth IRA • Contributing new money to a Roth IRA • You can open a Roth IRA as long as you have earned income and your adjusted gross income is below a specified limit. 11

Putting money into the Roth IRA Married filing a joint return Married filing separately Single Income under $95,000 Income between $95,000-$110,000 Income over $110,000 Income under $150,000 Income between $150,000-$160,000 Income over $160,000 Full contribution Contribution of less than $3,000 No contribution allowed Income of zero (0) Income between 0-$10,000 Income over $10,000 11

Converting a Traditional IRA to a Roth IRA • If you convert a Traditional IRA to a Roth IRA, you trade current income taxes for the potential of income-tax-free withdrawals in retirement. • You can’t convert a retirement plan distribution directly into a Roth IRA. 13

Converting a Traditional IRA to a Roth IRA • You must meet the following qualifications in order to convert funds: • Your modified adjusted gross income (AGI) must be under $100,000, whether you are single or married filing a joint return. If you are married and file separate returns, you do not qualify for a conversion. The converted amount is not included in determining your AGI for this purpose.

Converting a Traditional IRA to a Roth IRA • You must meet the following qualifications in order to convert funds: • You must pay the income tax on the conversion in the year of the conversion.

Converting a Traditional IRA to a Roth IRA • Paying taxes on a conversion Taxes paid out of IRA Funds Taxes paid out of other funds IRA balance $100,000 Tax owed1 $27,000 Total remaining $73,000 10 percent early withdrawal penalty Total converted IRA balance $100,000 Tax paid out of other funds Total remaining $100,000 No early withdrawal penalty Total converted $2,700 $100,000 $70,300 14 • 1 Assumes a 27 percent federal income tax bracket.

Converting a Traditional IRA to a Roth IRA • Partial conversions • Consider a partial conversion if: • A full conversion would push you into a higher income tax bracket. • You don’t have enough cash available to pay the tax on a full conversion. 16

Converting a Traditional IRA to a Roth IRA • Five-year holding period • Withdrawals of earnings on the account and withdrawal of any funds converted from a Traditional IRA may be subject to penalty and income taxes; if a withdrawal is made within the first five years of the first contribution or conversion to the Roth IRA. 17

Converting a Traditional IRA to a Roth IRA • Five-year holding period • If you have multiple Roth IRAs, the clock begins with the first Roth IRA you open. When the first Roth IRA meets the five-year holding requirement, all your Roth IRA accounts meet the requirement. 17

Converting a Traditional IRA to a Roth IRA • Required minimum distributions • You are not required to take minimum distributions from a Roth IRA. 17

Types of distributions • The Roth IRA is a retirement savings account, but you might find that you need the money in your account for other purposes. Just remember that if you withdraw funds from your Roth IRA for purposes other than retirement, you will have less savings for retirement. 18

Types of distributions • Three types of distributions can be made from your Roth IRA: • Qualified distributions. • Taxable distributions with no penalty. • Taxable distributions with a penalty. 18

Types of distributions • Qualified distributions • After satisfying the five-year holding period, the following distributions can be made with no federal income tax or penalty owed. • Payments to you after age 591/2. • Payments to a beneficiary after your death. 18

Types of distributions • Qualified distributions • Distributions due to your disability. • First-time home purchase, up to the lifetime limit of $10,000 for you, your spouse, your children, your grandchildren, and your parents or other ancestors. 18

Types of distributions • Distributions with no penalty • After satisfying the five-year holding period, the following withdrawals can be made with no penalty owed, prior to age 591/2. Federal income tax is owed on any amount that exceeds the amount of annual contributions. 19

Types of distributions • Distributions with no penalty • Contributions, excluding earnings, can be withdrawn tax-free at any time. • Higher education expenses for you, your spouse, your children, or your grandchildren. • Certain medical expenses. • A series of substantially equal payments over your life (or life expectancy). 19

Types of distributions • Distributions with penalty • Any other distributions can be made at any time and are subject to federal income tax and penalties on the amounts exceeding the amount of contributions made directly to the Roth IRA. 19

Types of distributions • Taking out funds from a Roth IRA • If you have multiple Roth IRAs, no matter which account you take money out of, the money will be distributed in a set order: 1. Annual contributions (non-conversion). 2. Previously taxed portion of your first conversion Roth IRA. 3. Not previously taxed portion of your first conversion Roth IRA. 19

Types of distributions 4. The rest of your conversion IRAs, in order, with the previously taxed portion distributed first. 5. Any earnings on your accounts.

Traditional IRA$100,000 $50,000deductible $50,000nondeductible Remaining Traditional IRA balance $60,000 Roth IRA $40,000 $20,000 nondeductible $30,000 nondeductible $20,000deductible $30,000deductible Roth IRA case study 2: Bob and Brenda

The Roth IRA • These IRA choices raise a few questions: • Does it make sense for me to continue contributing to a Traditional IRA? • Should I put my money into a Roth IRA instead? • Should I leave my money in a Traditional IRA? 4

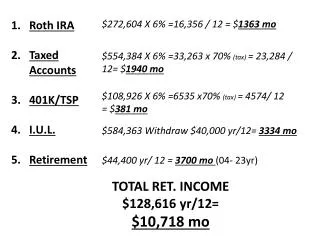

Questions? • Enrollment Process: 10 Minutes • Payroll Deducted: Up to $3000max/yr • 50 yrs or Older: Additional $500/yr

Thank you for attending cn 306843262004